Recession: Same as it Ever Was

Recession: Same as it Ever Was

Recessions happen gradually then suddenly...

Recessions have a dangerous habit of taking longer than the investing crowd expects to get started only to turn dangerous more quickly than almost anyone anticipates.

Take the 2001 recession and the 2000-02 bear market in the S&P 500 as an example.

With the benefit of hindsight, it might seem obvious the stock market was overvalued in 2000 and speculation was rampant. Investors of a certain vintage will recall anecdotes of stock market excess of that era such as the meteoric rise and fall of online pet retailer “Pets.Com,” or the Ameritrade brokerage advertising featuring “Stuart,” a slacker office worker who encourages his boss to buy stocks online at the height of the dot-com craze.

It might also seem logical to suppose the corporate spending binge on technology and networking in the late 1990s might eventually subside, leading to a recession, as it did by early 2001.

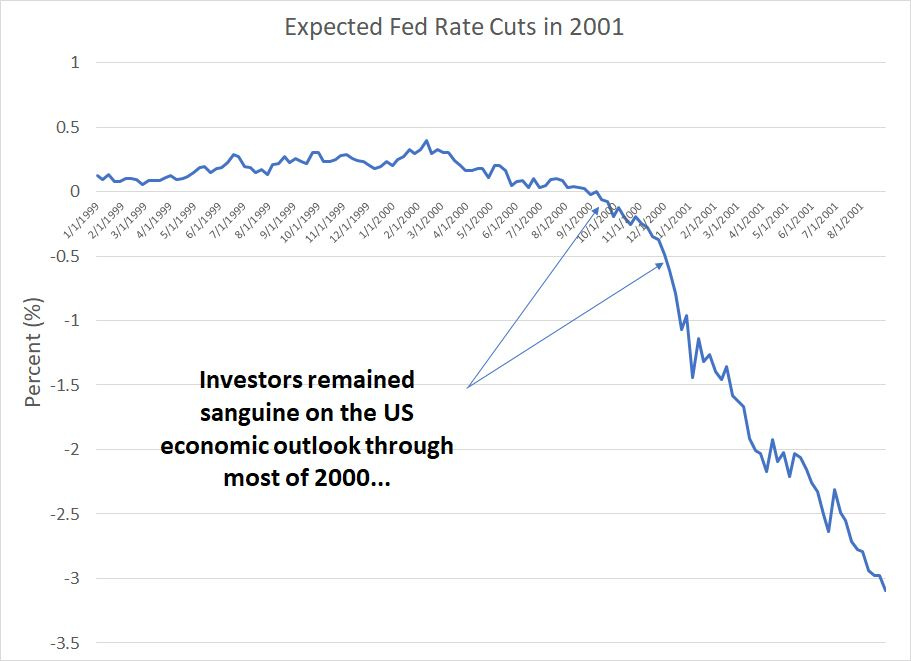

However, dig a little deeper and you’ll find Wall Street remained sanguine on the economic outlook for most of 2000, more than 6 months after the stock market peaked in late March of that year:

Source: Bloomberg

To create this chart, I examined Eurodollar futures contracts for December 2000 and December 2001 from the beginning of 1999 through August of 2001.

The recently retired Eurodollar futures contract was a short-term interest rate benchmark, and the chart above shows the expected change in short-term interest rates in the year 2001 – negative numbers suggest the Fed was expected to cut rates between December 2000 and December 2001 and positive numbers point to Fed rate hikes.

As you can see, from the beginning of 1999 through the middle of September 2000, Eurodollar futures were looking for the Fed to maintain interest rates at around 6.5%, which was the upper end of the Fed funds target from May through December of 2000.

Indeed, up until the beginning of September, the market saw a higher probability the Fed would hike rates again at some point in calendar year 2001 rather than being forced to cut rates to address spreading economic weakness.

As late as mid-November 2000, traders were only penciling in a single 25-basis point cut to the Fed funds rate through the entirety of 2001 despite growing evidence of economic deterioration.

Just look how quickly trends changed – in early January 2001, Fed Chairman Alan Greenspan announced a 50-basis-point intermeeting cut and followed that up with a second 50 basis point cut in early February. By the middle of March 2001, the month the US recession officially started, Eurodollar futures were pricing in almost 200 basis points (2%) of cuts by the end of 2001.

In other words, over a period of 4 to 6 months market expectations moved from forecasts for a robust economy in 2001 and, perhaps, the need to further hike interest rates to forecasts for 200 basis points worth of cuts amid a deepening recession.

