The Long Slide

The Long Slide

The slowest market cycle of the postwar era...

Financial markets are all about cycles.

That’s true whether you’re talking about bonds, stocks, or commodities like oil, natural gas and gold.

If you can answer one simple question – Where are we in the market and economic cycle? – you have a roadmap to profit from any imaginable market environment.

Of course, while that question may be simple that doesn’t mean it’s easy to answer – measuring and timing the cycle isn’t exact science, and every cycle is unique though they share certain defining characteristics, signposts and similarities.

And while some claim financial markets move faster these days than ever before, I’d argue the current cycle is the slowest of the postwar era.

After all, the S&P 500 peaked in early January 2022 while the Nasdaq 100 peaked in mid-November 2021; yet, the US economy clearly isn’t in recession right now, and declines in the broader indices from their cycle peaks remain modest.

And that brings me to this:

The Longest Bear Market

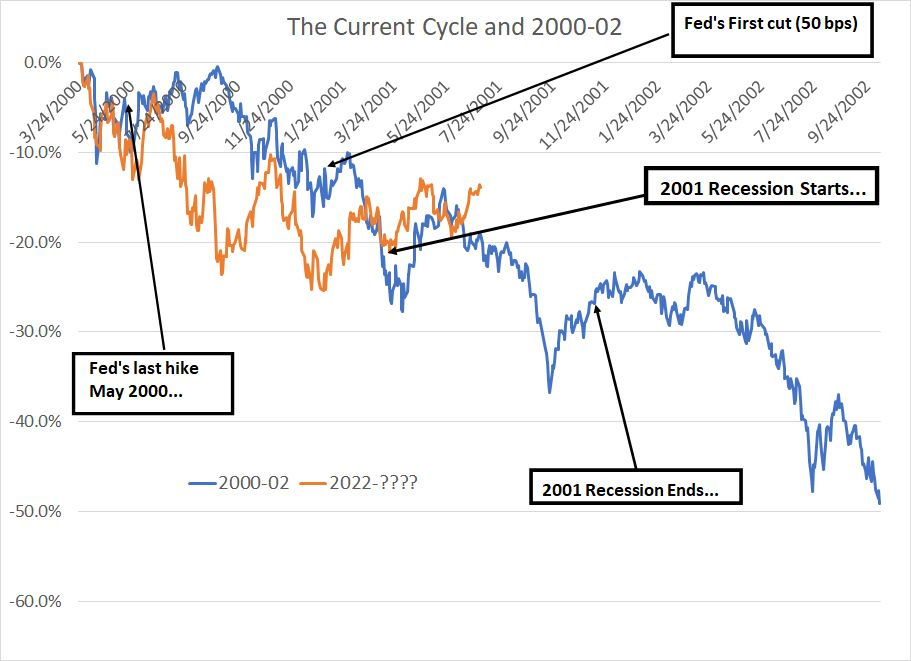

The S&P’s bear market from late March 2000 until early October 2002 was the longest since at least the 1930s, lasting for a total of 638 trading days; the maximum closing decline from peak to trough was 49.15%.

Source: Bloomberg

The blue line on this chart shows the evolution of the 2000-02 bear market in terms of cumulative decline from the market peak. I’ve also included labels to show key fundamental and economic events through that cycle.

The orange line represents the cumulative decline in the S&P 500 from the peak in January 2022 to date for comparison purposes.

I experienced firsthand the 2000-02 bear market, and the 2001 recession, albeit early in my career. And, I must confess, when I assembled the data to create this chart I expected the current cumulative market decline to be far less severe than at a similar stage of the 2000-02 bear market.

Chalk it up to the way memories change over time, but I was dead wrong about that.

After the first 322 trading days of the S&P 500’s 2000-02 bear market, the index was down 19.2% compared to 14.0% the same 322 trading days into the current cycle. That’s not far off the experience 20+ years ago and, over the past two weeks, the two bears have traded downside leadership.

Of course, naïve chart overlays are one thing, but there’s more to this comparison that just a few squiggly lines.

Let’s consider some key fundamental developments through the 2000-02 cycle, starting with this:

Fed Pivots and Bear Markets

The market peaked in March 2000, but the economy was still on solid footing at that time and the Federal Reserve maintained a tightening bias, hiking rates 50 basis points one final time in May 2000.

The Fed then “paused” with rates at 6.5% until January 2001 when, in a surprise inter-meeting move, then-Chairman Greenspan cut by 50 basis points to 6%.

In total the Fed cut rates by 300 basis points to 3.5% by August 2001; following the September 11, 2001 terrorist attacks, the pace of cuts accelerated, and interest rates were at 1.75% by December of that year, a level considered extraordinarily accommodative at that time.

It’s also important to reiterate the economy was red-hot at the end of 1999 – the Manufacturing Purchasing Manager’s Index stood at 58.1 in November 1999 and the Conference Board’s US Leading Economic Index (LEI) grew at +5.2% year-over-year in January 2000.

