Fooled by the Seasonals

Fooled by the Seasonals

It seems the fundamental bullish market narrative shifts weekly this year.

The bulls first hung their hats on misplaced expectations for an imminent Fed pivot, then it was “immaculate disinflation” (soft landing + lower inflation) and, finally “no landing,” which apparently signifies continued strong economic growth despite surging interest rates.

The bulls’ game of musical chairs was finally interrupted last week:

The Nasdaq 100 was down just over 3.1% for the week with the S&P 500 down 2.7%, and the iShares 7-10 Year Treasury ETF (NYSE: IEF) off 1.1%. That’s on pace for the largest weekly sell-off for the S&P 5090 and the Nasdaq 100 since the first week of December (December 2 to December 9th).

Does that mean the powerful equities rally to start 2023 is over?

As The Free Market Speculator readers know, I don’t put much stock in the bullish fundamental narratives that have dominated the year so far, and I continue to target the 3,000 to 3,100 level on the S&P 500 at some point in 2023, consistent with an average bear market decline in the broader index from the early 2022 peak.

My problem with the no landing narrative remains that it’s based primarily on a handful of lagging economic series such as retail sales and monthly employment data. I’ve written extensively about the employment numbers this year, including here and here, now let’s take a look at retail sales:

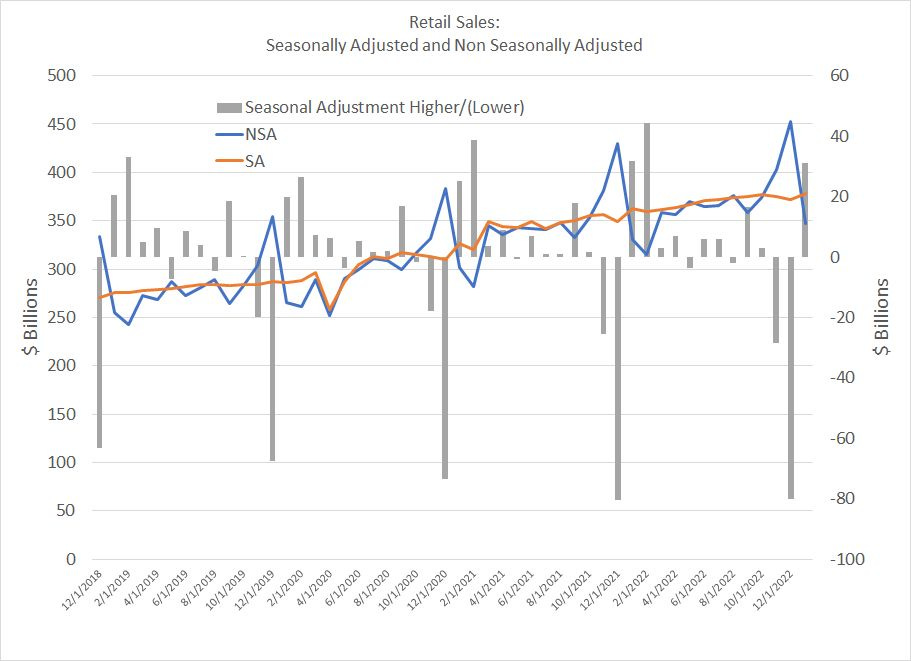

Source: Bloomberg

This chart shows the monthly retail sales data excluding gas stations, auto dealerships, food services and building materials since the end of 2018. The orange line is the seasonally adjusted figure while the blue line is the raw data series – the grey bars represent the seasonal adjustment the government applies to the data, higher or lower.

Note that these are all nominal numbers, not adjusted for inflation.

When the Census Bureau released this series on February 15th, it looked much better than economists had expected and lent credence to the “no landing” narrative.

However, retail sales – particularly the series I’ve charted -- have historically followed a seasonal pattern in the US, rising in the months of November and December due to the Christmas holiday and falling in the New Year. This is normal and happens every year – the fact that retailers sell more in December than in January tells us nothing about the strength of the economy.

That’s why the Census Bureau, which reports these figures, applies a seasonal adjustment to the monthly data – they adjust the raw data lower in November-December and higher in January and February to reflect the normal cadence of sales through Thanksgiving/Black Friday, Christmas and New Year.

The idea is that applying these seasonal adjustments helps us understand whether retail sales are strong or weak relative to expected seasonal norms.

So, while the widely reported seasonally adjusted retail sales number reported for January 2023 was $378.38 billion, the actual raw retail sales number was $347.243 billion – the government added in $31 billion to that raw number to adjust for the normal seasonal retail sales slump in January.

This all makes logical sense. However, Census uses historical patterns to perform these adjustments, so if historical patterns change, the adjusted figures can provide a distorting effect.

Of course, Christmas 2022 wasn’t canceled, so there was a normal seasonal surge in the raw data to end 2022.

However, since 2020, there has been a bias in a different form:

And the Survey Says...

Let’s look at the Wall Street consensus outlook for the month-over-month % Change in retail sales and the actual data since August 2020:

Source: Bloomberg

Look at the three red arrows I’ve drawn on this chart.

