Germany's Climate "Success"

Germany's Climate "Success"

The real reason carbon emissions hit a 70-year low...

The mainstream media loves to sing the praises of German energy policy and the country’s alleged success meeting its carbon emissions goals.

Early this year we were treated to a slew of headlines like this one from the Associated Press:

Source: ABC News January 4, 2024

It turns out this gem of a statistic is from a think tank called Agora Energiewende. The word “energiewende” means energy transition and, according the think tank website, its goal is to “develop feasible solutions and strategies for the decarbonization of the energy system on the way to climate neutrality.”

So, how did Germany achieve that impressive drop in carbon emissions last year?

Well, climate activists and think tanks, politicians and the mainstream media would like you to believe it’s down to the country’s rapid development of renewable energy generating capacity:

Source: Reuters, January 3, 2024

After all, as the above headline from Reuters explains, renewable energy technologies like solar and wind picked up 6.6 percentage points of market share in 2023, rising to 55% of all power generated on the German power grid last year.

Indeed, Germany’s renewable power installations hit a record in 2023 and the government is targeting 80% of electricity generation from renewables by 2030 on its way to net zero by 2045. Of course, the implication of all this is that phasing out fossil fuels like natural gas, coal and oil is not only feasible, it’s almost a reality, at least in Germany.

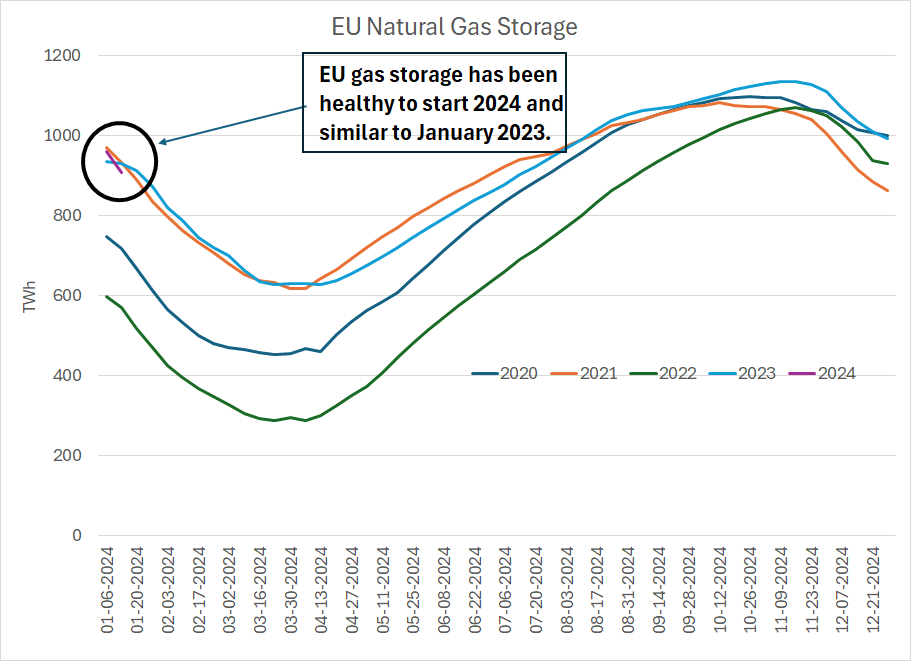

Meanwhile, some will tell you that thanks to the rapid growth in renewables generation, the European Union is awash in natural gas despite the loss of Russian supplies in 2022:

