The Ghost of Jackson Hole

The Ghost of Jackson Hole

The seismic shift in expectations for rates and the economy

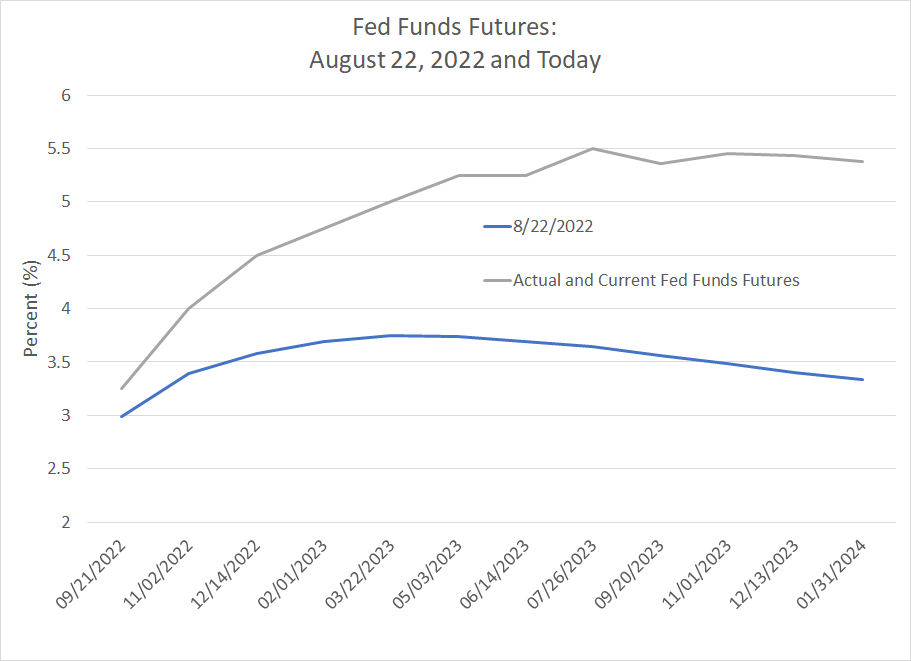

One year ago today, the Fed Funds futures market was pricing in a peak Fed Funds rate for the current cycle of about 3.75% by around March 2023, up from 2.50% at that time.

Futures market participants last summer also expected the Fed Funds rate to be around 3.40% by December 2023 (this December) implying the Fed would cut rates at least once in 2023.

That’s not how it turned out:

Source: Bloomberg

This chart shows implied rates factored into Fed Funds futures one year ago on August 22, 2022 in blue and the actual path of the Fed Funds rate over the same period in grey. The grey curve also includes current market pricing though the Fed’s January 2024 meeting.

As you can see, the Fed has been far more aggressive hiking rates than traders anticipated a year ago and one of the key events that helped shift market expectations was Fed Chairman Jerome Powell’s speech at the Jackson Hole Conference on August 22, 2022.

Among Powell’s comments last year:

History shows that the employment costs of bringing down inflation are likely to increase with delay, as high inflation becomes more entrenched in wage and price setting. The successful Volcker disinflation in the early 1980s followed multiple failed attempts to lower inflation over the previous 15 years. A lengthy period of very restrictive monetary policy was ultimately needed to stem the high inflation and start the process of getting inflation down to the low and stable levels that were the norm until the spring of last year. Our aim is to avoid that outcome by acting with resolve now.

Source: Federal Reserve Transcripts

Recall that Fed Chairman Paul Volcker was best-known for aggressively hiking interest rates in the late 70’s and early 80’s, a move that sparked a double-dip recession, but helped end the Great Inflation of the prior decade.

In short, Powell’s comments at Jackson Hole last year, coupled with similarly hawkish comments at the Fed’s press conference on September 21st, 2022, helped crush market expectations for a near-term, pause-and-pivot on rate hikes. The prevailing narrative following the Fed’s July 2022 meeting was that the central bank was “softening” its tone; Powell crushed that view.

