Soaring Gasoline Prices: Who's to Blame?

Soaring Gasoline Prices: Who's to Blame?

Is it "Greedy" Big Oil Companies?

On June 10th during a visit to the Port of Los Angeles President Joe Biden stated:

We’re going to make sure everyone knows Exxon’s profits. Exxon made more money than God last year.”

The reason they’re not drilling is that they’re buying back their own stock., which should be taxed quite frankly, buying back their own stock and making no new investments…

Source: Dallas Morning News

And, in a June 14th letter to executives at seven large energy companies including Chevron (NYSE: CVX) and Exxon Mobil (NYSE: XOM), President Biden wrote:

But at a time of war, refinery margins well above normal being passed directly onto American families are not acceptable.

There is no question that Vladimir Putin is principally responsible for the intense financial paid the American people and their families are bearing. But amid a war that has raised gasoline prices more than $1.70 per gallon, historically high refinery profit margins are worsening that pain.

And that brings me to a point you’ve probably been hearing and reading a lot recently particularly from politicians:

With oil and natural gas prices soaring, why aren’t US producers drilling more aggressively and why isn’t the industry spending more to produce more and build out additional refining capacity to ease high gasoline prices?

In many developed countries, these questions coupled with the recent commodity-driven surge in energy industry profits have led to proposals for windfall profits taxes – an additional tax on energy companies in one form or another.

There are many answers to these questions; however, it’s useful to step back and consider one over-arching point – the energy business is extremely cyclical:

Source: Bloomberg

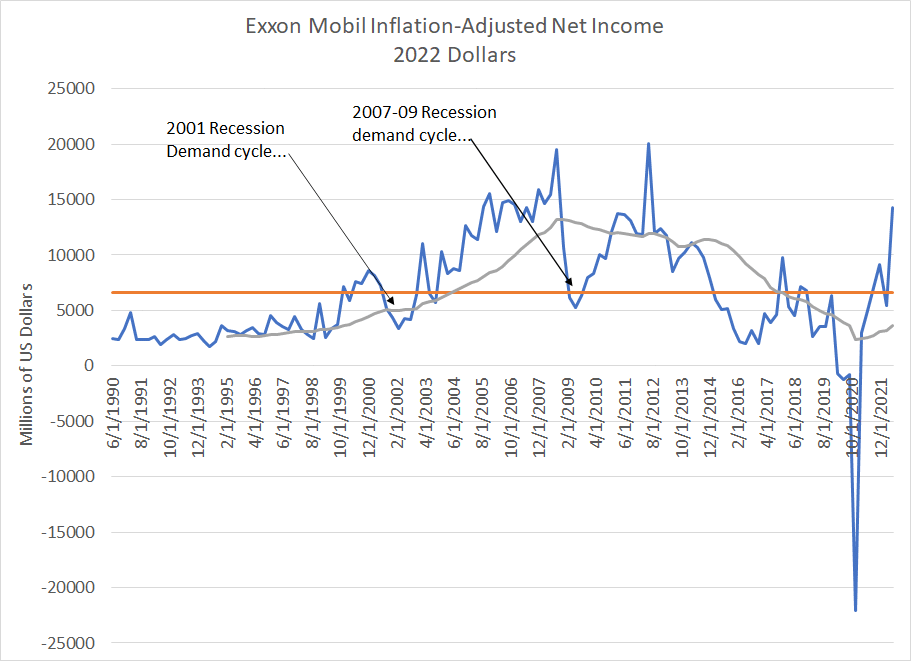

To create this chart, we examined quarterly net income (profit) for Exxon Mobil (NYSE: XOM) since June 1990 (about 32 years). Rather than reporting nominal figures, which are meaningless because $1 billion in 1990 is a very different thing than $1 billion today, we’ve adjusted these net income numbers using the CPI Index.

Thus, all the quarterly profit figures are re-based to March 31, 2022 US dollar terms.

Two points jump out.

First, while Exxon’s quarterly profits figures have jumped recently, and current analyst estimates show Q2 2022 net income at about $14.7 billion dollars, the company’s quarterly profits since late 2014 have generally been BELOW the long-term average.

And look at that 20 quarter – five year – moving average of quarterly profits.

That line has been declining since the 2007-09 period and recently reached levels not seen since the mid-1990s.

And, while XOM could make $13 to $15 billion per quarter over the next several quarters, the company lost an inflation-adjusted $22.08 billion in the fourth quarter of 2020 alone amid the coronavirus commodity price collapse and global COVID lockdown demand destruction.

Second, we look at this chart in terms of four distinct phases or cycles.

The first from the late 1980s up until 1999-2000 was an energy downcycle – commodity prices were relatively low, and the energy market was glutted. In a March 6, 1999 cover story “Drowning in Oil,” The Economist magazine even predicted that a persistent glut of oil could send prices down to the mid- single digits for a prolonged period of time.