The ISM PMI finally dropped below 50 in August 2000 and hit a recessionary level below 45 in December of that year. Meanwhile, the year-over-year change in LEI – historically a good harbinger of recession ahead – turned negative in November 2000.

As I mentioned earlier, the National Bureau of Economic Research (NBER) dates the recession to March 2001; it was one of the shortest and mildest in history, lasting only until November of the same year. Yet, the market fell for nearly a year after the recession ended; indeed, the most intense declines of the entire cycle started in the summer and autumn of 2002.

So, let’s compare those developments to the current cycle.

The Fed Funds futures market is pricing in 83.6% probability the Fed hikes 25 basis points at its next meeting on May 3, 2023, taking the target rate to 5.25%. Futures have been all over the place in terms of expectations for the back half of 2023 and early 2024; however, as it stands right now, the market is pricing in about 75 to 100 basis points of cuts by early next year.

Of course, based on the summary of economic projections released at last month’s meeting, the consensus on the FOMC favors holding rates at 5.25% though year end, then cutting rates by roughly 100 basis points by the end of next year.

It seems the definition of what constitutes a Fed “pivot” depends on whom you ask – if a pivot means the final cut in a hiking cycle, that’s likely to be next month. And if a “pivot” is the first cut of the loosening cycle, then I suspect that’s likely by this autumn or early 2024.

However, before you conclude this “pivot” is an all-clear to buy stocks with both hands, take a second look at the 2000-02 cycle.

The Fed’s final cut of that cycle was May 2000, less than 2 months after the peak of the bull market in late March. And the Fed’s first cut was January 2001, just as the bear market was accelerating to the downside and 2 months before the start of the recession in March 2001.

Indeed, Greenspan only implemented that surprise 50 basis point cut in early January 2001 after clear signs the US economy was in danger of tipping into recession.

In other words, regardless of your definition of “pivot,” it wasn’t bullish for stocks and other risk assets in 2001 nor do I expect it to be this time around.

Momentum Delays Recession

And while it was 23 years ago, I do vividly recall some of the conversations underway back in the spring and summer of 2000.

Then, as now, the economy looked to be slowing, but it wasn’t at all clear that recession was imminent. Indeed, market participants were still fretting over the potential for additional tightening from the Fed:

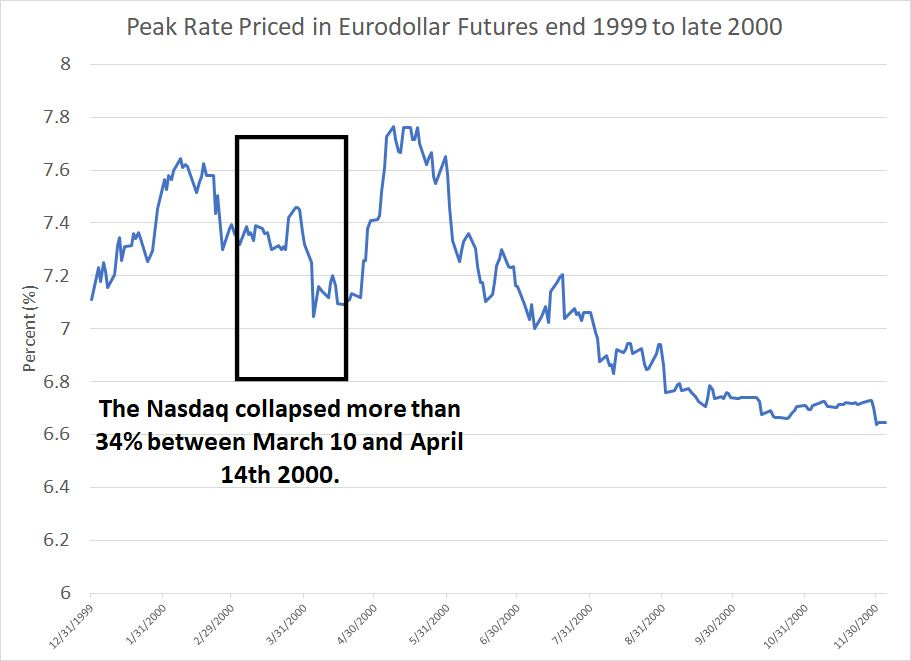

Source: Bloomberg

This chart uses the Eurodollar futures market to determine market expectations for peak expected short-term interest rates over the ensuing two years from the end of 1999 through to December 2000.

The Nasdaq Composite was up 13.4% in the first two months of 2000 in what turned out to be the final spectacular melt-up of the long tech bull market of the late 1990s. With tech stocks soaring and the economy still on solid footing, market expectations for further interest rate hikes ramped in early 2000.

Then, there was an accident.