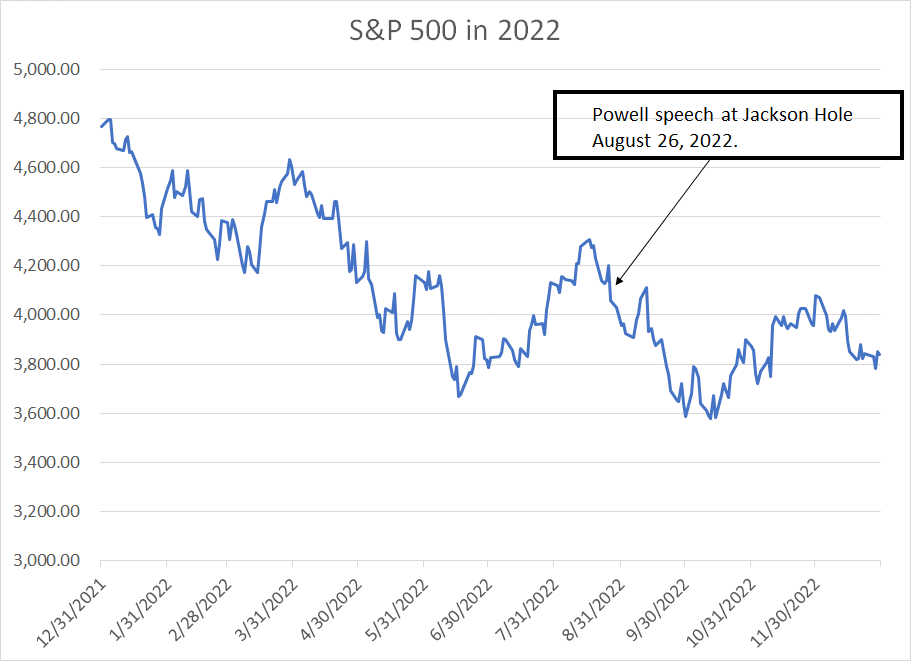

A hawkish Powell also kicked off renewed selling pressure in equities:

Source: Bloomberg

Well, it’s that time of year once again and Fed Chairman Jerome Powell will deliver a widely anticipated speech at the Jackson Hole conference this Friday August 25th at 10:05 AM Eastern Time.

What’s interesting is that market expectations today just ahead of the Powell speech are far more hawkish, and far more sanguine on the economy, than was the case one year ago. Indeed, the main driver of stock market weakness so far this month appears to be the potential for the Federal Reserve to keep rates higher for longer to restrain stubbornly high inflation, NOT an imminent economic downturn or deepening earnings recession.

Yesterday, bond yields spiked due, in part, to an article penned by an influential journalist and Fed insider at the Wall Street Journal, Nick Timiraos regarding the neutral rate of interest, a topic of widespread discussion over the past few weeks.

Simply put, the neutral rate, sometimes known simply as R* or R-Star, is the level of rates that neither stimulates nor impedes economic growth and inflation. Of course, no one can tell you with any degree of accuracy the current level of R* and it’s not constant over time. Right now, there’s some growing concern R* is much higher than it was in the 2009-2020 era following the Great Recession and Global Financial Crisis.

The implication is that current rates — the Fed Funds rate in the 5.50% region and real 10-year yields north of 2% — are not high enough and monetary policy may need to be tightened further to sustainably bring down inflation. There’s some thought Powell might discuss R* at Jackson Hole this week or allude to the need to hike rates even more later this year.

The Great Vanishing Pivot

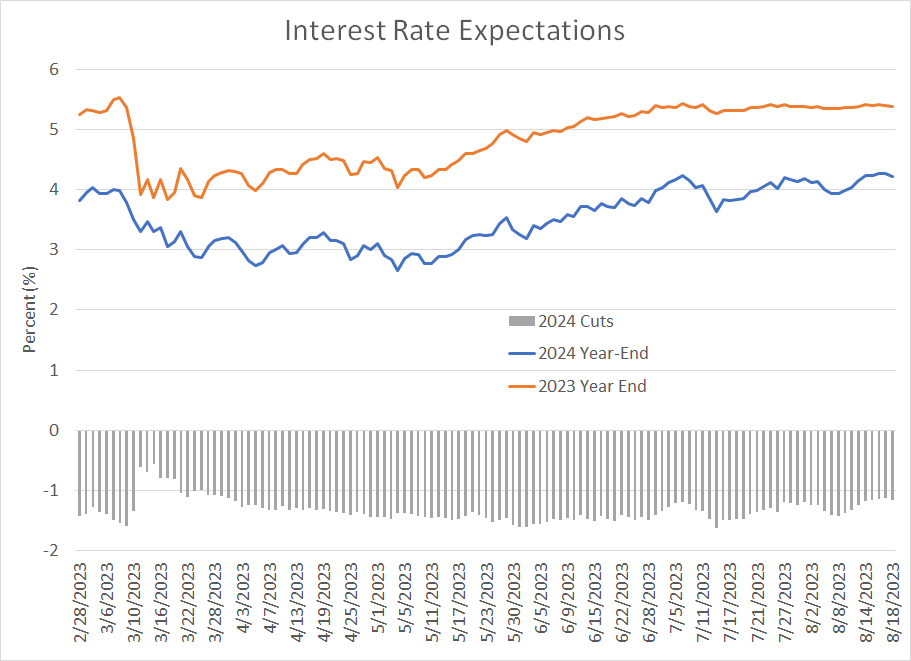

The Secured Overnight Financing Rate (SOFR) futures are pricing short-term rates of about 5.40% as of the end of this year. Those expectations haven’t changed a great deal this summer -- SOFR futures for December 2023 are roughly unchanged since the end of June.

