Oil's Recession Warning

Oil's Recession Warning

What oil says about the health of the global economy

Here’s a question I’ve received a lot lately:

Why are oil prices so weak?

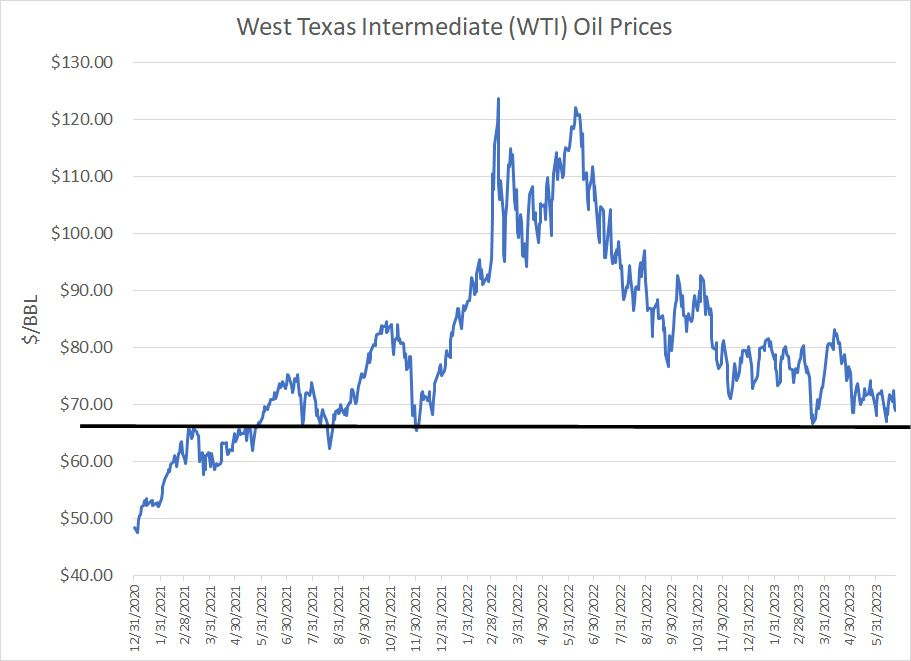

Whether you care to watch Brent or West Texas Intermediate (WTI), prices are not only down sharply from last year’s peak, but also barely holding long-term support levels:

Source: Bloomberg

For WTI this roughly $63 to $68/bbl region I’ve marked on the chart acted as resistance for crude in early 2021 and support since the middle of the same year.

So far in 2023, we’ve tested that region on multiple occasions.

Supply, Demand and the “Call on OPEC”

Yet, step back from the chart for a moment, and the supply-demand balance in oil markets looks healthy and likely to tighten into the second half. US total refined products supplied, a measure of demand for products like diesel and gasoline, has been above the 7-year seasonal average for 12 of the past 13 weeks.

Meanwhile, US inventories of oil, gasoline and diesel are all below the long-term seasonal averages.

The latest Oil Market Report from the International Energy Agency (IEA) forecasts 2023 global oil demand to jump 2.4 million bbl/day this year to a record high of 102.3 million bbl/day.

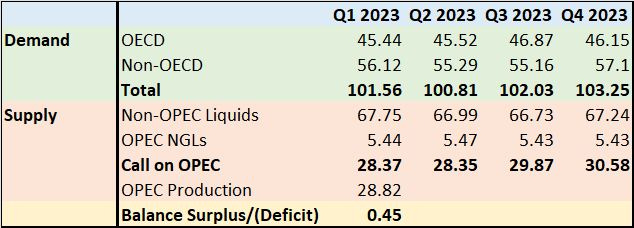

And here’s a look at OPEC’s latest forecast:

Source: OPEC June 2023 Monthly Oil Market Report

This chart breaks down OPEC’s expectations for oil supply and demand for each quarter of this year.

On the demand front, shaded in green, this table divides the world into two categories – OECD (developed) and non-OECD (emerging markets). As you can see, the cartel is looking for demand to jump from roughly 100.8 million bbl/day in Q2 2023 to 102.0 million bbl/day in Q3 and 103.25 million bbl/day in Q4.

Some of this is due to normal seasonality – 90% of the world’s population lives in the Northern Hemisphere and the summer months (third quarter) represent summer driving and travel season, a period of peak demand for oil.

There’s a second important component. You can see demand for oil in non-OECD countries like China and India is expected to see a dramatic increase from Q2 to Q4 2023, even larger than the normal seasonal uplift. That’s primarily a result of expectations for a recovery in Chinese crude oil demand as the economy reopens.

Indeed, oil demand reached a record high of 15.1 million bbl/day in China for the month of April 2023:

Source: Bloomberg

Now, let’s flip over to the supply side highlighted in red on my table. As you can see, this category is broken down into non-OPEC production (production from countries like the US, Brazil and even Russia) as well as OPEC natural gas liquids (NGLs). The reason OPEC breaks out NGLs production from within the cartel is that some NGLs output is not subject to OPEC production management quotas.

That leads us to the “Call on OPEC” category. Basically, this is the amount of oil OPEC would need to produce each quarter to balance the market – the calculation is simply total oil demand less non-OPEC production and OPEC NGLs production.

