Higher for Longer

Higher for Longer

The regime change in inflation and interest rates underway...

Bear market rallies are all about sentiment and positioning rather than economic and market fundamentals.

When the market sells off and risk of recession rises, investors tend to grow bearish and take defensive action such as raising cash, buying put options to protect against market downside, even shorting stocks outright.

While it certainly makes sense to reduce risk as the market sells off, it also sets up the stock market for a countertrend “pain” trade higher.

Simply put, any whiff of positive news that sends the market higher, even for just a few days, can be enough to prompt investors to cover shorts or reduce hedges. That, in turn, can lead to upside momentum and fear of missing out (FOMO) on further market upside as no investor wants to miss out on the big “Turn” for the markets.

That’s particularly true in 2023 thanks to fresh memories of the historic, V-shaped turn in stocks back in March-August 2020.

In that cycle, the S&P 500 set an all-time high on February 19th, collapsed almost 34% to a closing low just over a month later on March 23rd and then soared to log fresh all-time highs again by August 18th. That was the shortest bear market and the fastest recovery to all-time market highs in history dating back to at least the 1920s.

And, thanks to unprecedented, coordinated monetary and fiscal stimulus, the National Bureau of Economic Research (NBER) pegs the 2020 recession lasting just 2 months, the shortest in the history of their business cycle research dating back to June 1857.

Think about it from the perspective of an active fund manager sitting on a sizable cash position as of the end of 2022 -- if the market takes off like it did back in 2020, would you really want to sit on the sidelines in cash, all-but-guaranteeing underperformance relative to your benchmark?

Given the proliferation of V-shaped moves driven by changes in Fed policy over the past 15 years – late 2018 and early 2020 being just the two most recent – it’s not totally unreasonable to fear missing out on a market melt-up.

The Shredding Bull Narrative

Of course, while investor positioning and fear of missing out are the real drivers of bear market rallies, that’s not a very satisfying rationale for a rally, so the talking heads in the financial media typically seek to justify these moves with some sort of fundamental narrative.

In late week’s update “The Bear is in Hibernation,” I highlighted the 3 bullish pillars that have been driving the upside so far this year:

1. There’s a possibility the US economy could avoid a hard landing (recession) in 2023.

2. Inflation has peaked for the cycle and should continue to recede, allowing the Federal Reserve to pause after 1 or 2 additional hikes, then begin cutting rates to support economic growth by the end of 2023.

3. Last year’s market declines mean stocks have already priced in all the bad news on corporate earnings and economic headwinds, so investors view further dips as an opportunity to buy at attractive prices.

It bears repeating that I have serious doubts about all 3 of these pillars; indeed, I offered some counterpoints to each in last week’s issue.

Over the past week, points 2 and 3 were further shredded by market and economic realities.

