Chicken Hawks

Chicken Hawks

And the risk of a crippling stock market bubble...

The Fed Funds futures market is now pricing in 100% probability the Fed hikes at least 50 basis points (0.50%) at each of the next three FOMC meetings scheduled for May 4th, June 15th and July 27th.

There’s even a roughly 50% probability baked in that the Fed makes it 75 basis points at one of those 3 meetings.

And, by the end of this year – the December 14, 2022 FOMC meeting to be exact – the futures are pricing in a certainty the Fed will have hiked a total of at least 2.75% in 2022.

Put simply, that’s like nothing we’ve seen in decades. The last time the Fed hiked 75 basis points was in November 1994 and I’d argue that hike from 4.75% to 5.5% almost 30 years ago is less meaningful than a 75-basis point hike from the current near-zero target range of 0.25% to 0.50%.

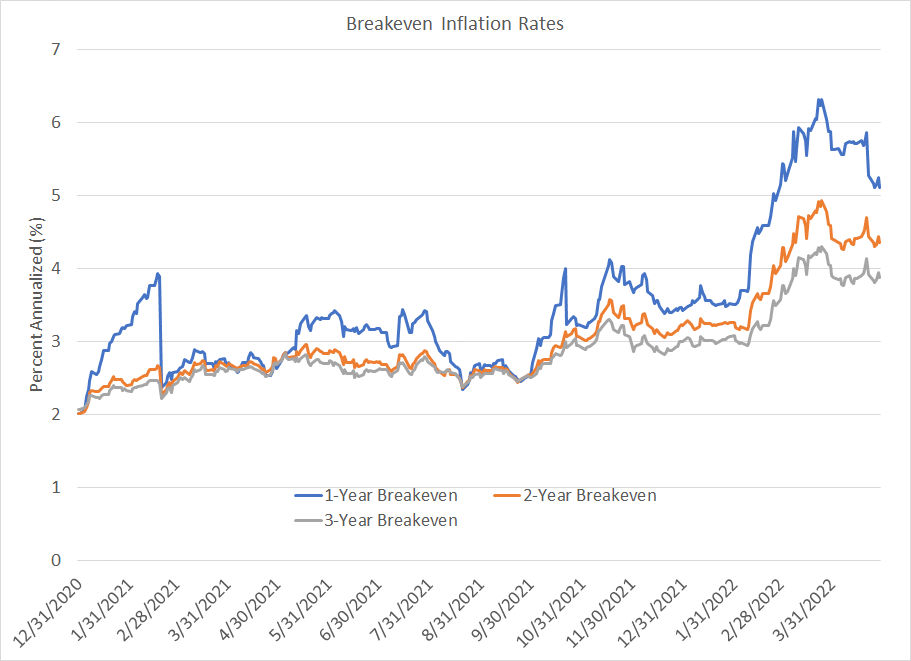

So, the market is betting on the Fed to be aggressive and hawkish this year and that’s helping cool short-term inflation breakevens:

Source: Bloomberg

Granted, the 1-year, 2-, and 3-year breakeven inflation rates are still much higher than in late 2020, even higher than they were at the end of last year. And even the three-year breakeven at 3.88% implies an average inflation rate over the next 3 years that’s nearly double the Fed’s target.

However, the recent trend here is significant – 1-year breakeven inflation rates are down more than 1% from their highs in late March, the two-year is down about 55 basis points and the 3-year is off about 43 basis points.

