Two Ways High Yield Bonds Suffer

Two Ways High Yield Bonds Suffer

And one way to profit...

Investors will need to make up their minds ahead of the next Fed meeting scheduled for March 22, 2023.

Either one of two things – but not both – can be true.

Soft Landing or No Landing

The first option is that the US economy is strong and we’re headed for a soft landing or even a “no landing” scenario.

If that’s the case then inflation isn’t likely to come down even close to the Fed’s 2% target without tighter monetary policy and, just as important, a higher-for-longer Fed funds rate.

Indeed, the market appears to be in the early stages of pricing in that outcome:

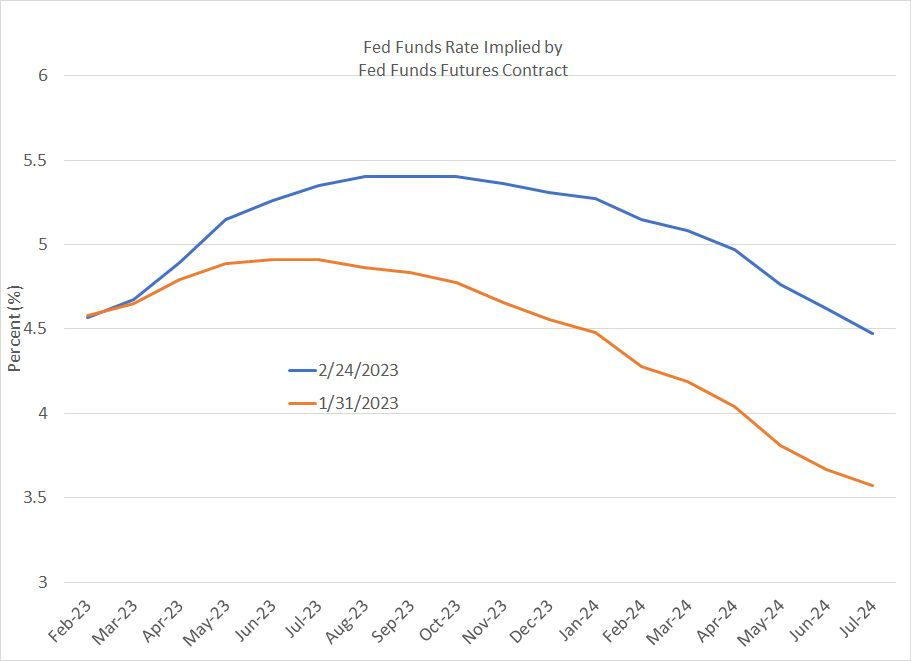

Source: Bloomberg

This chart shows the Fed Funds rate priced into Fed Funds Futures on two different dates, January 31st and February 24th. As you can see, market participants were looking for peak Fed Funds rate of approximately 4.9% as of the end of January and were expecting the Fed to start cutting rates by the end of 2023.

By late February, the market was pricing in a peak Fed Funds rate a full 50 basis points higher at 5.4% with the subsequent Fed cutting cycle to start later, perhaps not until the spring of 2024.

And while rate expectations are rising, so too are expected breakeven inflation rates:

Source: Bloomberg

The 5-Year Breakeven Inflation Rate – a market-derived measure of inflation expectations over the next 5 years –tested 2.6% late last month. While that’s well off last year’s peak at 3.7% or so, it’s also up sharply from the mid-January lows near 2.14%. Just as important, we’re now seeing market inflation expectations back at October-November 2022 levels despite the recent bump higher in Fed rate hike expectations.

This higher-for-longer rate scenario likely means higher bond yields across-the-board with yields on high-yield junk bonds rising alongside yields on government and corporate bonds of all stripes.

Rising yields would drive down the value of iShares iBoxx High Yield Corporate (NYSE: HYG), an ETF that tracks high yield bond prices.

Recession is Coming

The second option – the one I favor – is that there will be a recession this year, it’s just been delayed to the second half of 2023.

Every economic and market cycle is a bit different though they all share certain common elements. In a normal cycle, the stock market peaks and then, within a year, the US economy enters recession. As the economy slumps, so do corporate earnings, and the rapid decline in profit expectations is what normally results in the most intense phase of the bear market.

In this cycle, the S&P 500 peaked in January 2022, but we’re not in recession yet.

In my view, there are two main reasons for this unusually large lag time between market peak and recession:

1. Most of the selling pressure in markets to date has been a function of concerns about rising interest rates and the most aggressive Fed hiking cycle since the 1980s. That’s why interest rate sensitive technology stocks peaked long before the broader market and it’s also why, as I pointed out in last week’s issue of FMS, “What Bear Market,” some stocks, sectors, and foreign market indexes remain within a whisker of all-time highs.

2. The US economy was growing at a rapid pace at the end of 2021 and consumers’ balance sheets were healthy due to COVID-era stimulus spending and a still-strong jobs market. Indeed, while some will undoubtedly argue with me, I believe it was excess government stimulus that led to the inflation problem we’re currently experiencing coupled with years of underinvestment in the real “old” economy (energy production, for example). This strong momentum heading into 2022 means that it’s taking longer than normal for the economy to slow and for rate hikes to “bite.”