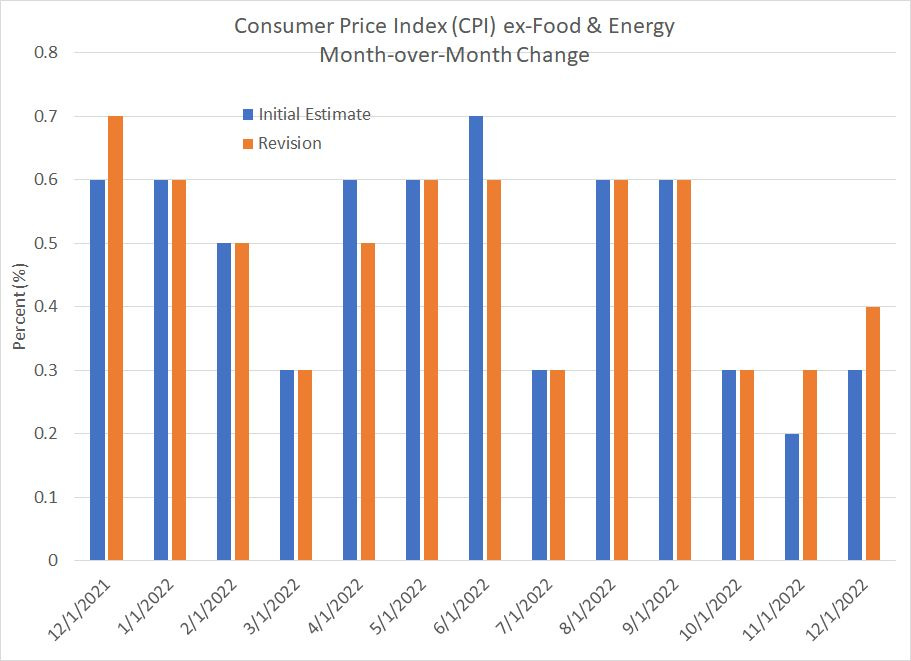

In particular, the Bureau of Labor Statistics (BLS) extensively revised the Consumer Price Index (CPI) over the past year, drawing the nascent disinflationary trend into some question:

Source: Bloomberg

This chart shows the month-over-month change in core CPI (excluding food and energy prices) since December 2021. As you can see, initial CPI data showed core CPI falling to 0.2% in November 2022, the lowest monthly gain since August 2021 and then rebounding only slightly to 0.3% in December 2022.

However, with last week’s revisions, BLS has revised higher data for each of the past two months by 0.1% -- suddenly, the year-end 2022 core disinflation looks more like a short term dip and rebound than a steady trend lower.

Indeed, the December 2022 CPI jump of 0.4% at the core (actually 0.3993% unrounded) annualizes to about 4.9%, more than double the Fed’s target.

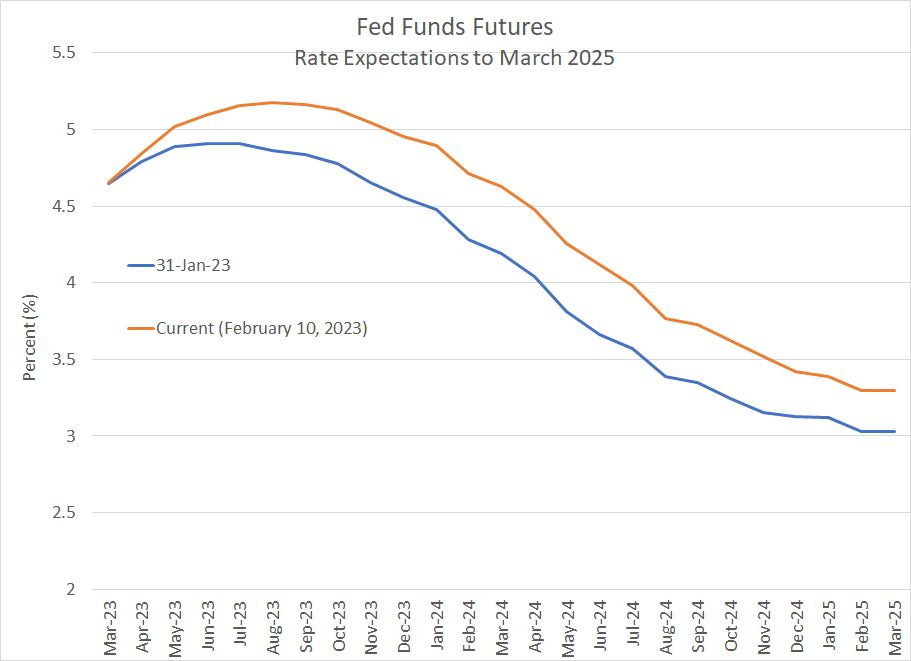

Small wonder traders ramped expectations for Fed tightening over the next few years:

Source: Bloomberg

This chart shows the Fed Funds Rate priced into Fed Funds futures between March 2023 and March 2025 both on January 31, 2023 and midday on Friday the 10th.

As you can see, at the end of January traders were pricing in a peak Fed Funds rate of 4.91% for this cycle by March or April this year, followed by around 35.5 basis points in cuts (one to two 25 basis point cuts) by the end of 2023. Less than two weeks later, markets are now pricing in a peak Fed funds rate of 5.175% by this summer with a less than even shot the Fed then cuts once by year-end.