Instead, the big shift is in expectations for Fed policy in 2024:

Source: Bloomberg

This chart presents the rates implied by SOFR futures for December 2023 in orange and for December 2024 in blue. The grey bars below the chart show the expected change in short-term interest rates through next year.

In short, as recently as mid-July, markets were looking for the Fed to cut rates by more than 160 basis points (1.6%) in 2024 compared to only around 110 basis points worth of cuts priced into markets at one point on Monday. The market now sees rates ending 2024 (next year) around 4.25%; over the past few days market expectations for year-end 2024 interest rates hit the highest levels of 2023.

Except for a brief period amid the regional banking crisis in March, when the futures market participants pared back expectations for interest rates both this year and next, expectations for a 2024 Fed “pivot” have not been this restrained all year.

The 5% World

An August 8th report from the research team at Bank of America (NYSE: BAC) was the subject of some debate and concern on trading desks over the past week. The report warned that we’re shifting from a 2% world – an era of extraordinarily low rates following the Global Financial Crisis of 2007-09 – back to a 5% interest rate world.

Generally, I agree with that thesis. Indeed, many of the factors cited in the BofA report are points I’ve also covered extensively in these weekly missives including the potential for years of underinvestment in new natural resource projects to result in chronic supply shortages, and waves of inflation, in commodities like oil, natural gas and copper.

I’ve also argued that overly aggressive energy transition targets — transition to alternative energy and away from fossil fuels — has exacerbated this problem by further discouraging investment in new fossil fuels productive capacity.

A second issue is the US government’s massive spending and debt issuance, something I wrote about extensively just last week in “How About Those Bonds?”

There remains serious risk rising government borrowing and debt service costs crowd out private investment, resulting in less robust economic growth over the long haul.

Historically, governments have sought to lean against the business cycle – spending more to stimulate growth amid economic downturns – but the current trend seems to be big spending straight through the cycle, through booms, busts, and everything in-between. Running the US economy “hot” in this manner would tend to raise the level of R*.

However, while crucial, in my view, these are longer-term concerns for the stock and bond markets.

The more immediate risk is that investors are now dramatically underestimating the potential for a recession.

Contrary to popular belief these days, the stock market typically performs best when the Fed is hiking interest rates, not when it’s cutting. It’s usually not higher rates or Fed policy that cause the most extreme phase of a bear market, but a collapse in economic growth and corporate earnings amid recession.

What really has me worried right now is sentiment on the US economy and stock market appears to be turning more bullish just as the outlook begins to deteriorate:

Are the Bulls Back?

In the monthly Global Fund Manager’s Survey put out by the research team at Bank of America earlier this month, a whopping 65% of fund managers surveyed believe the US economy will enjoy a soft landing with inflation coming down without sparking recession.

An additional 9% believe there will be “no landing,” essentially the idea that US economic growth will not slow meaningfully despite one of the most aggressive Fed rate hike campaigns in decades.

Of course, the debate over R*, and the soft and no landing narratives, are closely related because you can only really assess the neutral rate of interest by looking at the current level of rates and the health of the economy. Simply put, if your view is that the US economy remains strong then, apparently, the Fed’s rate hike campaign over the past year isn’t as aggressive as it might appear.

