Stocks are "Done" with COVID

Stocks are "Done" with COVID

Watch the Value/Growth Relationship

Coronavirus may still dominate headlines in the mainstream and financial media, but it’s no longer driving the stock market.

The relative performance of value and growth stocks is one of the most watched relationships in the stock market.

Historically, investors buy growth stocks when they’re concerned about economic growth, because these stocks don’t need a tailwind from the broader economy to show growth in earnings and sales. In contrast, the Russell 1000 Value Index is dominated by more cyclical stocks including sectors like energy, financials and industrials that benefit directly from broader economic growth.

The highest-weighted value sector is financials while the largest growth sector is information technology.

Banks historically benefit from rising short-term interest rates because rates are correlated with net interest margin on their loan books. When economic growth and inflation are rising, investors tend to anticipate higher rates and stronger net interest margins for the banks, driving the group, and the major value indices, higher.

Growth stocks, by definition, carry higher valuations – higher price-to-earnings (P/E) ratios – to reflect their faster growth rates.

Consider two stocks in the same industry: Tesla (NSDQ: TSLA) and Ford Motor (NYSE: F). The former trades at 162 times estimated 2021 earnings while the later carries a multiple of just over 13 times.

Ford is a classic cyclical value stock that benefits from stronger economic growth and higher sales of new cars and trucks. Investors value Ford mainly based on money it’s generating in profits right now over the next few years -- if I add up expected earnings per share from Ford for the years 2021 through 2026 it’s equivalent to about 76% of the current stock price.

Unlike Ford, Tesla’s current valuation is based on distant future earnings power and the projected growth in sales of electric vehicles (EVs), a market where TSLA is a leader, after 2030.

In Tesla’s case, the sum of Wall Street earnings expectations for the years 2021 through 2026 accounts for just 9% of the current price of the stock. Even if I add up all of TSLA’s earnings through 2030, the sum comes to less than one-quarter of the stock’s current market capitalization.

That means three-quarters of Tesla’s current share price is a function of profits it’s not expected to realize until after 2030!

That brings me to one of the most fundamental rules in finance, the time value of money. It’s the basic idea that $1 earned 5 or 10 years in the future is worth less than $1 earned today.

The key question: How much less?

The answer depends on what’s known as the discount factor – the higher the discount factor, the lower the present value of future cash flows. Since rising interest rates increase the discount factor – decrease the value of future earnings – they tend to depress price-to-earnings ratios for growth stocks. The effect of rising rates, and the consequent rise in the discount factor, is magnified the further you move into the future.

Thus, rising rates will tend to depress valuations for growth stocks which rely on distant future profits to support current valuations to a much greater degree than value names.

The coronavirus outbreak upended this traditional value-growth relationship.

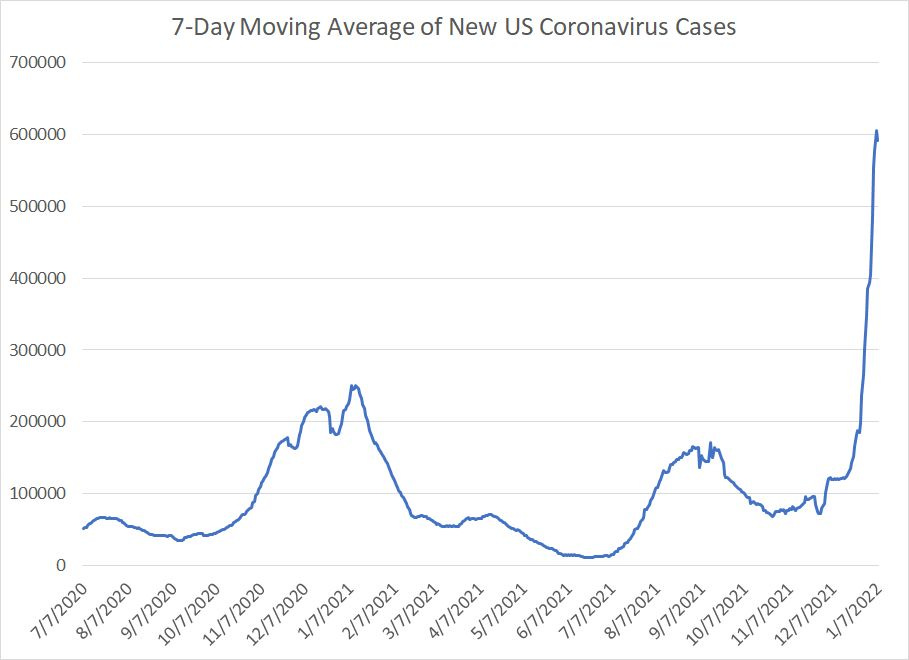

Take a look:

Source: Bloomberg

This chart shows the 7-day moving average of new coronavirus cases (positive test results) in the US.