Indeed, over the past few days there’s been a surge in open interest in put contracts on the Secured Overnight Financing Rate (SOFR) futures contracts for later this year. Simply put, there seem to be at least some trades in significant size forecasting a scenario where the Fed is forced to hike rates all the way to 6% this year in an effort to quell resurgent inflation.

In my view it remains inconsistent to bet on a soft landing for the US economy AND a near-term pivot in rates.

Last week, traders appeared to be worrying about the potential for more rate hikes, resurgent inflation, and economic growth. However, the bigger risk in my view remains recession before year-end and a major sell-off in the broader market driven by deteriorating corporate profitability.

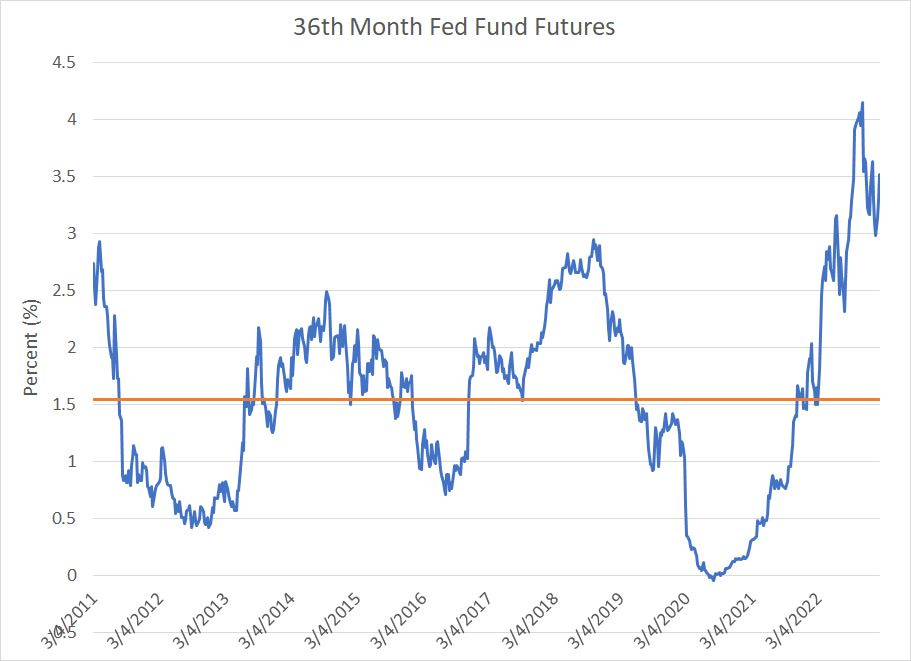

Regardless, there is one more fascinating longer-term shift in market expectations that’s underway:

Source: Bloomberg

This chart shows market expectations for the Fed Funds Rate 36 months in the future (3 years) since 2011.

For example, right now the March 2026 futures are pricing in a Fed Funds rate of about 3.52%. The orange line represents the long-term average since 2011 is about 1.54%.

Simply put, the era of near-zero rates and subdued inflation is over.

As you can see from my chart, since 2011 traders have tended to price in Fed hikes when the economy looked strong, such as in early 2011, late 2014 and late 2018. However, even at peak hawkish, market expectations for the peak Fed funds rate over the ensuing 3 years never rose above the 2.5% to 3% range.

On the other side of the equation, markets have tended to quickly price in Fed cuts at the first sign of economic weakness – the periods from 2011-13, mid-2016 and early 2019 are all examples of that. That makes some sense, because for most of this period, inflation remained below the Fed’s target, giving the central bank the luxury of prioritizing economic growth over price stability.

That’s all changed.

Since last summer, the Fed Funds futures have not just priced in more Fed hikes near term, but a much higher plateau for the Fed Funds rate in coming years of 3%+.

This suggests markets believe the Fed will eventually cut when the economy weakens, but persistent inflationary pressures will forestall the sort of dramatic monetary stimulus equity markets have enjoyed in the post financial crisis era.