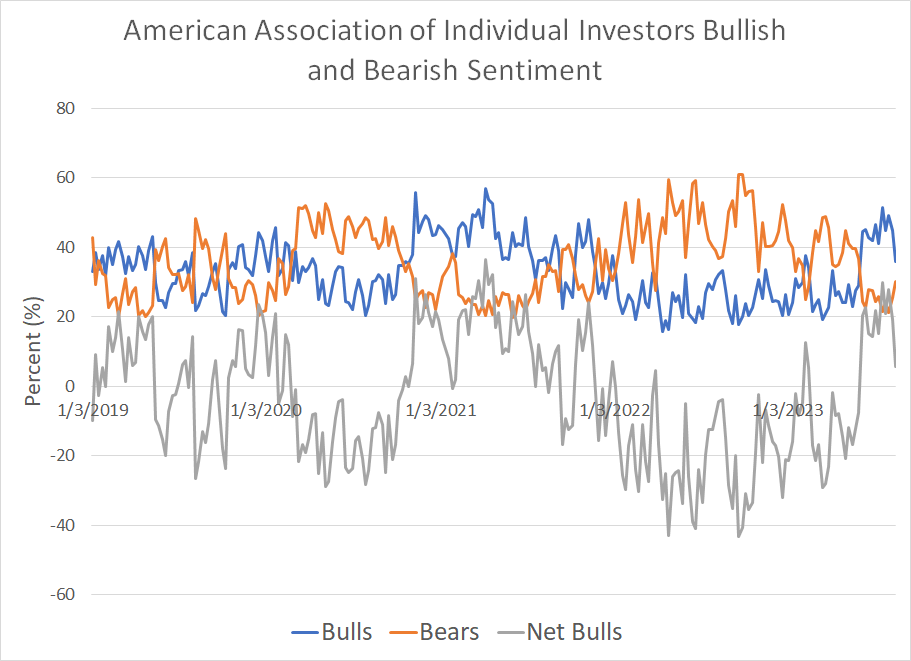

And while last week’s American Association of Individual Investors (AAII) release does show a weakening in bullish sentiment, as of the end of July, sentiment was the most bullish since late 2021, just before the major market peak:

Source: AAII, Bloomberg

Sentiment is an imperfect timing tool. However, I do believe it’s notable that following a long period of bearish sentiment through much of last year and early 2023, investors turned bullish this summer. Indeed, in the July 20th survey, just before the S&P 500’s July 31st closing peak, bulls outnumbered bears in the AAII survey to the tune of 29.9 percentage points.

That AAII July 20th net bullish reading is the highest since April 2021. To be fair, extreme bullish readings in the spring of 2021 did not mark an immediate market top; however, it did signal the final run of the 2020-2022 bull market. And, when sentiment flipped bearish in late 2021, the bull run was running on fumes with some sectors, notably tech, showing a marked deterioration in relative strength.

At a minimum, if the equity bull market through the first 7 months of 2023 was climbing the proverbial “wall of worry,” then the underinvested bears appear to have finally capitulated on the market and put some of their excess cash to work over the past month.

That leaves little wall of worry left to climb.

As the consensus adopts the soft landing narrative, 10-Year Treasury yields soar to the highest levels since 2007, and erstwhile bears flip to bulls on stocks there remains a significant risk of recession. One reason is this:

Excess Savings Have Been Depleted

Last spring in “Are We There Yet?,” I wrote about an interesting concept covered in a research paper published at the San Francisco Federal Reserve.

Simply put, the idea is that the government’s response to the COVID outbreak in 2020 was unprecedented, including direct stimulus payments to many consumers. This excess savings from stimulus payments has supported consumer spending ever since. So, the Fed paper published back in May attempted to quantify these “excess savings” and chart their progress over time.

The methodology was straightforward. The authors look at the trend in US personal savings over the 4 years up until the start of the 2020 recession and economic lockdowns (through February 2020). They then project that trend in savings through the most recent month and look at actual cumulative consumer savings over the same time.

Any cumulative savings above the trend rate are considered excess savings – essentially this is a measure of how much money government stimulus added to US consumer savings in aggregate over the past 3 years compared to a trend rate of savings growth.

Well, just last week, the same researchers at the San Francisco Fed issued an update to that research report titled: “Excess No More? Dwindling Pandemic Savings.”

Take a look:

Source: My Calculations Using Methodology in “The Rise and Fall of Pandemic Excess Savings” By Hamza Abdelrahman and Luiz E. Oliveira

As you can see, US consumers had accumulated as much as $2.1 trillion in excess savings by the middle of 2021 after multiple rounds of stimulus and a quick recovery in the US labor market from 2020 lockdowns. Starting last year, consumers began drawing down their excess savings in earnest, to about $750 billion as of the end of 2022 and just $190 billion or so as of the end of June, the last month for which we have data.

So, given that consumers spent around $280 billion in excess savings in Q1 2023 and another $280 billion or so in Q2, it’s likely these excess savings built up from COVID stimulus payments will be fully exhausted in the current quarter (Q3 2023).

Granted, estimating excess savings is not an exact science, nor can we predict with any degree of certainty what the impact of savings exhaustion might be this quarter. However, it strikes me as logical that consumers’ significant cushion of savings likely helped support spending even as the economy has slowed, and credit tightened, since last summer. In effect, excess savings could logically be expected to increase the “lags” in the cycle that I outlined in a post last Thursday “Lags, Sentiment and Market Tops.”

As savings are extinguished that also raises the risk the consumer could become more of a drag on economic growth in coming months.

With the crowd increasingly convinced the US will avoid recession and the Fed will need to keep rates above 5% for a prolonged period, I can’t help but wonder if the biggest surprise in coming months might be increased evidence the economy is slowing sharply, rising concern regarding a hard landing and a rally in bonds as a haven from equity market storms.

DISCLAIMER: This article is not investment advice and represents the opinions of its author, Elliott Gue. The Free Market Speculator is NOT a securities broker/dealer or an investment advisor. You are responsible for your own investment decisions. All information contained in our newsletters and posts should be independently verified with the companies mentioned, and readers should always conduct their own research and due diligence and consider obtaining professional advice before making any investment decision.