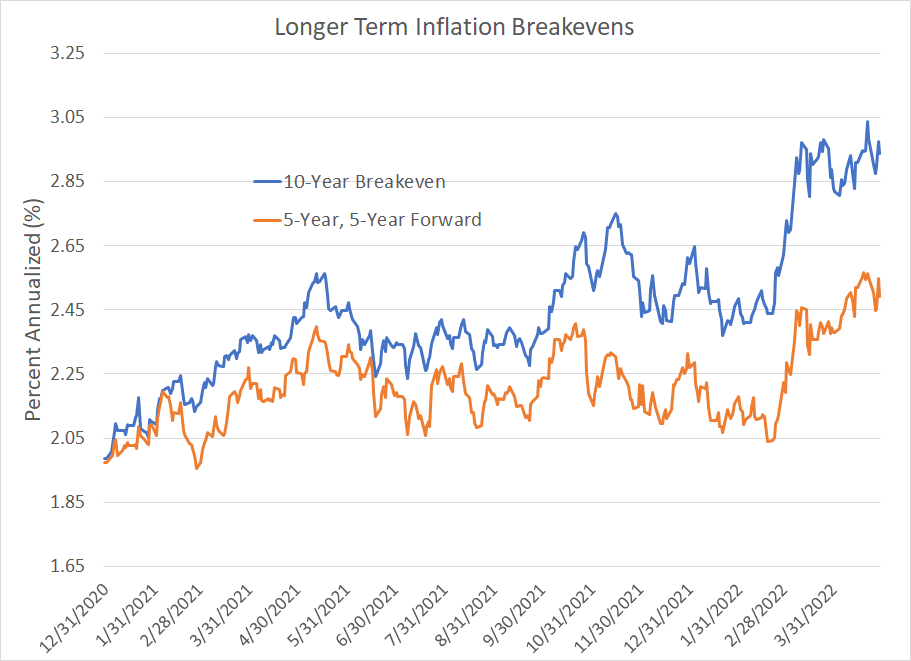

However, the longer-term outlook is different:

Source: Bloomberg

While the numbers aren’t as elevated in absolute terms, I’d argue this chart is even more sinister.

As you can see, the average expected inflation rate over the next 10-years (blue line) is currently 2.94%, almost 100 basis points above the Fed’s target. Meanwhile the average expected inflation rate for the 5-year period starting 5 years from now – average annualized inflation expected from roughly 2027 to 2032 – is 2.50%.

Even more interesting, these longer-term measures of expected inflation have been jumping to new highs since mid-April even as the shorter-term measures I outlined earlier have moderated somewhat.

Transitory Anyone?

Two points about this.

First, the market clearly no longer buys the line that inflation is temporary, transitory, or solely the result of COVID-related distortions and the Russian invasion of Ukraine.

Ask ten different investors to define “short-term” and you might get 10 different answers, but I’d wager none of them would be “a decade” or 2027 to 2032.

That’s long-term or, charitably, intermediate term. It’s increasingly apparent the US (and global) inflation problem is bleeding into longer-term expectations – the growing danger is consumers begin to expect higher inflation and act accordingly, resulting in a 70’s style self-fulfilling inflationary spiral.

And there’s a second implication of this setup– the market sees the Powell Fed as a flock of “chicken” hawks.

In other words, market participants are looking for the Fed to hike aggressively over the next 3 months, maybe even into early next year. That’s halting the unchecked advance in expectations for inflation over the next 1 to 3 years.

However, the market is similarly convinced the central bank will eventually blink in the face of the inevitable slowdown in economic growth and the labor market that accompanies such a dramatic reversal in monetary (and fiscal) policy.

The uncomfortable truth is the way central banks beat inflation is by engineering a recession.

Economic downturns result in pain, including rising unemployment, a bear market in stocks and, perhaps, turmoil in the housing market. The market is betting the Fed will “chicken out” at the first sign of economic or market trouble rather than pushing past the pain as Paul Volcker’s Fed did back in the early 80s.

And to be frank, who can blame investors for thinking that’s likely?

After all, Jerome Powell’s Fed did a dramatic about-face on rate hikes in late 2018 and early 2019 in response to the mini bear market in the S&P 500 back in Q4 2018. That’s despite the fact there was precious little evidence the US economy was faltering back in 2018 and the US labor market remained strong with unemployment under 4%.

