Powell: A Dove in Hawk’s Clothing

Powell: A Dove in Hawk’s Clothing

The Federal Reserve announced an expected 25 basis point hike in interest rates last Wednesday.

The accompanying statement, and Powell’s comments at the press conference, were undeniably hawkish. Highlights included a revision to the Fed’s so-called dot-plot projections showing its target rate at 1.875% by the end of 2022, rising to 2.75% in 2023.

That largely endorses the consensus view on Wall Street just before the Fed meeting though it’s well above the central bank’s “dot plot” projections released on December 15th, which showed rates ending this year at about 0.875%, rising to 1.625% by the end of next year.

So, how did the market react to this hawkish turn?

The S&P 500 jumped 6.96% in the final four trading days last week led by the very stocks that tend to perform worst when interest rates rise -- growth stocks and the Nasdaq -- up 10.16% and 10.53% respectively.

The most logical fundamental explanation: The market simply doesn’t believe the Fed, or its Chairman Jerome Powell.

Equity and fixed income traders alike just don’t believe the Fed will be willing to raise rates far enough or fast enough to bring the current generational surge in inflation to heel.

The median of the Fed’s most recent economic projections shows PCE Inflation at 4.3% in 2022, 2.7% next year and 2.3% in 2024 compared to the central bank’s target of 2.0%.

Yet, while the central bank expects inflation to fall sharply over the next two years as it hikes interest rates, it’s looking for economic growth to remain solid, declining from 2.8% in inflation-adjusted (real) terms this year, to 2.2% in 2023 and a still above-trend 2.0% in 2024.

History suggests one or the other of these projections is wrong:

Either inflation will fall quickly to near the Fed’s long-term target at the cost of economic growth falling well below the Fed’s current projection of 2% by 2024.

Or inflation will remain elevated relative to the central bank’s current expectations because Powell and the Fed will ultimately panic as rising rates hit economic growth and the stock market, prompting an earlier-than-anticipated end to any tightening regime.

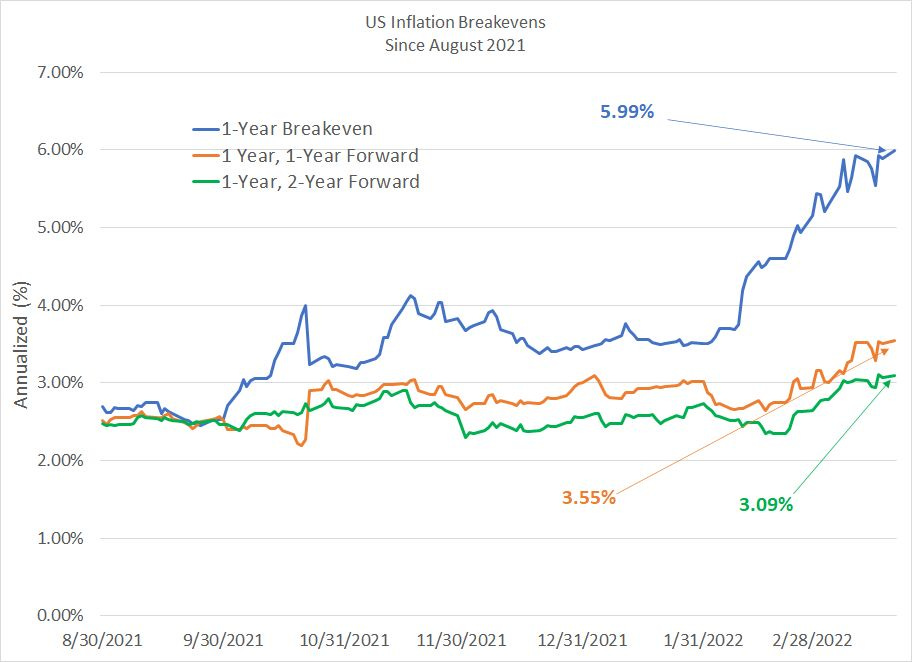

The market is betting on the latter outcome:

Source: Bloomberg

I used current market pricing in the Treasury Inflation-Protected Securities (TIPS) market to calculate the market’s expectations for inflation over 3 different time periods – the next year, inflation over the one-year period starting 1 year from today and inflation over the 1-year period starting two years from today.

As you can see, the TIPS market is currently pricing in inflation of just under 6% over the next year (3 times the Fed target) and inflation of 3.55% over the 1-year period starting in March 2023 and 3.09% for the one-year period starting in March 2024.

This point is crucial:

In all three cases, market inflation breakevens are higher than prior to last week’s Fed meeting and at the highest levels of the current cycle.

In other words, despite last week’s Fed rate hike and a more hawkish-than-expected statement and press conference, the market is pricing in much higher average inflation than it was before the Fed news.

The TIPS market uses the Consumer Price Index (CPI) to calculate inflation while the Fed’s preferred measure is the core Personal Consumption Expenditure (PCE) deflator. These measures are not the same for several reasons including that the core PCE excludes the impact of food and energy prices.

Nonetheless, even assuming a healthy contribution to CPI from food and energy prices, the market’s projection of 3.55% annual inflation over the 1-year period starting in March 2023 looks well above the Fed’s own projection for 2.7% inflation for the entirety of 2023.

Similarly, the Fed’s 2.3% median forecast for 2024 inflation is some 0.8% below the market’s inflation expectations for the period from March 2024 to March 2025.

In short, the market is betting Powell is a dove in hawk’s clothing who will ultimately be willing to tolerate higher-for-longer inflation, delivering yet another easy-money bump for the Nasdaq and growth stocks much like the experience of late 2018 and early 2020.

I’m just not sure the outcome for stocks will be as sanguine this time.

After all, in late 2018/early 2019 when Powell backed off planned tightening, inflation was clearly not a problem in the US. And, in 2020, when the Fed (and US federal government) delivered record-setting peacetime stimulus, deflation looked to be the bigger risk and the market was in free-fall.

It’s difficult to imagine the Fed backing down from its current tightening plans with inflation close to 3 times its target, consumers increasingly highlighting inflation as a major worry and the S&P 500 down less than 10% from its January peak this morning.

DISCLAIMER: This article is not investment advice and represents the opinions of its author, Elliott Gue. The Free Market Speculator is NOT a securities broker/dealer or an investment advisor. You are responsible for your own investment decisions. All information contained in our newsletters and posts should be independently verified with the companies mentioned, and readers should always conduct their own research and due diligence and consider obtaining professional advice before making any investment decision.