If OPEC produces more than the “call,” the global oil market is in surplus, and you can expect global oil inventories to rise. All things equal, an oil market in surplus is bearish and the consequent rise in global inventories is bearish crude.

The opposite applies to a deficit – if OPEC produces less than the “call,” the implication is that oil-consuming countries would need to draw down inventories to meet demand and falling inventories are likely to act as a tailwind for prices.

As you can see, in Q1 the call on OPEC was 28.37 million bbl/day and the cartel produced 28.82 million bbl/day, which means the global oil market was oversupplied to the tune of about 450,000 bbl/day. However, look at how the call is projected to evolve over the course of the next 3 quarters.

In Q2 – the current quarter – the “call” is roughly flat with Q1 because seasonally low demand in Q2 is offset somewhat by an expected decline in non-OPEC production. Some of that is the result of seasonal maintenance and normal weather-related production disruptions in Q2.

However, OPEC also revealed that the cartel’s production was 28.773 million bbl/day in March, 28.529 in April and 28.065 in May 2023. This decline in OPEC production is largely the result of announced production cutbacks with steeper production cuts phasing in starting on May 1st. The implication here is OPEC production was above the “call” in March and April, but fell below the “call” by May 2023. That suggests global oil inventories should have begun to draw down in May-June.

Now, let’s step this analysis forward. Saudi Arabia announced a unilateral production cut of 1 million bbl/day in July 2023 and it’s quite possible the country will decide to extend that cut through the rest of the year, especially if Brent oil prices remain below that $80/bbl region.

This implies OPEC production falling further from that 28.065 million “marker” by July 2023. A drop to 27.5 million bbl/day on average in Q3, for example, would imply an oil market undersupplied by some 2.3 million bbl/day for Q3 2023 alone.

Of course, the situation would grow even more dire into yearend should OPEC’s estimates of a Q4 2023 “call” of almost 30.6 million bbl/day prove valid. Should the oil market truly face a deficit of 2+ million bbl/day in Q3 and Q4, or even 1 million bbl/day, that would be unequivocally bullish for oil prices into the second half of the year.

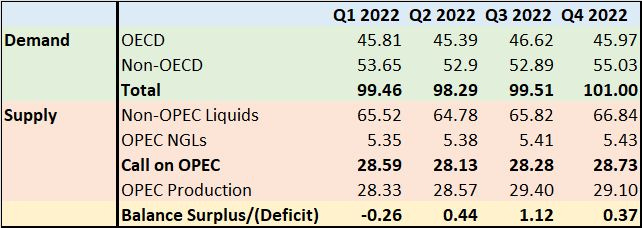

Here’s a table showing OPEC’s estimates for how the oil market evolved in 2022:

Source: OPEC June Oil Market Report

Last year, based on OPEC estimates, the oil market was actually oversupplied in every quarter except Q1 2022; yet, oil prices still spiked into the summer based on fears Russia’s invasion of Ukraine would disrupt the supply side of the equation.

In the second half of this year, however, there’s real risk of a real supply-demand balance based on OPEC’s estimates that would result in an unsustainable draw on global commercial oil inventories.

Thus, the outlook for oil supply and demand into H2 2023 from OPEC – and broadly similar estimates from IEA – do NOT match the reality on the ground of oil testing multi-month lows in the $60’s/bbl for WTI and low $70’s/bbl for Brent.

There are two possibilities:

The oil market is “wrong,” and we will see a massive rerating of prices higher into H2 2023 as demand picks up, and OPEC supply is inadequate to cover the “call” and fill the gap.

Alternatively, OPEC and IEA are wrong, and their demand estimates are way off for H2 2023. Should the expected H2 2023 demand surge not materialize that would put the Call on OPEC well below the 29.9 to 30.6 million bbl/day estimates outlined in OPEC’s June release.

Non-OPEC supply simply can’t adjust higher fast enough to drive a second half glut of oil that would account for the discrepancy between official estimates and the current price action in global oil markets.

So, the only scenario I can see that could forestall the OPEC-projected tightening of the oil supply/demand balance into H2 2023 enough to account for current lackluster crude oil price trends is a global recession that drives down demand.

In my view, oil prices do not have significant downside risk from the current quote unless the recession proves far more severe than anything currently anticipated. Saudi’s unilateral cut starting July 1st suggests the Kingdom is looking to support oil prices even if that means there’s a hit to their oil revenues in the short run.

However, when given the choice of betting the oil market is right or the IEA and OPEC are right about the global economy, I’ll always side with the collective knowledge of the millions of traders who comprise the market.

There’s also a major discrepancy between the message in commodity and equity markets right now.

Something has (still) got to give – either the global economy is a lot weaker than current trading in equity markets suggests and oil prices are simply reflecting a likely collapse in demand in H2 2023. Alternatively, the calls for a global economic “soft landing” are correct, OPEC and IEA estimates for a surge in demand materialize and crude oil is a screaming bargain right now.

DISCLAIMER: This article is not investment advice and represents the opinions of its author, Elliott Gue. The Free Market Speculator is NOT a securities broker/dealer or an investment advisor. You are responsible for your own investment decisions. All information contained in our newsletters and posts should be independently verified with the companies mentioned, and readers should always conduct their own research and due diligence and consider obtaining professional advice before making any investment decision.