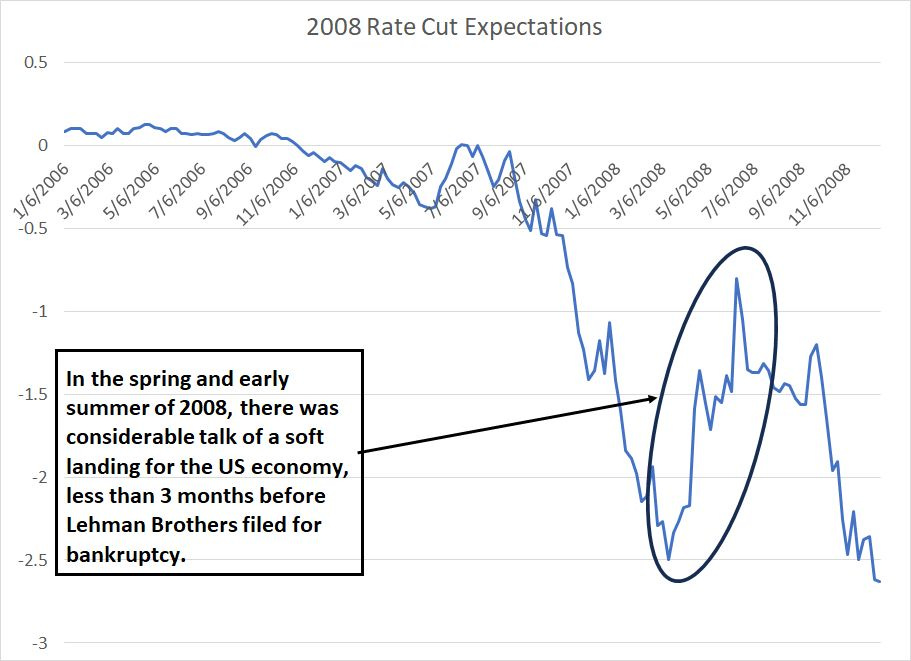

The same basic pattern was evident in the lead up to the far more severe Great Recession and financial crisis of 2007-09:

Source: Bloomberg

This chart shows expected Fed rate cuts in calendar year 2008 starting at the beginning of 2006 through to the end of that year.

From the summer of 2006 through to September of 2007, the high end of the Fed Funds target range stood at 5.25%. And up until about mid-2007, even as stress in the financial system and residential housing markets became apparent, Eurodollar futures weren’t looking for the Fed to embark on a major rate-cutting campaign in 2008.

That started to change when the Fed cut rates 50 basis points in September 2007 and followed that move with a 25-basis point cut in October and another 25 basis points in December, bringing rates down a total of 1% in just 3 months.

Market expectations for the economy began to deteriorate rapidly in early 2008. By March, the market had priced in 225 basis points of additional cuts from the year-end 2007 level of 4.25% through December 2008.

But just look at that move between March and June 2008 I’ve circled on the chart. Simply put, a wave of economic optimism in the spring and summer of 2008 prompted traders to downgrade the potential for additional monetary easing while soaring crude oil prices raised concerns of rising inflationary pressures.

Just consider: In early May 2008, the Fed cut interest rates to 2% and held rates at that level until the central bank cut rates by 50 basis points in early October of the same year. By June 2008, however, the Eurodollar futures were pricing short-term rates as high as 3.70% by December 2008.

In other words, for a time, right in the middle of what’s arguably the worst year for the US economy since the 1930’s, market participants thought the Fed might be able to HIKE rates before yearend.

Indeed, it wasn’t just Wall Street that saw diminished probability of a US economic downturn and further rate cuts. The Summary of Economic Projections prepared by the Fed at its meeting on June 24-25, 2008, actually upgraded real (inflation-adjusted) GDP growth for the US economy for the year to 1.0% to 1.6% from its April range of 0.3% to 1.2%. The consensus at the Fed was that real economic growth would rebound to north of 2% in 2009 and 2.5% to 3.0% by 2010.

The minutes from that Fed Meeting included this gem of a sentence:

With increased upside risks to inflation and inflation expectations, members believed that the next change in the stance of policy could well be an increase in the funds rate; indeed, one member thought that policy should be firmed at this meeting.

Source: Federal Reserve Minutes of the June 24-25, 2008 Meeting

And that brings US to the current situation:

The Outlook for Rate Cuts in 2024

On November 4, 2022 the Secured Overnight Funding Rate (SOFR) futures market, the successor to the Eurodollar Futures, was pricing in short term interest rates near 4% as of the end of 2024.

Some nine months later on August 4, 2023 SOFR futures were pricing in a year-end 2024 rate of 4% and today it’s at around 4.50%. So, expectations for the level of rates as of the end of next year really haven’t changed a great deal since last autumn.

Market expectations for interest rates at the end of 2023 have bounced around a bit this year; however, the market has been consistent in expecting the Fed to keep rates elevated for a time to quell inflation in 2023 followed by significant rate cuts next year.

If we look at Fed Funds futures as today, the market is pricing in 48% probability the Fed hikes rates once more by 25 basis points this year to 5.75% at either their November 1st or December 13th meeting. Futures see near-zero probability the Fed will make a move at its meeting next week. The market then sees the Fed cutting rates by around 100 basis points (1%) by the time of its December 18, 2024 meeting.

Since June, the market has actually reduced expectations for 2024 rate cuts, presumably because of increased confidence in the economic outlook and concerns about resurgent inflation due to, among other things, the recent surge in crude oil prices.

At its last meeting, the Fed’s own staff economists removed previous forecasts for a US recession and, as I noted in August, a host of Wall Street banks have reduced the probability of recession over the next 12 months. Soft landed is not the consensus for most asset managers surveyed by Bank of America as part of its monthly Global Fund Manager’s survey.