Regardless, the strong economic data the market has focused on of late – like the monthly payrolls and retail sales numbers – generally represents either lagging economic data and/or series that are heavily influenced by seasonal adjustments and revisions.

Key leading indicators, such as the yield curve, the Conference Board’s US Leading Economic Index continue to point to economic weakness by the second half of this year.

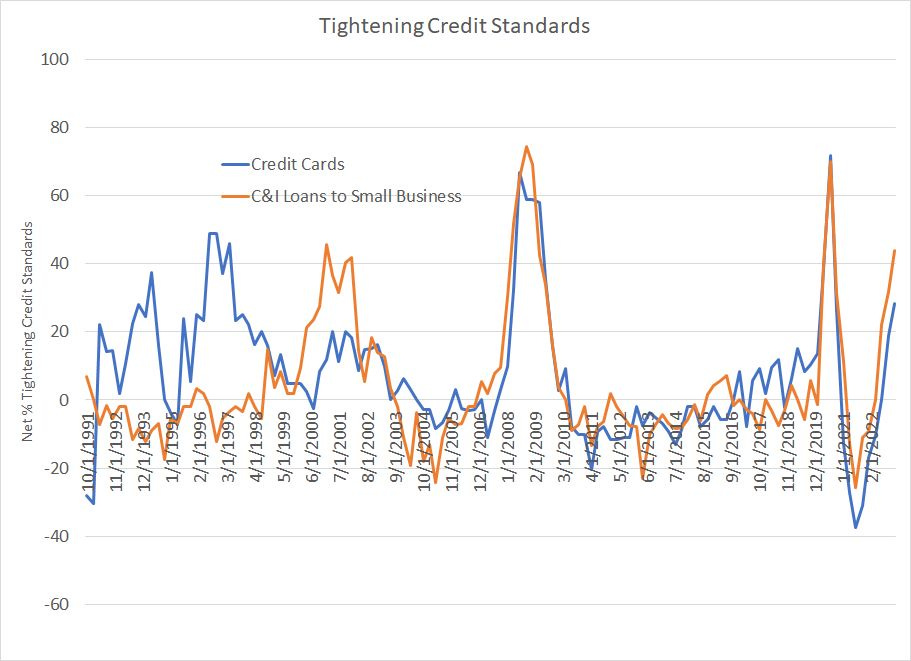

So too the Fed’s Senior Loan Officer Survey:

Source: Bloomberg

This chart shows data from the Fed’s quarterly Senior Loan Officer Opinion Survey. A rising line indicates that banks are tightening lending standards, making it more difficult to obtain credit.

The Fed survey breaks down lending standards for multiple categories of loans – I’m highlighting just two on this chart, lending standards for small business Commercial and Industrial (C&I) loans and lending standards for consumer credit cards.

As you can see, lending standards tend to spike ahead of US recessions such as back in 2000, in 2007-08 and again in 2019-20. Once again, lending standards are spiking, which suggests that later this year the main engine of the US expansion right now – consumer spending – will be sputtering.

Of course, recessions are bad news for high-yield bonds even when they lead to a Fed pivot on rates:

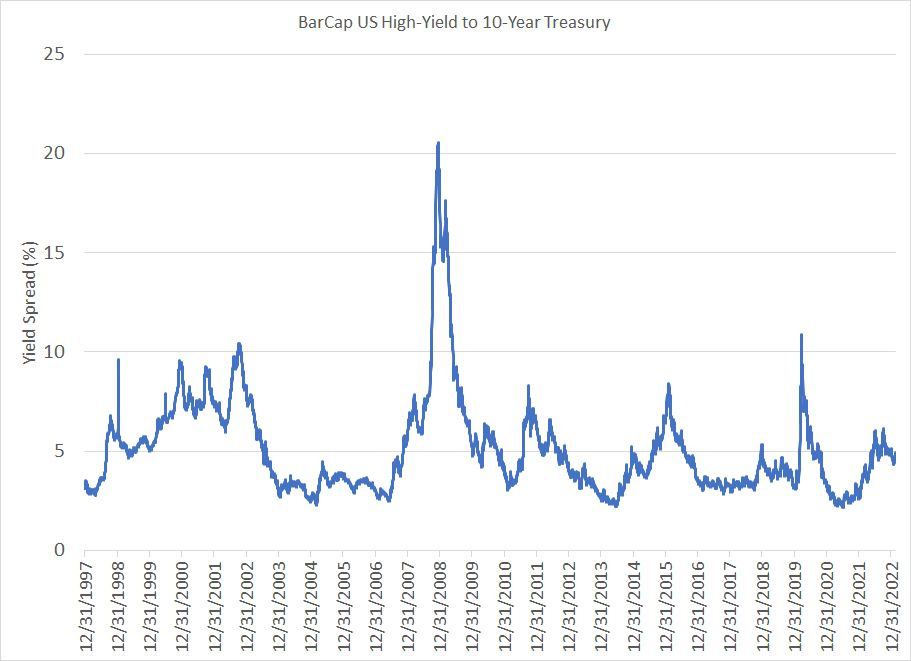

Source: Bloomberg

This chart shows the yield spread between the BarCap US High Yield Corporate Index and the 10-year US Treasury bond since the late 1990s.