Do you see how the reported seasonally adjusted retail sales numbers have tended to look weak relative to expectations in late 2020, 2021 and 2022 and then surged well ahead of expectations in January for each of these years?

Of course, this holiday season was no exception with both November and December 2022 retail sales below expectations prior to that blockbuster number for January 2023.

I’d posit this pattern, which has only existed since 2020, suggests there has been a subtle-yet-powerful shift in the seasonality around holiday sales. Most likely, this reflects consumers’ general propensity to do more of their holiday shopping earlier in the year than normal (before November).

Of course, I don’t know why that’s happened.

It could be that amid the lockdown-driven supply chain mess over the past few years, consumers were worried about the lack of goods availability as the Thanksgiving-Christmas season approached. Or it could be the surge in online shopping means consumers find it more convenient to spread their holiday shopping over more months, earlier in the year.

Regardless, if you seasonally adjust November and December sales down to reflect holiday shopping patterns before coronavirus lockdowns (2019 and earlier), then your downward seasonal adjustments are likely to be too large if consumers are simply doing their shopping earlier in the year. This makes retail sales look artificially weak.

And if you then were to adjust January sales higher to reflect the post-Christmas hangover, the upward seasonal adjustment could make January sales look artificially strong.

My point: If retail sales and employment are the main fundamental support for a “no landing” scenario, that narrative rests on a foundation of shifting sand.

It’s quite possible, should the seasonal pattern hold, February retail sales, to be released on Wednesday March 15th will look pretty weak because of the fading tailwind of an inflated positive seasonal adjustment that flattered the January 2023, January 2022 and January 2021 sales estimates.

The Long and Short

While my fundamental read on the markets and economy has changed little since late 2022, I still think it’s too early to fully embrace the potential downside for markets:

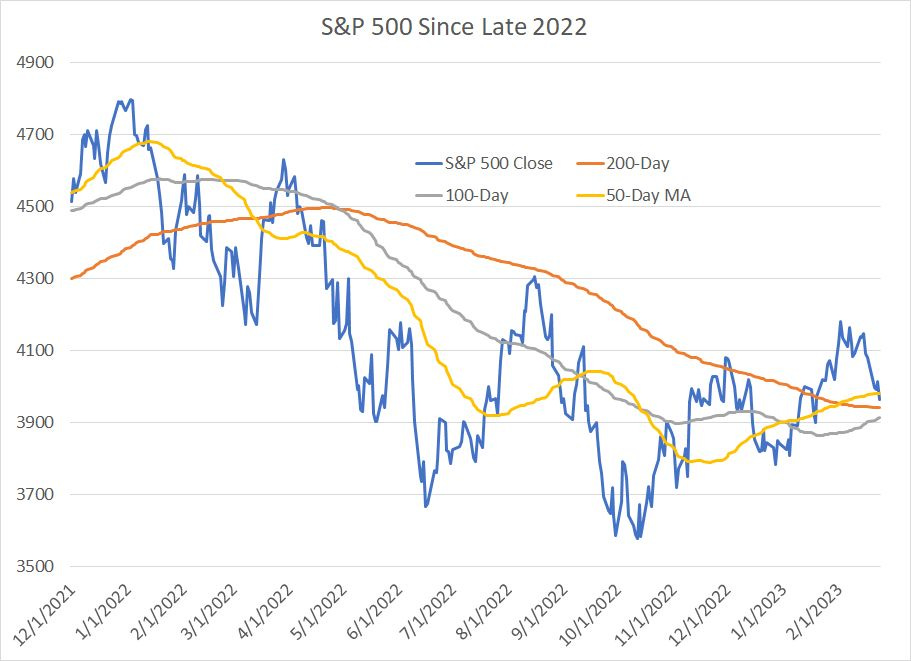

Source: Bloomberg

As you can see, the S&P 500 has pulled back from its early February peak, however, it’s now back into technical support at the confluence of the 50-day, 100-day and 200-day moving averages.

Moreover, a level of roughly 3,950 would represent a 38.2% retracement of the entire October 12th to February 2nd rally in the S&P 500 while a level of 3,875 would represent a 50% retracement. These are both Fibonacci levels that are widely watched by technicians and both represent support below the current quote.

Moreover, as I’ve written repeatedly this month, bear market rallies are a function of sentiment and positioning, NOT fundamentals. With the market now pulling back into support, I suspect there will be some underinvested bulls who missed the initial rally off the lows and are now desperate to buy the dip.

At some point, the short-run will give way to the long-run, and markets will begin to reflect the deteriorating fundamentals I’ve outlined in this issue and prior updates.

The trick is, of course, timing that shift. The best we can do for now is watch the charts, continue to follow indicators like market breadth and upside/downside volume and keep an eye on particular fundamental catalyst dates such as the next employment number due on Friday March 10th, retail sales on the 15th and the Fed meeting on the 22nd.

DISCLAIMER: This article is not investment advice and represents the opinions of its author, Elliott Gue. The Free Market Speculator is NOT a securities broker/dealer or an investment advisor. You are responsible for your own investment decisions. All information contained in our newsletters and posts should be independently verified with the companies mentioned, and readers should always conduct their own research and due diligence and consider obtaining professional advice before making any investment decision.