The Growth Premium

The Growth Premium

The market's most vulnerable groups...

Editor’s Note: I’ll be speaking at the Orlando Money Show at the Omni Orlando Resort at ChampionsGate on October 31, 2022 along with my friend and Capitalist Times co-founder Roger Conrad. If you’d like to join me at the show, you can register to attend by tapping here.

Alternatively, you can register by phone through Money Show on 1-800-970-4355, be sure to use my name when you register. It’s free to attend the conference as my guest but, if history is any guide, you may want to book your hotel room soon to get the special Money Show hotel rate.

Despite a deteriorating economic backdrop and the big sell-off in stocks year-to-date (the S&P 500 is still down 17%+), the market is still extraordinarily expensive right now:

Source: Bloomberg

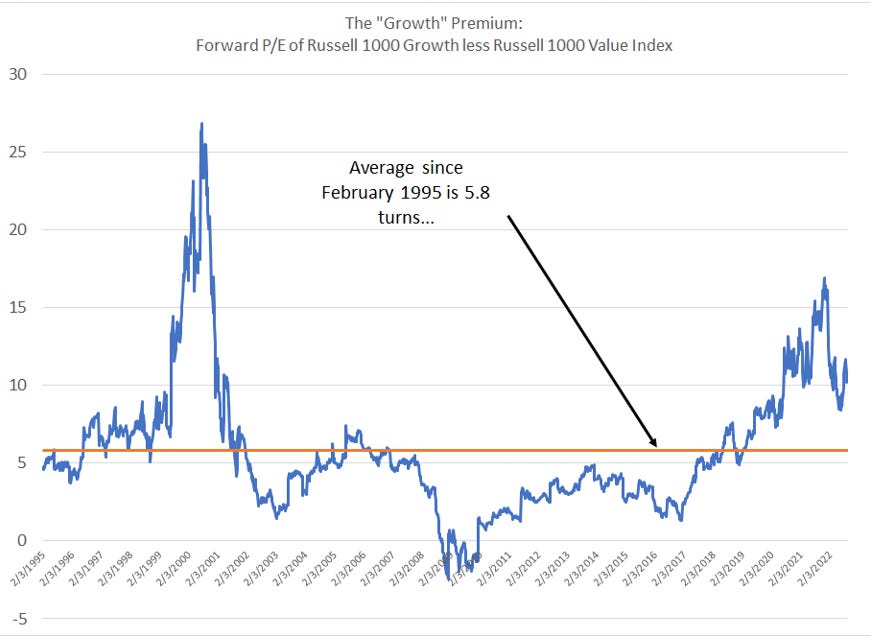

I’ve highlighted multiple measures of market valuations in recent months, so here’s one inter-market relationship I haven’t covered in some time now.

This chart shows what we like to call the “Growth Premium,” which represents the forward price-to-earnings ratio for the Russell 1000 Growth Index less than of the Russell 1000 Value Index. So, for example, the Russell 1000 Growth Index trades at almost 25 times forward earnings estimates right now compared to 14.3 times for the Value Index so the growth premium is about 10.7 turns (25 minus 14.3).

The higher this premium, the more expensive growth stocks – large cap stocks with rapid earnings growth -- are relative to their more cyclical value counterparts.

So, as you can see, while this growth premium is down from over 16 turns at the highs last year, it’s still almost double the long-term average of 5.8 turns. And, in the last big growth cycle back in 2000-02, this premium didn’t bottom until growth stocks traded at a discount (negative premium) to their value counterparts.

Given the hefty market weight for growth sectors like technology and stocks like Amazon.com (NSDQ: AMZN) in the S&P 500, it’s going to be very difficult for the stock market to see a durable rally without a major rally in badly battered growth stocks into early 2023 and a new expansion in the growth premium. And for growth valuations to expand as they did in 2020-21, you’d likely need to see two criteria – improved US economic growth and falling interest rates.

Again, with the Fed still clearly prioritizing fighting inflation right now, that strikes me as an unlikely scenario. Indeed, a sudden surge in valuations for speculative growth stocks is likely exactly the opposite of what the Fed would like to see over the next few months.

DISCLAIMER: This article is not investment advice and represents the opinions of its author, Elliott Gue. The Free Market Speculator is NOT a securities broker/dealer or an investment advisor. You are responsible for your own investment decisions. All information contained in our newsletters and posts should be independently verified with the companies mentioned, and readers should always conduct their own research and due diligence and consider obtaining professional advice before making any investment decision.