However, while a commodity bear market meant low profitability for companies like Exxon, low oil prices through the 1990s also encouraged demand and discouraged capital spending on exploration and production of oil. That, in turn, led to the supply-driven commodity up cycle from the late 1990s to the 2008-2014 peaks in oil.

As oil prices (and natural gas prices) rose from the late 1990s until the 2008-2014 period, so did Exxon’s profitability alongside profits for the rest of the energy business. That’s the second phase of this chart and this up-cycle led to a boom in industry capital spending on exploration and development.

That CAPEX boom included both spending on shale production as well as investment in sources like deepwater reserves, oil sands and further development of mature basins like the North Sea.

Eventually, the boom years gave way to a downcycle for commodity prices and industry profits from late 2014 through the end of 2021.

As industry profits collapsed, so did spending on exploration and development. And while Exxon, a massive company with significant business diversification and low breakeven prices, rarely loses money, many smaller producers with more leverage and lower credit quality went bankrupt in the bust years.

Finally, what you’re seeing today – right now – is the start of the fourth energy cycle visible on my chart above. Years of underinvestment in exploration and development of new oil and gas reserves have led to a structural shortage of oil, much like what the US faced in the late 1990s.

This is a supply-led up-cycle that can only be cured with more oil supply. And the only way to see significant new oil supply is via a sustained profits up-cycle for companies like Exxon Mobil that encourages, facilitates and finances significant new capital spending just as the 1998 to 2014 upturn did.

Also note that in the last commodity supercycle from the late 1990s through to 2014, there were two prominent demand-side mini-cycles for oil. We’ve labeled both with the first surrounding the mild 2001 recession and the second around the much more severe credit crisis and recession cycle of 2007-09.

Both demand cycles brought downturns for commodity prices and industry profits in the short term, but did nothing to change the longer-term and more powerful supply-led upcycle.

Simply put, the supply side of the oil market represents the main commodity trend while demand is the noise around that trend.

So, what of current high oil prices, lack of investment in drilling and windfall profits?

One again, because the energy industry is cyclical that means that there will be periods of higher profits interspersed by periods of depressed profits.

There’s really no such thing as windfall profits for the energy business or any other cyclical group – profit up-cycles are necessary to balance out (and survive) the inevitable, prolonged downcycles.

And it also worth flipping the script and considering the role of profits in the economy.

In general, investors don’t buy a company’s stock because they want to lower gasoline prices for consumers. Investors buy a stock because, ultimately, they think the stock will earn money, pay dividends, buy back stock or, by dint of improving business prospects, enjoy a rise in the underlying stock price.

Rising energy industry profits drive increased investor interest in buying stocks like Exxon Mobil and make it easier for Exxon to borrow money. In effect, this provides capital to the industry, encouraging greater investment (CAPEX) over time.

Ultimately, it’s the profit cycle that drives the commodity supply cycle. However, it takes time for markets to work – for profits to encourage CAPEX and for CAPEX to generate durable growth in supply to meet demand – which is why supply-led cycles haver historically been so persistent, lasting many years compared to months for demand-led cycles.

This is why government policy can have negative side effects for the price and investment cycle.

For example, a windfall profits tax on energy companies such as what the UK has enacted, reduces energy industry profits and deploys that capital to reduce energy bills for consumers. The effect of that is to discourage investment in new supply (lower industry profits means less CAPEX) and encourage oil demand (by lowering effective prices). Of course, that’s a recipe for even higher prices, and a longer period of supply adjustment – such moves can prolong the upcycle.

Put in a different way: If you tax away high profits and simply allow the industry to slog through periods of massive losses like 2020, the result is less capital flowing to the industry, less CAPEX and even more extreme upswings in pricing.

In the US, higher profits for shale producers is encouraging greater drilling activity and capital spending. However, producers are clearly reluctant to press the growth button aggressively immediately after commodity prices rise – after all, should the upturn prove short-lived as in 2018, increased CAPEX leads to painful losses as prices fall back to Earth.

And, measures such as more onerous environmental regulations discourage new CAPEX and investment – after all, would you spend more money to generate long-term growth if you believe the government is hostile to your business?

Why not just return capital to your owners – shareholders including, directly or indirectly, most Americans – in the form of dividends and share buybacks?

Only after a period of consistently improved profitability and with some degree of confidence that policymakers won’t threaten long-term profitability, can CAPEX rise sustainably enough to encourage new supply.

In short, increased regulation or hostility towards the energy industry, activism targeting companies like Exxon Mobil – it’s all bullish NOT bearish for oil and gas prices because it restricts investment in supply.