Earnings Alchemy, Rates and the Nasdaq

Earnings Alchemy, Rates and the Nasdaq

The flawed bullish pivot narrative

On the surface it’s been a placid 10 days for equity markets with the S&P 500 unchanged since its close on Friday April 14th and the Nasdaq 100 down 0.82%.

However, the next two weeks are pivotal.

I regard earnings from JP Morgan Chase & Co. (NYSE: JPM) as the unofficial start to quarterly earnings season. However, while JPM reported a little over a week ago on Friday 14th, only about 20% of companies in the S&P 500 have reported to date and just 14% of stocks in the Nasdaq 100.

In the week ended this Friday April 28th, 178 stocks in the S&P 500 representing more than 43% of the total index market capitalization will report their Q1 2023 results. And the week that follows, ended May 5th, brings results from 168 companies in the S&P 500 with a more than 23% share of the total S&P 500 market cap.

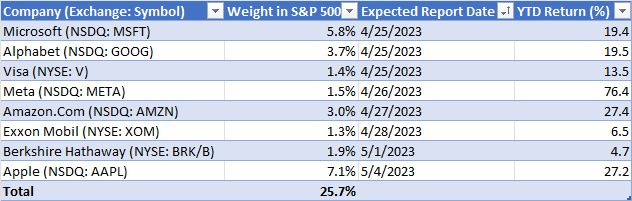

Here are the 8 stocks due to report earnings over the next two weeks with the highest weights in the S&P 500:

Source: Bloomberg

As you can see, five of these eight names are technology and growth mega caps that have generated an average total return of almost 34% year-to-date compared to the S&P 500, up just 8.3%. In short, these have been leaders of the year-to-date rally and it’s tough to imagine a scenario where these 5 stocks falter without the S&P 500 also getting hit.

Economic Growth, Interest Rates and the Nasdaq

As I’ve written previously, since this bear market started in early 2022, equity markets have retained a strong inverse correlation with moves in interest rates and expectations for Fed policy.

Simply put, when rates rise, the market falls and vice versa.

That’s the core of the bullish narrative right now: Inflation has peaked, and the economy is weakening, allowing the Fed to pivot on interest rates later this year, which is bullish the stock market. This Fed pivot case is generally seen as most bullish for the Nasdaq and growth stocks, including those in my table above, that dominate the earnings calendar over the next two weeks.

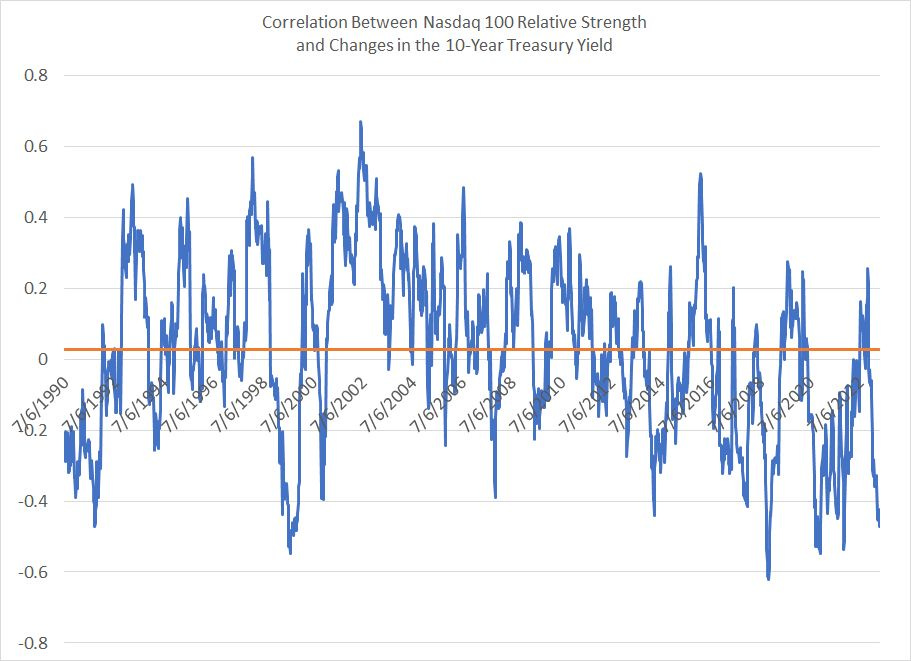

There’s only one slight problem with that – the Nasdaq and interest rates aren’t inversely correlated:

Source: Bloomberg

To create this chart, I examined weekly total returns for the Nasdaq relative to the S&P 500 and weekly changes in the 10-year Treasury yield since June 1990. I then calculated a 26-week (6-month) correlation between these two series, with a positive number indicating Nasdaq tends to outperform when rates are rising and a negative number indicating Nasdaq outperforms when rates are falling.

The orange line at +0.0265 is the average correlation for the entire dataset – there’s a weak positive correlation between interest rates and Nasdaq relative strength over the past 33 years.

That flies in the face of the conventional wisdom that a Fed pivot, and lower interest rates, is bullish for the Nasdaq and growth stocks.

