Fed Rate Hikes and Market Bottoms

Fed Rate Hikes and Market Bottoms

And why the June lows won't hold...

People have different opinions about the path of the stock market and, of course, I can understand and respect that. Indeed, different opinions are what make a market.

However, as financier Bernard Baruch once said: “Every man has a right to his opinion, but no man has a right to be wrong in his facts.”

One of my pet peeves is to hear and read multiple people declare something about markets as fact, when it’s demonstrably untrue.

A recent example is the notion the stock market usually bottoms before the end of a Fed rate hike cycle or that a Fed “pivot” is uniformly bullish for stocks.

Neither claim is true.

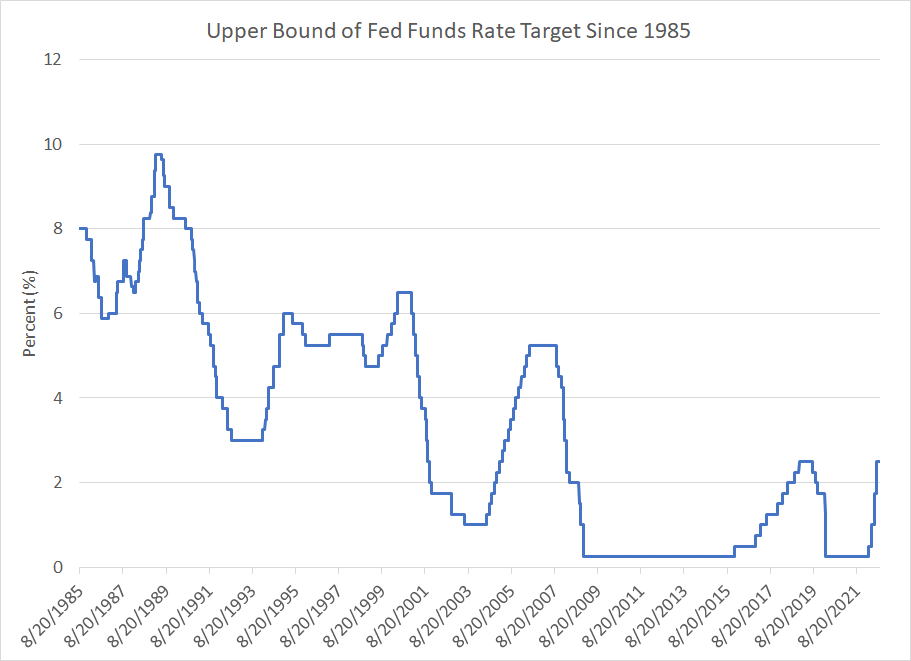

Let’s start with a look at the upper bound of the Fed’s target for interest rates:

Source: Bloomberg

There are several rate cycles evident on this chart since the mid 1980s.

For example, the Fed hiked interest rates from 1% in 2004 to a peak of 5.25% in 2006 with the final 25 basis point hike in that cycle coming in June 2006. The Fed then left rates steady for over a year until it cut by 50 basis points in September 2007.

Rates finally bottomed at 0 to 0.25% in late 2008.

Of course, the stock market peaked in October 2007 and fell by around 50%, reaching a low in March 2009. So stocks did NOT bottom before the Fed finished hiking rates, the S&P 500 bottomed only months after the Fed had been through a prolonged cutting cycle.

The same can be said of the 1999-2000 Fed cycle. The first hike in that series was June 1999 and the final hike came in May 2000. Over this period of just under one year, the Fed hiked 6 times for a total of 175 basis points to a peak rate of 6.50%. The Fed then maintained rates at 6.5% until the central bank cut 50 basis points in January 2001.

The stock market peaked in March 2000, falling almost 50% to its October 2002 lows. Much like 2008-09, the S&P 500 didn’t bottom until AFTER the Fed had cut interest rates to 1.75% through a series of 11 cuts.

Of course, then the Fed actually continued to cut rates after the late 2002 market lows, reaching a terminal rate of 1% in the middle of 2003.

Indeed, one common feature of every bear market since 1973 — there have been 7 such declines — is the market only bottoms AFTER the Fed cuts interest rates at least once.

Based on the Fed Funds futures market, traders are looking for the Fed to hit a terminal rate — the highest Fed funds rate for the current hiking cycle — of roughly 4.4% by March of 2023. Since the current target rate is 2.25% to 2.5%, that implies about 200 basis points of additional hikes including a (likely) hike of 75 basis points next week.

Currently, the Fed funds futures price in a target rate of 4% by the time of the Fed’s November 1, 2023 meeting, which implies rising probability at least one cut of 25 basis points or more around the middle of 2023.

Of course, these are just predictions made by traders in that market and have been moving around a great deal over the past few months in response to incoming data and rhetoric from Jerome Powell and others at the Fed. However, if the central bank does start cutting next summer, and the pattern of bear markets in the past half century holds up, the S&P 500 wouldn’t bottom until late next year.

So, what are the Fed “pivot” bulls on about?

There are actually a number of factors at work. But I think one of the most important are what psychologists call a “recency” bias — basically, humans are hard-wired to overestimate the important of recent experience when making decisions.

I cover this issue in a bit more depth in the video presentation I recently posted to YouTube here:

DISCLAIMER: This article is not investment advice and represents the opinions of its author, Elliott Gue. The Free Market Speculator is NOT a securities broker/dealer or an investment advisor. You are responsible for your own investment decisions. All information contained in our newsletters and posts should be independently verified with the companies mentioned, and readers should always conduct their own research and due diligence and consider obtaining professional advice before making any investment decision.