This Time Really Isn’t Different

This Time Really Isn’t Different

In a speech before the UK House of Commons in 1948 Sir Winston Churchill said:

“Those who fail to learn from history are condemned to repeat it.”

(While this phrase is often attributed to Churchill, it’s a slightly altered quote from Spanish-American philosopher George Santayana.)

Regardless, the sentiment rings true – the current perilous situation for the US and global economies looks increasingly like the early 1970s due, in part, to repeating many of the policy mistakes of the 1960s.

I must confess, when I studied economics in the 1990s at the University of London, our look at economic history in the US and UK through the period from 1960 to the early 1980s didn’t seem particularly relevant. I once assumed policymakers had learned from the “wage-price” spirals of the 70s and would be loath to allow loose monetary policy to feed into long-term inflation expectations ever again.

However, the experience of the past 15 years has proved that assumption incorrect. Following the global financial crisis of 2007-09 and, to an even greater extent following the global coronavirus lockdowns of the 2020-22 era, the Fed and other central banks have committed a policy blunder that’s arguably even bigger than those of the early 1970s.

Easy money and ultra-low interest rates for much of the past 15 years led first to a bubble in financial assets including stocks and, particularly, growth stocks.

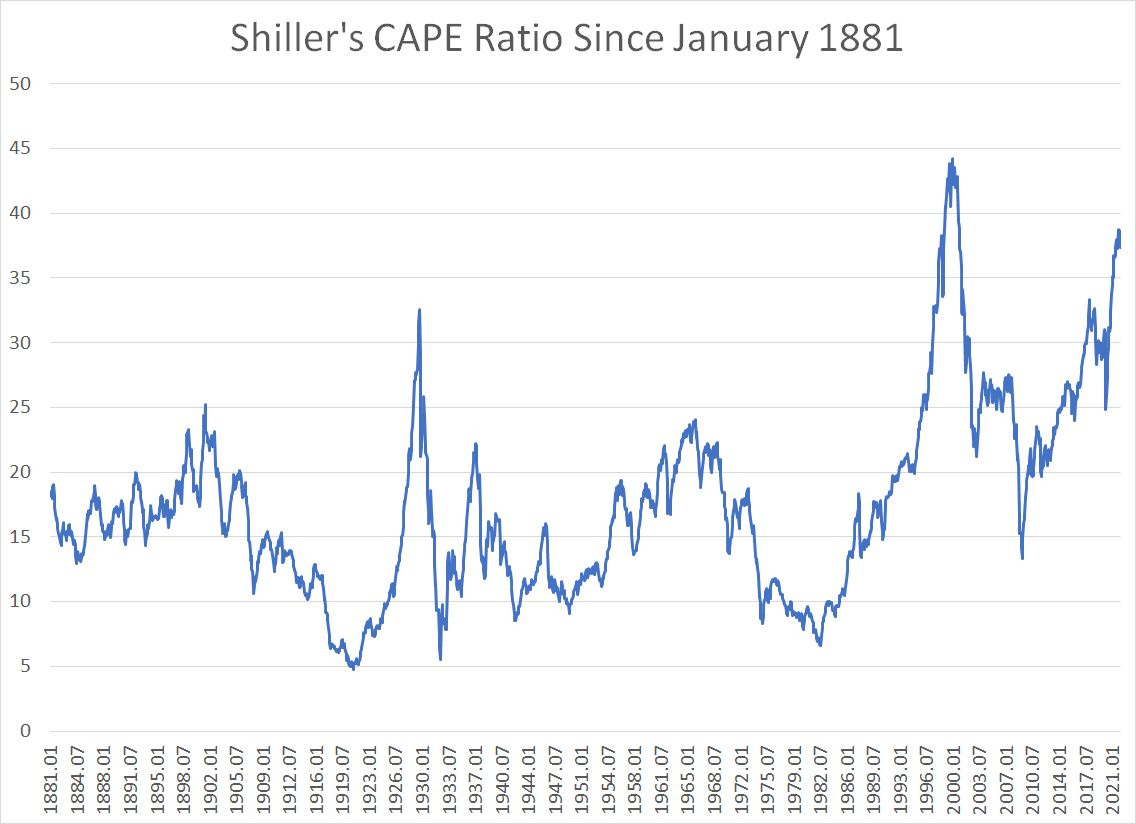

That’s driven stock market valuations to incredible heights in recent years:

Source: Professor Robert Shiller, Yale University

This chart shows Robert Shiller’s Cyclically Adjusted Price to Earnings (CAPE) ratio for the S&P 500 since January 1881. As you can see, the current reading is 37.4 times, the highest in more than 141 years of US financial history save a brief period from late 1998 to early 2000.

Also note the previous spikes in this index of market valuations – the peaks in April 1901, August 1929, February 1966, and January 2000.

Let me give you a bit of financial history in a nutshell: None of these four historic spikes in CAPE ended well for those broadly invested in US stocks.

More specifically, you’re probably familiar with historic market performance following the 1929 peak (The Great Crash and Depression), the 1966 peak (the Great Inflation) and the 2000 peak (the Y2k Tech Wreck).

However, in case you’re wondering about April 1901, Shiller’s approximation for the S&P 500 closed at almost the same level in April 1901 as it did in September 1923, more than 22 years later. Unfortunately for anyone who bought and held stocks over this period, the purchasing power of $1.00 in 1923 was the same as just 43 cents in 1901.