As you can see, yields on high-yield “junk” bonds historically spike during US economic downturns as recessions cause a deterioration in corporate credit quality, particularly for companies with shakier credit profiles.

Last year, this spread spiked to a peak just over 6% in early October, but has since receded to under 4.5%. At 6% the spike in high-yield bond yields was minor compared to economic “soft patches” like 2010-11 and 2015-16, let alone recessions like 2001, 2007-09 and 2020.

Simply put, if there is a heard landing as I expect, look for some sort of high-yield corporate credit event this year when yields spike sharply relative to the 10-Year Treasury.

The only scenario that would be bullish for high yield bonds would be what some are calling the “immaculate disinflation” scenario. In this scenario, inflation trends down to the Fed’s target without significant additional upside to rates; yet, somehow, the US economy avoids recession.

In that event, we’d effectively return to the low-inflation, ultra-low-rate environment that dominated from 2009 through to 2021.

However, that “have your cake and eat it too” scenario seems (by far) the least likely outcome, based more on hope and the collective fairytale that this time it’s different than economic and market realities.

How to Profit from Falling Junk Bonds

The ProShares Short High-Yield Fund (NYSE: SJB) is an ETF that’s designed to rise in value when the Markit iBoxx USD High Yield Index declines in value.

The iBoxx High Yield Index index tracks a portfolio of US dollar denominated corporate bonds with credit ratings below investment grade.

Take a look:

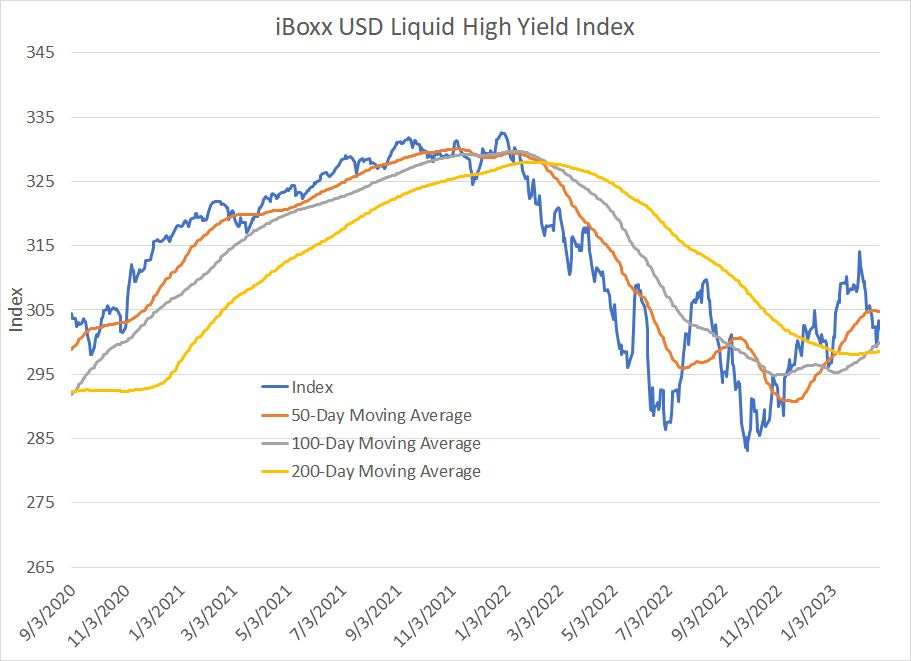

Source: Bloomberg

As you can see, high-yield bonds peaked just ahead of the stock market on December 28, 2021 and this index fell about 14.9% to a low in late September 2022.

The subsequent rally effort over technical resistance at 310 failed in early February and this index is close to taking out support at the 200-day moving average.

The March 2020 lows for the index were around 240 and in late 2018, amid a mini panic about rising rates at the time, the index reached 263 before rebounding.

If there is a US recession as I expect then this high yield bond index could easily retest those lows, down 15% to 20% from the current quote.

Like all inverse ETFs, SJB is exposed to some compounding error, a phenomenon I covered in FMS back in January 2022; however, the problem is minimized by the low volatility of the underlying index. As an example, the iBoxx High Yield Bond Index declined 11.9% from the end of 2021 through the lows in late September 2022 and the SJB ETF was up 11.24%, broadly tracking 1x the inverse of its benchmark.

DISCLAIMER: This article is not investment advice and represents the opinions of its author, Elliott Gue. The Free Market Speculator is NOT a securities broker/dealer or an investment advisor. You are responsible for your own investment decisions. All information contained in our newsletters and posts should be independently verified with the companies mentioned, and readers should always conduct their own research and due diligence and consider obtaining professional advice before making any investment decision.