Source: Bloomberg

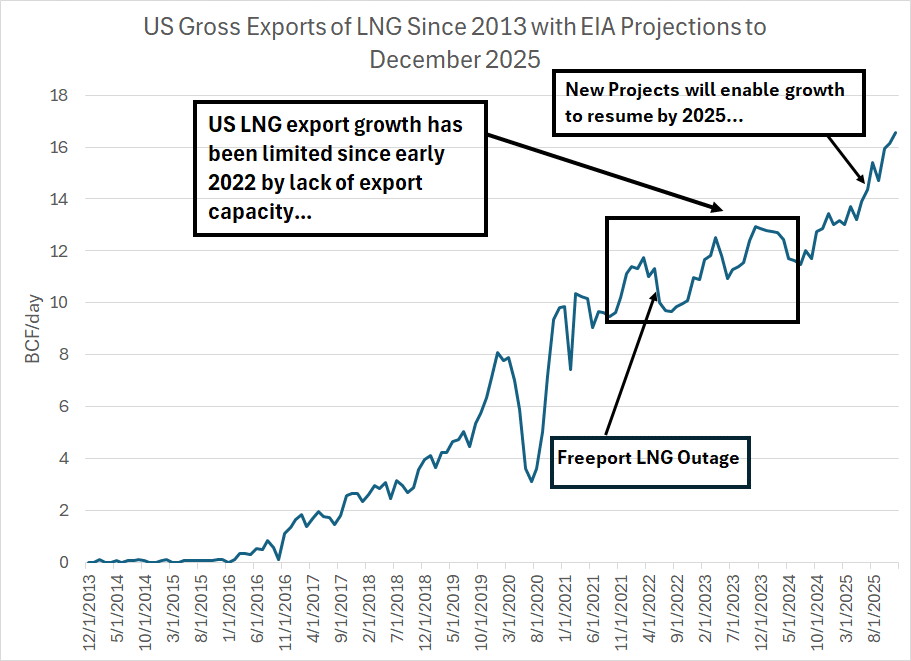

Some even question whether there’s adequate global demand for natural gas to support the rapid expansion in US liquefied natural gas (LNG) export capacity slated for the next few years:

Source: Bloomberg

The list of new US liquefaction projects includes the Golden Pass LNG facility in Texas with 2.4 bcf/day of peak export capacity and the Plaquemines LNG project in Louisiana with peak export capacity of more than 3 million bcf/day. The Port Arthur and Corpus Christi Stage III projects, both located in Texas, would add an additional 3.29 bcf/day of combined capacity.

And these are just projects that have already received approval and are under various stages of construction; additional capacity is in earlier stages of planning and approval with potential start-up after 2027.

Construction timetables are always fluid, especially for a large-scale project like an LNG terminal. Indeed, last month Exxon Mobil announced a delay to its Golden Pass LNG terminal. Previously the project was expected to be completed in stages from Q2 2024 through Q1 2025 and now management sees the first stages of project completion at year-end and first exports in early 2025.

Regardless, current peak US LNG export capacity is around 14 bcf/day and that’s likely to grow to about 22.5 bcf/day by early 2025 and more than 26 bcf/day by 2027. That’s a near 90% increase in US LNG export capacity over a period of about 4 years.

So, could the global market be headed for a glut of gas, as demand from major importers like the EU collapses just as US export capacity takes off?

Take a closer look at the real drivers of falling German demand for natural gas and other fossil fuels and the entire “net zero” narrative collapses.

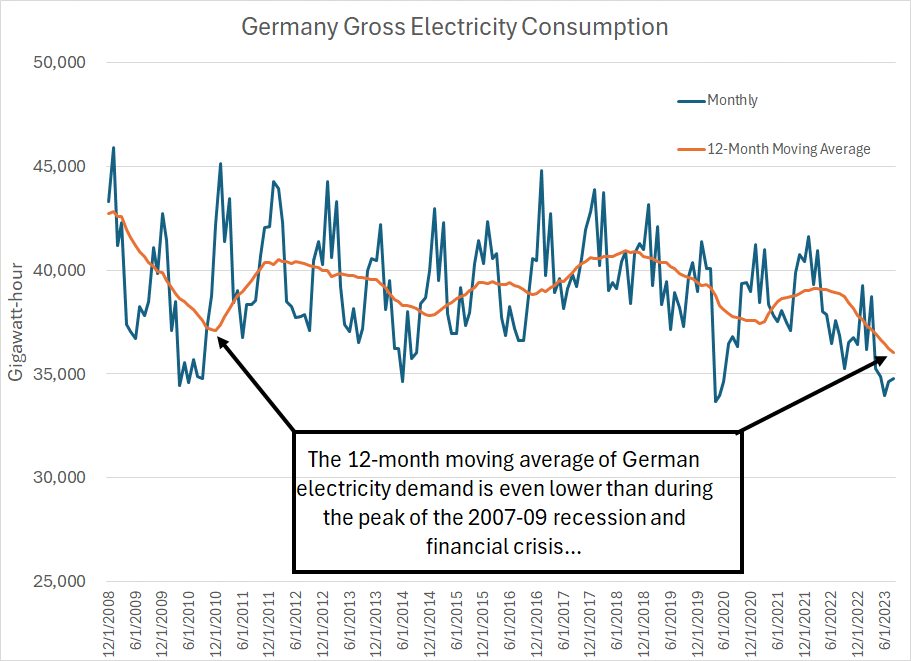

First up, look at German electricity demand since 2008:

Source: Bloomberg, Eurostat

A quick glance at monthly data on German electricity consumption reveals the 12-month moving average of demand has plunged since early 2022. In fact, the 12-month moving average of German electricity demand is lower today than it was at the height of the recession and financial crisis years of 2007-09.