Of course, this relationship is far from stable over time and since 2016-17 there has been a downward shift in the correlation – since the beginning of 2017 the average correlation between rates and Nasdaq relative strength is about -0.17.

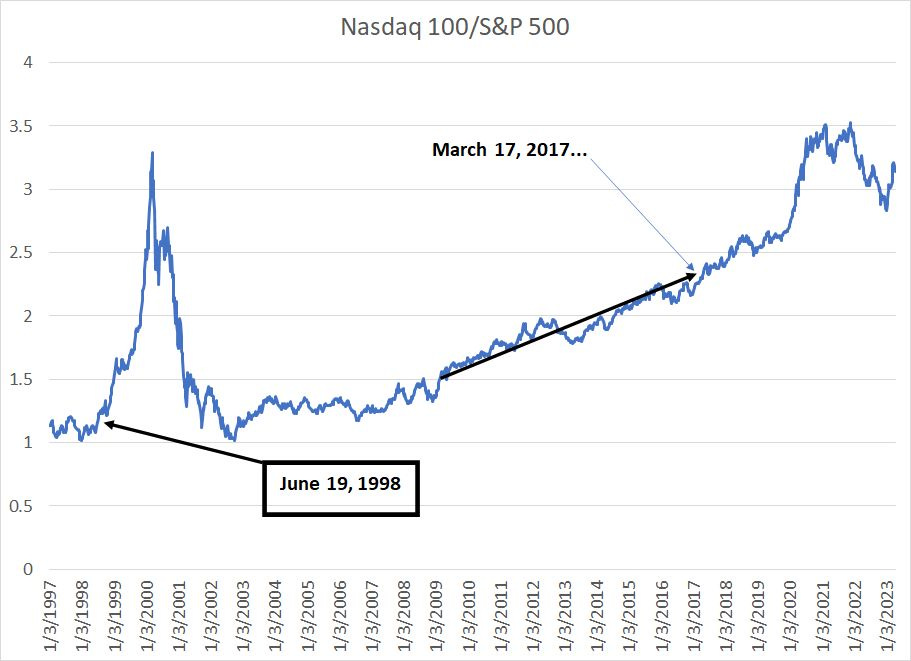

This shift roughly corresponds to the surge in Nasdaq relative strength to the S&P 500:

Source: Bloomberg

It’s also worth noting the last time the Nasdaq 100 saw a relative strength surge to the S&P 500 in the 1998-2000 period, the correlation with interest rates also flipped negative. The late 1998-2000 experience is the only other period in the past 30 years where the magnitude of the inverse correlation between Nasdaq relative strength and interest rates has been as large as it’s been over the past few years.

That makes some sense considering the bubble mentality that gripped investors in 1997-2000 and over the past few years.

Specifically, Nasdaq 100 outperformance so far this year reflects the view growth stocks will benefit from lower interest rates while suffering no ill effects from the economic trends that drive interest rates lower.

In other words, for the Nasdaq surge to make sense, one must assume earnings for the stocks in the index won’t be impacted to a significant degree by a looming US recession. Or, at a minimum, earnings and growth prospects for the likes of Amazon.Com (NSDQ: AMZN), Microsoft (NSDQ: MSFT) and Apple (NSDQ: AAPL) have only modest and transitory exposure to broader US, and global, economic conditions.

That’s the same argument made about the Nasdaq and growth stocks 23 years ago in early 2000. The idea then was that tech stocks were acyclical because rapid growth in use of the Internet could drive steady earnings and revenue growth over time even as the broader economy entered recession. Trends like Internet-enabled growth in business-to-business “B2B” services, and the need to invest heavily in networking gear able to handle the explosion in data traffic, were used to justify nosebleed valuations.

This time around, it’s themes like artificial intelligence (AI) and electric vehicles (EVs) that’s supposedly driving acyclical growth, and rising valuations, for stocks like Microsoft and Tesla (NSDQ: TSLA).

The problem is that assumes this time is different.

This is predicated on the view a small cadre of US tech and growth stocks have truly invented a perpetual recession-resistant growth machine. That leaves investors free to ignore pedestrian considerations like the health of the business cycle or the prospect COVID lockdowns may well have pulled forward demand for certain tech products, leaving scope for an earnings hangover into H2 2023 and 2024.

Inventing a way to abolish the business cycle stands about as much chance of success as medieval alchemists’ centuries-long efforts to convert base metals like lead into gold. Ultimately, I’m looking for the negative correlation between interest rates and the Nasdaq to mean-revert to a positive, or at least more neutral, level as investors come to the realization that when the economy shrinks, and consumer spending falters, it’s not likely to be good news for Microsoft and Apple.

The earnings deluge over the next two weeks will help determine if that monumental shift is imminent or if the alchemist fantasy can hold sway a bit longer.

DISCLAIMER: This article is not investment advice and represents the opinions of its author, Elliott Gue. The Free Market Speculator is NOT a securities broker/dealer or an investment advisor. You are responsible for your own investment decisions. All information contained in our newsletters and posts should be independently verified with the companies mentioned, and readers should always conduct their own research and due diligence and consider obtaining professional advice before making any investment decision.