This represents a regime change for markets with massive long-run implications.

The era of low interest rates, low inflation and rapid policy response to every shift in the business cycle is now over and the era of higher-for-longer rates, above-target inflation and waning central bank influence on markets is now underway.

For equity market investors the biggest implication is there’s a multi-year shake-up in the stocks, investment styles and sectors most likely to beat the S&P 500.

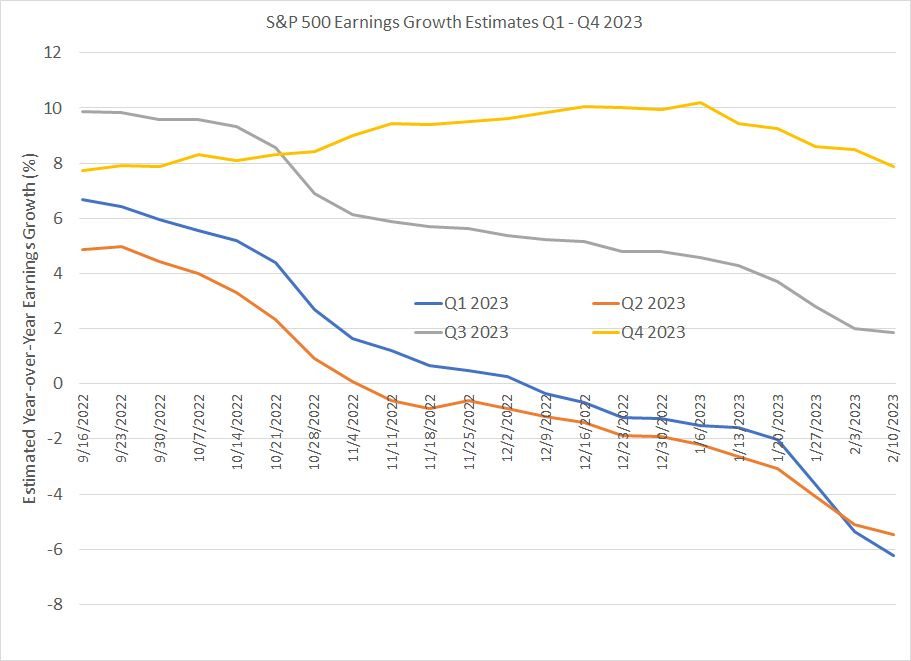

Meanwhile, the idea markets are “pricing in” a mild recession and decline in earnings strikes me as optimistic given downside revisions remain a moving target:

Source: Bloomberg

Since the end of 2022, market expectations for Q1 2023 earnings for the S&P 500 have been revised lower from -1.3% to -6.2%, while estimates for Q2 2023 earnings have been downgraded from -1.9% year-over-year to down 5.5% year-over-year.

And since Q4 2022 earnings season kicked off in earnest back in mid-January, the downside revisions have spread into the second half of 2023 — Q3 2023 earnings earnings growth is now forecast at less than +2%, half of the expected growth rate in late December.

Of course, as I said at the start of today’s issue as well as in last week’s commentary, the Bear is in Hibernation, the fundamentals don’t matter much in the short-run as bear market rallies tend to be driven more by investor sentiment and positioning rather than economic and market fundamentals. Ultimately, markets will react to the deterioration in corporate earnings and the economy; however, the path of least resistance remains higher for now.

Measuring sentiment and investor positioning is an imprecise and notoriously difficult task; however, later this week I’ll outline a handful of indicators I watch.

To make sure you receive my twice-weekly economic, market and stock commentary free of charge, sign up for The Free Market Speculator by typing your e-mail in the box below:

DISCLAIMER: This article is not investment advice and represents the opinions of its author, Elliott Gue. The Free Market Speculator is NOT a securities broker/dealer or an investment advisor. You are responsible for your own investment decisions. All information contained in our newsletters and posts should be independently verified with the companies mentioned, and readers should always conduct their own research and due diligence and consider obtaining professional advice before making any investment decision.