The key to Germany’s “success” in reducing natural gas and electricity demand was to engineer a recession, particularly in so-called energy-intensive industries.

According to the German Federal Statistical Office, the industrial sector accounted for 29% of total energy demand in 2021, the year before the Russian invasion of Ukraine. That makes the industrial sector the single largest consumer of energy in the country, ahead of private households at 28% and the transport sector at 27%.

(That shouldn’t come as a huge surprise since Germany has been long regarded a manufacturing powerhouse.)

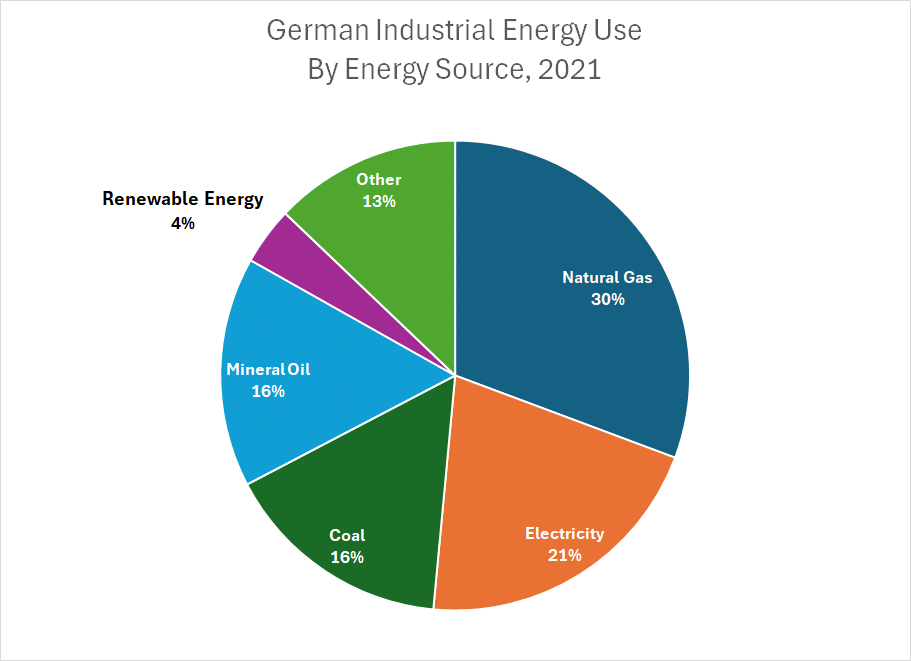

Here’s a look at the source of energy for Germany’s industrial end-users:

Source: German Federal Statistical Office

As you can see, natural gas is the single largest source of energy for Germany’s industrial sector, accounting for more than 30% of total use. Natural gas, electricity and coal combined comprise more than two-thirds of the total. If you’re wondering, “Mineral Oil” is what the German Statistical Office calls crude oil and refined products.

Meanwhile, a handful of energy-intensive industries account for an outsized portion of German industrial energy demand including chemical manufacturing, basic metals production, refined products and paper and paper products.