The Nasdaq, the leader of the late 90’s bull market, collapsed more than 34% between March 10 and April 14th 2000. We began to hear talk the Fed had “broken something” after hiking rates from 4.75% to 6% between June 1999 and March 2000; some began to speculate the central bank was “done” for the current cycle and, as you can see, peak rate expectations backed off by around 50 basis points as the market crashed.

Finally, the stock market recovered in May – August with the S&P 500 climbing more than 12% from its April low to its late August high and the Nasdaq Composite up a whopping 35.1% from May 24th through mid-July 2000.

That, coupled with the Fed’s hike in May 2000 convinced investors more hikes might be in store that year – expectations for peak rates actually reached fresh cycle highs by the summer of 2000.

In short, from this standpoint, the current situation appears analogous to the summer or early fall of 2000 for a few reasons:

The economy is slowing, but still on decent footing and a recession is not yet underway.

The Fed still holds a tightening bias though they’re likely reaching the end of that tightening cycle and markets continue to wrestle with the timing of a potential pause or pivot.

There have been some warning shots of stress in markets – the tech wreck in April 2000 and the regional banking crisis last month – however, one could still make the argument these crisis events are isolated and don’t present a serious threat to the broader economy and financial markets.

Now, back in 2000 the bear market seemed fairly mild for the S&P 500 through the summer; in fact, as late as September 2001, the S&P 500 was within 2% of its all-time highs set almost 6 months earlier.

However, trends turned more sinister in the autumn of 2000 and into early 2001 with the S&P 500 declining more than 20% from its all time peak by March 2001.

The precipitating event for the downside acceleration was not additional rate hikes, rather, it was clear signals the economy was tipping into recession by the autumn of 2000. Those signs were visible both in the economic data as well as in corporate earnings when leaders of the erstwhile rally began to disappoint and experience sizable declines on the news.

Talk of perennial growth for tech stocks due to the rapid growth in use of the Internet faded into talk of excess tech-related spending in the late 90’s and a hangover in 2000-01.

Of course, as I said, no two cycles are exactly alike. However, in 2000-01 it was the rapid deterioration in economic conditions and a worsening corporate profits outlook that prompted a rapid sell-off in the broader market, NOT changes in Fed rate hike expectations.

Moreover, warning signs of economic weakness remained elusive for almost 9 months after the market peaked in early 2000.

One should be careful about comparing two market environments as it’s all-too-easy to make sweeping and erroneous conclusions by overlaying the chart of the S&P 500 today over the same chart from 23 years ago.

However, in my view these cycles share one key similarity that make the analog relevant:

Source: Bloomberg

The US economy is much like a giant oil tanker – it has momentum and can’t change course or turn around quickly. In both 2000-02 and the current bear market cycle, the economy started from a position of strength and considerable growth momentum.

This chart shows the month-over-month change in the Conference Board US Leading Economic Index (LEI) from February 1999 through December 2001 (the blue bars) and from August 2020 to the present (orange bars).

In both cycles the economy was growing at a solid clip in the 12 to 18 months prior to the stock market peak, featuring a series of sequential LEI gains of 0.5% to 1.0%. Similarly, the US unemployment rate fell from 4.6% in September 1998 to a multi-decade low of 3.8% in April 2000 much as it recently touched 60-year lows of 3.5%.

I’d posit the economy was even stronger in 2020-21 because the sheer scale of the fiscal and monetary accommodation applied following the COVID lockdown recession dwarfs the relatively modest stimulus efforts from the Federal Reserve in 1998 following the Russian debt default and the collapse of the LTCM hedge fund.

(The level of coordinated stimulus in 2020-21 is unprecedented in peacetime; the subsequent growth jolt to the US economy, and the dangerous generational surge in inflation, are predictable consequences).

However the key point is that in both 2000 and 2022 the economy entered the year with significant growth momentum that took time to fade. Indeed, in both cases, it wasn’t imminent recession that prompted the initial selling pressure, but concerns about bubbles in financial markets (ironically, tech/growth stocks in both cases).

Eventually, there was spillover from the bubbles in financial markets to the real economy and from the real economy to broader corporate earnings. This negative feedback loop is what prolonged the 2000-02 bear market despite the fact the 2001 recession was among the mildest of the prior 50 years.

So, that brings me back to the question I posed at the beginning of this update:

Where are we in the market and economic cycle?

Given the glacial speed of the current cycle, I suspect the answer is we’re in a position similar to the summer or fall of 2000. The slide from white-hot economic growth to recession is taking longer than usual this cycle, but a recession is coming and with it stocks are likely to probe new cycle lows.

DISCLAIMER: This article is not investment advice and represents the opinions of its author, Elliott Gue. The Free Market Speculator is NOT a securities broker/dealer or an investment advisor. You are responsible for your own investment decisions. All information contained in our newsletters and posts should be independently verified with the companies mentioned, and readers should always conduct their own research and due diligence and consider obtaining professional advice before making any investment decision.