You can see three main “surges” in US virus cases since the summer of 2020 (all dates are approximations):

1. From September 12, 2020 to January 8, 2021.

2. From June 21, 2021 to around September 13, 2021.

3. From October 26, 2021 to the present.

In the first surge, the S&P 500 was up 15.09% while the Nasdaq 100 was up 18.35%, the Russell 1000 Value Index was up 18.96% and the Russell 1000 Growth Index was up 15.96%. The ARK Innovation ETF (NSDQ: ARKK), a good proxy for the growth momentum darlings in the US market since early 2020 jumped 69.7% over this time period.

Notice that while value stocks did beat growth (by a 3% margin) over this time period, the Nasdaq 100, an index dominated by large cap technology and growth stocks, beat the S&P 500, and ARK Innovation beat them all by a wide margin.

During this first surge, expectations for US economic growth increased dramatically amid growing optimism about a raft of new fiscal stimulus from the incoming Biden Administration and the announcement and subsequent roll-out of two new coronavirus vaccines.

Rising expectations for economic growth would normally be expected to result in rising short-term interest rates (as investors sell bonds in anticipation of Fed rate hikes) and strong outperformance for cyclical value stocks. In contrast, you’d expect growth stocks to lag and for aggressive growth names – such as those in ARKK – to get hit hard.

As I outlined, that didn’t happen. Value only beat growth by a small margin and ARKK soared; meanwhile, the yield on two-year US government bonds remained roughly flat between the summer of 2020 and early 2021 and the 10-year yield increased just under 0.3%.

One likely culprit for that unusual pattern: Due to the surge in new virus cases, the Fed was widely expected to keep rates lower for longer over fears of removing stimulus too early and hitting the economy and markets. Also, many of the primary stocks in the Nasdaq 100 benefit from virus-related restrictions, helping keep growth stocks afloat.

Value finally surged as virus cases declined from early January to late June – The S&P 500 rallied 11.2% while the Russell 1000 Value Index was up 12.7% and ARKK fell more than 16%.

That brings me to the summer surge in coronavirus cases from June 21 to September 8th of last year when, despite a generally strong economic growth outlook, the Russell 1000 Growth Index jumped 10.25%, the Nasdaq 100 was up 10.6% and the S&P 500 and Russell 1000 Value indices were up just 7.16% and 1.39% respectively.

Again, the surge in virus cases trumped the fundamentals that normally should have supported value.

That brings me to the most recent “surge.” Not only has the 7-day moving average of new cases soared to the highest levels of the entire outbreak, but we have a new virus variant (omicron) that’s even more contagious and has quickly become the dominant strain in the US.

Last month, President Biden said: “For the unvaccinated, you're looking at a winter of severe illness and death for yourselves, your families and the hospitals you may soon overwhelm.”

That certainly sounds like the sort of virus surge and uncertainty that would act as a headwind for value stocks and support growth names, particularly tech stocks like Amazon.Com (NSDQ: AMZN) and Zoom (NYSE: ZM) that benefit from coronavirus containment measures. I’d posit that a statement like that from the White House last summer would have likely resulted in a pop for growth stocks.