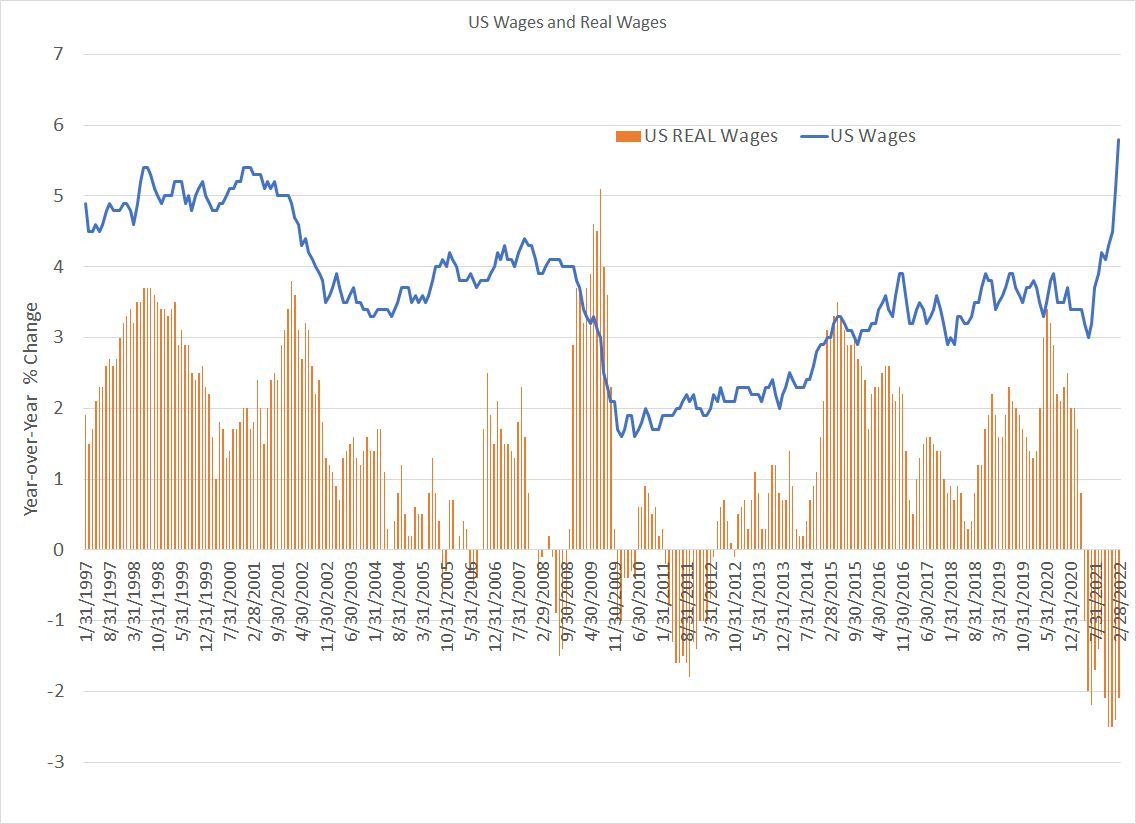

And, more recently, the coordinated easy money and fiscal stimulus from the Fed and US government since 2020 have had much the same effect as the coordinated stimulus campaigns of the late 1960s and early 70s:

Source: Bloomberg

This chart shows the Atlanta Fed’s Wage Tracker Index as a blue line, which shows overall annualized growth in US wages. To create the orange bars of real wage growth, I simply adjusted annual growth in US wages by inflation (CPI).

As you can see, US wage growth is BOTH the strongest it’s been in 25 years AND the weakest.

On a nominal basis, US wages are up 5.8% year-over-year, even higher than the boom years of the late 1990s. Yet, sky-high inflation means the purchasing power of those rising wages is falling by more than 2% annualized, an even bigger drop than coming out of the vicious 2007-09 recession.

Will Americans sit by and watch the purchasing power of their wages fall?

Well, the experience of the 1970s suggests they will not – rising inflation expectations ultimately lead to faster wage growth, which ultimately feeds even more aggressive wage demands.

Indeed, that’s already reflected in current economic data as well – the latest JOLTS data from the Bureau of Labor Statistics shows a near-record total of more than 11.26 million unfilled jobs in the US, which compares to only about 6.3 million unemployed.

They say the most expensive words in the financial markets are “This time it’s different.”

Well, I owe yet another debt of gratitude to my economics professor and dissertation advisor at the University of London almost 30 years ago – that study of the 1970s experience is priceless.

My bet is this time is NOT different – not for the economy, not for stocks, not for inflation and not for commodities.

There is one piece of (very) good news for those of us trying to generate real wealth through trading and investing in financial markets.

You see, investors who simply bought the index or invested in a diversified mix of US stocks in the late 1960s lost money in real terms throughout the 1970s and into the early 1980s as their meagre nominal gains were more than fully offset by the ravages of inflation.

History suggests those who invest in index funds or ETFs can expect a similar experience over the next 5 to 10 years, while those invested in growth funds are likely to see even bigger losses. Indeed, the most famous growth fund of the 1960s – run by Gerald Tsai, celebrity manager of his day – ultimately lost more than 90% of its value in the ensuing bear market.

However, investors willing to “trade” the cycles of that era – the multi-year bull and bear cycles from the late 1960s until the 1982 low – stood to generate tremendous gains.

Similarly, the 70’s was a golden age for commodities and a great time to be invested in smaller US stocks.

In short, there were plenty of bull markets (and bear markets) in the 1970s even though the long-term, buy-and-hold investor got crushed to the point that then-influential BusinessWeek magazine ran a cover story in its August 13, 1979 issue titled “The Death of Equities.”

DISCLAIMER: This article is not investment advice and represents the opinions of its author, Elliott Gue. The Free Market Speculator is NOT a securities broker/dealer or an investment advisor. You are responsible for your own investment decisions. All information contained in our newsletters and posts should be independently verified with the companies mentioned, and readers should always conduct their own research and due diligence and consider obtaining professional advice before making any investment decision.