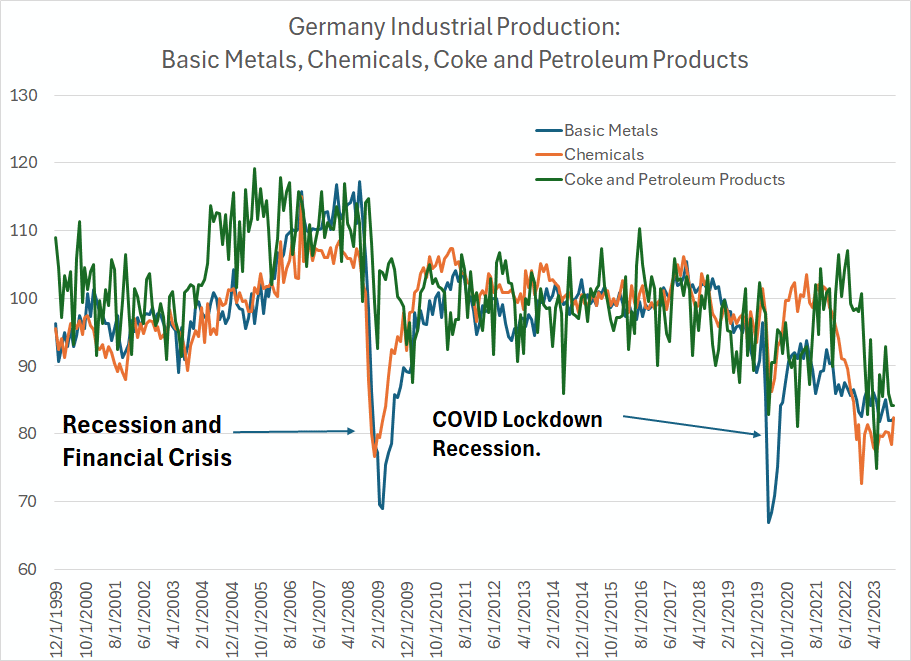

So, the main reason Germany has been able to reduce electricity and natural gas consumption, alongside related carbon emissions, so much since 2021 is these energy-intensive industries have dramatically cut back production:

Source: Bloomberg, Eurostat

This chart shows German industrial production (IP) for three energy-intensive industries since December 1999. These figures represent an index where industrial production in 2015 is equal to a base level of 100.

As you can see, it’s normal for IP in these economically sensitive industry groups to drop during recessions; however, recoveries following the recessions of 2007-09 and 2020 were relatively rapid.

Since 2022, IP for all three of these industry groups has dropped to recessionary levels.

Even worse: There’s no sign of the normal cyclical rebound you’d see following an economic downturn.

The problem is that while electricity and natural gas costs in Europe are off their peaks, they’re still far higher than in many other industrialized countries around the world including the US. Further, gas and electricity costs are significantly above average “normal” levels prior to the 2021-22 run-up. Given that stubborn, elevated cost structure, it’s just not profitable for many German industries – especially these core energy-intensive industries – to boost their output.

Germany’s energy transition efforts in recent years, including shuttering all its nuclear power capacity, and expanding intermittent renewables over coal and gas, have exacerbated the problem.

In fact, the German Chamber of Commerce and Industry conducted a survey of German industrial companies last summer and found almost two-thirds felt Germany’s energy transition had impacted their business negatively or very negatively. Almost one-third (32%) favored investment abroad over domestic expansion, double the 16% in the 2022 survey.

Of course, the risk of deindustrialization in an economy known for its manufacturing excellence is too great to be ignored. After months of political wrangling, the German government announced a plan to support industry back in November.

The list of policy measures includes cutting the electricity tax to the lowest level permitted by the European Union for all manufacturing firms and providing additional, direct support for 350 companies that compete globally and are seen as the most at-risk of relocating their operations outside the country.

Providing subsidies and support for German households and businesses to offset sky-rocketing energy costs has become expensive and is only possible under EU rules because of a temporary crisis support measure put in place following the initial Russian invasion.

Simply put, my view has been, and remains, countries like Germany, hit hard by sky-rocketing energy costs following Russian supply disruptions, would be delighted to see the projected increase in US LNG supplies and the resulting economic and fiscal relief.

The energy crisis in Europe isn’t over, not even close.

Between Europe and Asia, I see plenty of demand to absorb new supplies of US LNG as well as LNG expansion from other producing countries.

The diversification of supply would also represent a welcome development compared to European dependence on Russian imports prior to 2022. The exact level of European gas prices this winter is less relevant than the need to forestall longer-term economic damage from skyrocketing energy costs over the next few years.

DISCLAIMER: This article is not investment advice and represents the opinions of its author, Elliott Gue. The Free Market Speculator is NOT a securities broker/dealer or an investment advisor. You are responsible for your own investment decisions. All information contained in our newsletters and posts should be independently verified with the companies mentioned, and readers should always conduct their own research and due diligence and consider obtaining professional advice before making any investment decision.