However, that just hasn’t happened. In fact, the basic playbook since early 2020 – buy mega-cap tech and growth stocks when cases surge—has failed miserably:

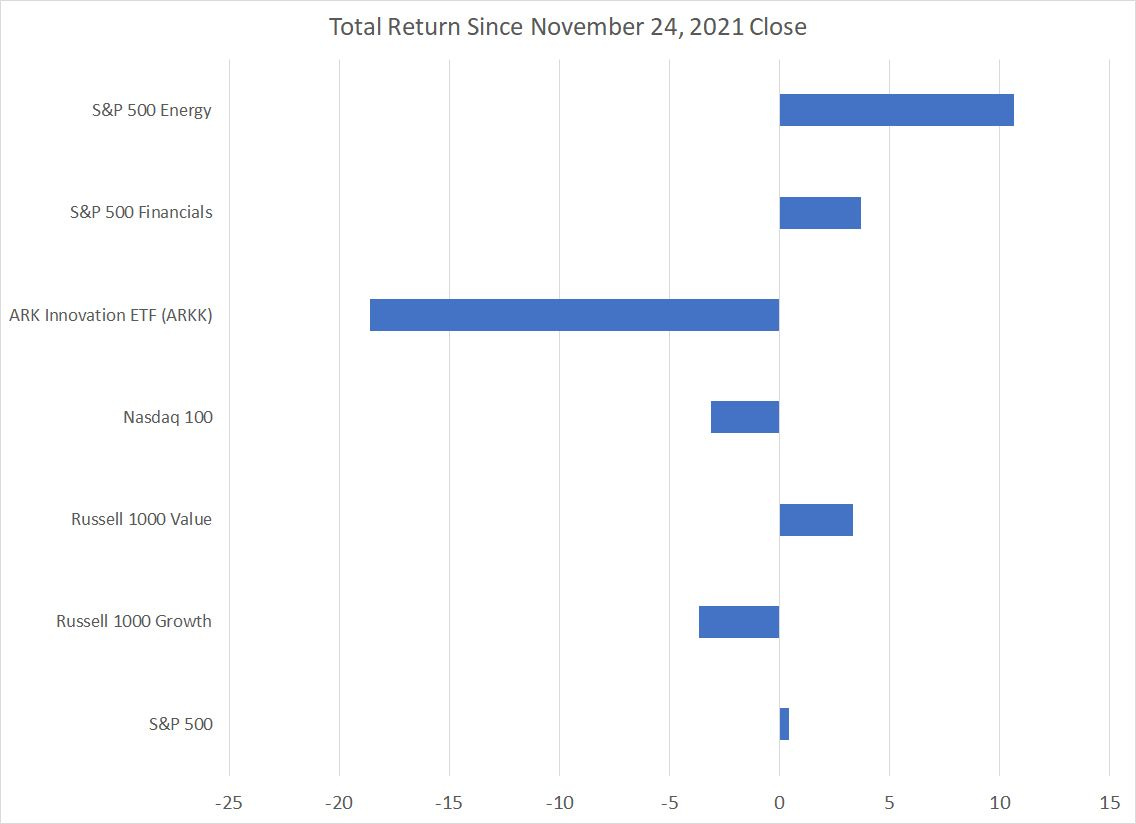

Source: Bloomberg

This chart shows the total return for various market indices since November 24, 2021, just before reports of the omicron variant hit the newswires.

Asa you can see, the Russell 1000 Value Index has jumped 3.34% since that time, besting the Russell 1000 Growth Index by more than 7 percentage points. Value and cyclical sectors like Financials and Energy have performed well while more speculative growth names, such as those in the ARK Innovation ETF, have been hit particularly hard.

Let me put this in perspective. There have been 32 trading days since November 24th and I examined 32 trading day holding periods for the Russell 1000 Growth and Russell 1000 Value Indices since 1997, a total of 6,024 rolling 32 trading day holding periods. Seven percentage points of outperformance for value over growth is a 2.4 standard deviation event – it’s highly unusual to see value stocks beat growth by this magnitude.

Put in a different way, the last time we saw value outperform growth by this magnitude was back in 2000 and 2001 when the late 90’s tech bubble was popping, setting up value for a decade of significant outperformance.

The traditional fundamentals – particularly the recent surge in interest rates – is supplanting coronavirus headlines as the key stock market driver.

That spells trouble for the market in 2022 as the Federal Reserve begins to reverse the extraordinary monetary easing put in place since the coronavirus outbreak started in early 2020.

DISCLAIMER: This article is not investment advice and represents the opinions of its author, Elliott Gue. The Free Market Speculator is NOT a securities broker/dealer or an investment advisor. You are responsible for your own investment decisions. All information contained in our newsletters and posts should be independently verified with the companies mentioned, and readers should always conduct their own research and due diligence and consider obtaining professional advice before making any investment decision.

Look forward to reading more market commentary through 2022.