Recall that this is the same pattern we saw in 2000-01 and 2007-08.

Specifically, there is no gradual change in market expectations in favor of recession over soft landing. Rather, markets tend to remain optimistic about the economy until there’s a shift or catalyst that prompts a sudden, unmistakable jump in recession probabilities and a corresponding change in the outlook for monetary policy.

Let’s overlay current expectations for 2024 Fed rate cuts against the experience in 1999-01:

Source: Bloomberg

Much like the first 9 months of 2000, expectations for year-end 2024 interest rates have remained rangebound for most of this year.

However, the 2000 experience illustrates this period of relative calm, and the sanguine economic outlook in global markets right now, can shift to near-certain recession and Fed rate cuts in a matter of just a few weeks.

Don’t be fooled by all the talk of Goldilocks, resurgent corporate earnings and “No Landing” – recessions usually start in this way and the consequent stock and bond market shifts can be breathtaking.

In the Long Run, We’re All Dead

A century ago, in 1923 British economist John Maynard Keynes wrote:

“The long run is a misleading guide to current affairs. In the long run we are all dead.”

Back in the late 1990s, early in my career, I remember reading commentary from several market gurus calling for a crash in the stock market, led by the Nasdaq and technology. They were right, but way too early.

And, in early 2000, long-time stock market bear Julian Robertson shuttered his Tiger Management hedge fund amid poor returns and capital outflows. Tiger was once one of the largest hedge funds in the US with some of the best long-term risk adjusted returns and, for many years through the mid 1990s, investors were eager to buy in.

Of course, Tiger made the decision to close its doors, and investors lost confidence in Tiger’s bearish outlook, literally days before the Nasdaq’s infamous March 2000 peak.

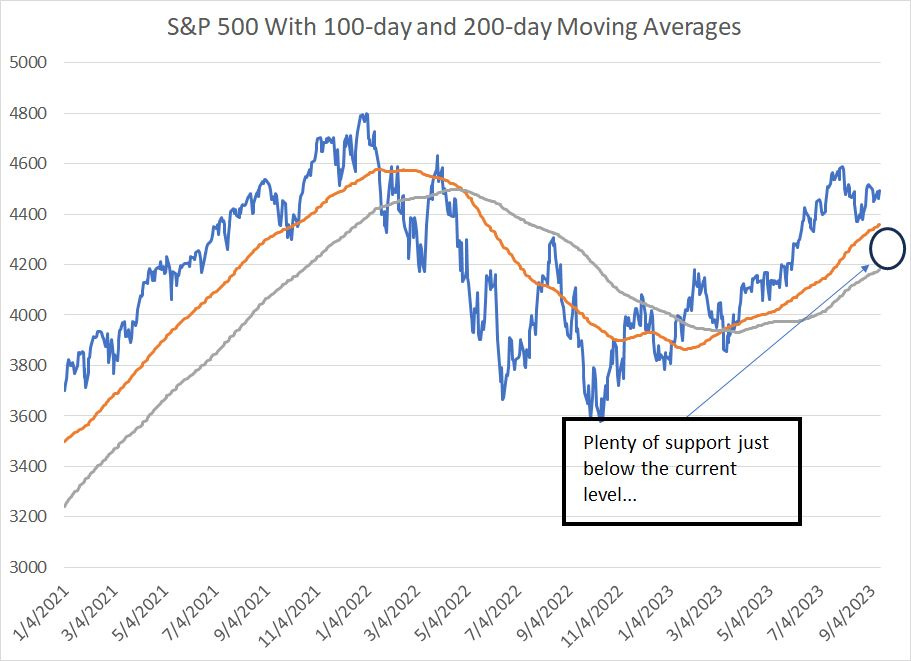

My point: it’s possible to be entirely correct about the long-term path of the stock market, and the health of the economy, and still lose money in the short term. We don’t want to fall into that trap and, right now, the technical picture for the market remains bullish:

Source: Bloomberg

I’ve posted this chart on several occasions in the past few months and it’s worth posting again.

The S&P 500 pulled back a total of 4.8% from its July 31st closing peak to its mid-August closing low and, as you can see in the chart above, the market held above key support defined by its 100-day and 200-day moving averages. Corrections of this magnitude are common – pullbacks of 5 to 10 percent on a closing basis occur around 2 to 3 times each year on average.

In addition, August and September are seasonally two of the weakest months of the year for the broader stock market from a seasonal perspective, so it’s not unusual for the stock market to see a correction in this period that’s followed by a year-end rally.

I continue to believe we’ll see more downside for the stock market and will undercut the October 2022 lows amid signs of broadening economic weakness. However, that’s an intermediate to long-term view – the current situation recalls a second, famous quote from John Maynard Keynes:

“Markets can remain irrational longer than you can remain solvent.”

With that in mind, I’m recommending a few adjustments to the model portfolio this week:

Keep reading with a 7-day free trial

Subscribe to The Free Market Speculator to keep reading this post and get 7 days of free access to the full post archives.