A Reverse Wealth Effect

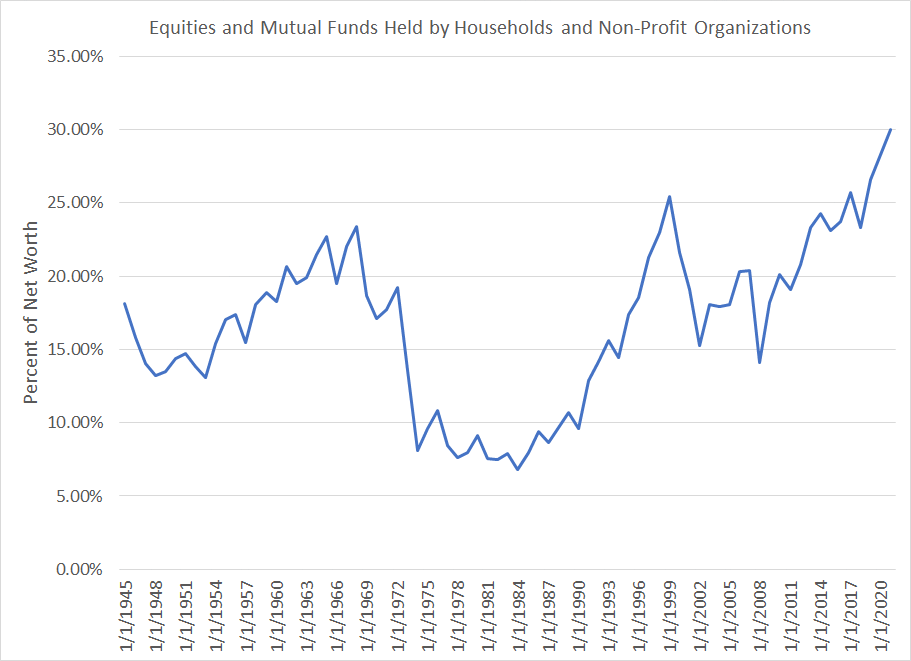

This chart must be of more than just casual concern for the Fed:

Source: Bloomberg, Federal Reserve

According to the Fed, at the end of 2021 US households and non-profit organizations (NPO) had a record net worth of over $150 trillion in nominal terms, up about 142% since the end of 2009, which is well above the roughly 32% rise in the Consumer Price Index (CPI) over the same time frame.

However, what’s interesting is direct holdings of equities (stocks) and indirect holdings of stocks (and bonds) through funds accounted for just under 30% of that total net worth as of the end of 2021. That’s the highest ratio in the history of this series dating back to 1945.

The two prior peaks on this chart are December 31, 1968, and December 31, 1999. The former represents the peak of the bull market that immediately preceded a long period of range-bound trading in the S&P 500 from 1968 through 1982. Of course, the latter represents the peak of the late 1990s bull market in the Nasdaq, technology and growth stocks. Both peaks were followed by significant pain for investors.

There are two implications.

First, on this basis, the bubble in equity and bond markets since the end of 2008 has reached unprecedented levels – households are more “bulled up” on stocks and funds than at any time since 1945.

Second, consider what’s known as the wealth effect – when consumers feel wealthier because the value of their assets rises, they tend to spend more freely. That effect is evident over the past two years – since the end of 2018, the portion of household net worth in stocks and funds has leapt by nearly 7 percentage points, a record matched only in the late 1990s.

The Fed’s easy money, and the breathtaking rally in stocks from the 2020 lows has helped turbocharge the economy, creating a grand stock market wealth effect for consumers.

However, there’s a flip side to that, a potentially devastating vicious cycle. Should the Fed’s hiking campaign continue to drive downside in the stock and bond market (higher yields means lower bonds prices) there would be a negative wealth effect as investors feel poorer. And, since a greater portion of household net worth is tied up in financial markets than at any other time in post-War history, the downside risks here from that reverse wealth effect are staggering.

As much as the Fed might insist it doesn’t target asset prices or the stock market, the erstwhile equity bubble has linked the fortunes of the S&P 500, the Nasdaq and the US economy like never before.

So, it’s not a stretch to suppose the Fed will eventually panic in the face of tumbling stock markets and weakening economic conditions, cutting interest rates and/or restarting quantitative easing as a result. Something similar happened in 1974 when the Fed began cutting rates from a May 1974 peak of 13% to under 5% by early 1976 before inflationary forces were truly under control.

The result: Inflation remained a problem throughout the 1970s with the Fed under Arthur Burns and, later, William Miller ultimately unwilling to accept economic pain as the price for bringing inflation under control.

Simply put, the market views the Powell Fed as more likely to follow the pattern of the Burns and Miller Feds than the Volcker example of the early 1980s.

If you enjoyed this piece, please do me a favor and click the heart-shaped “like” button below this post. This helps raise the profile of this free Substack service, so I can justify posting more frequently.

And, if you have any questions or comments, be sure to post in the comments section below. I plan to feature answers to common questions in upcoming posts.

DISCLAIMER: This article is not investment advice and represents the opinions of its author, Elliott Gue. The Free Market Speculator is NOT a securities broker/dealer or an investment advisor. You are responsible for your own investment decisions. All information contained in our newsletters and posts should be independently verified with the companies mentioned, and readers should always conduct their own research and due diligence and consider obtaining professional advice before making any investment decision.