Wall Street's Not-so-Free Lunch

Wall Street's Not-so-Free Lunch

America's growing, dangerous retirement pitfall

You’ve probably heard or read the old adage there’s only one free lunch on Wall Street and that’s diversification.

The idea is pretty simple:

If your portfolio consists of a single stock, your financial future is entirely dependent on the fortunes of that one company and its industry group. However if you buy a basket of say 20 stocks in different industry groups and business niches, then strong performance from some of your holdings can offset the inevitable clunkers and underperformers.

Even better, why not just buy the SPDR S&P 500 Trust (NYSE: SPY), the oldest and largest exchange traded fund (ETF), giving you a stake in the 500 stocks in the S&P 500 index with one simple transaction?

Add in investments in other assets classes — say an allocation to fixed income (bonds), foreign stocks, maybe even gold — and your risk theoretically drops even further. That’s because when the US stock market tumbles, strength in bonds or gold could help soften the blow.

The result is (theoretically) less risk and steadier, more reliable returns over the long haul.

It’s the big idea that underlies the surge in popularity of passive and index investing strategies over the past decade:

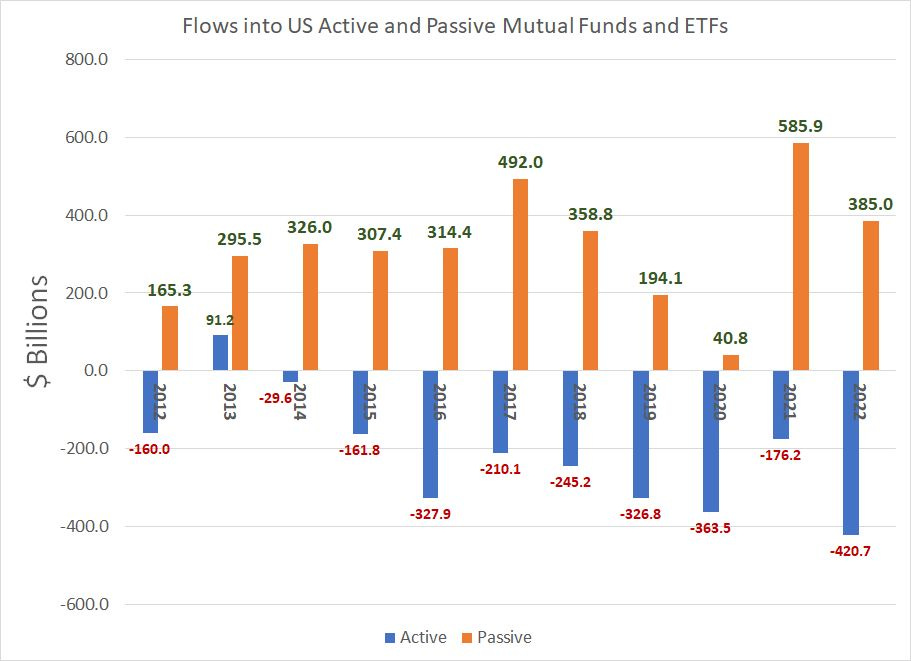

Source: Bloomberg

This chart shows annual net investment into passive and active equity (stock) mutual funds and exchange-traded funds (ETFs) by year from 2012 through 2022.

As you can see, over this 11 year period, active equity funds have only experienced a single year of inflows — $91.2 billion back in 2013 — while passive/index funds have seen inflows in every single year over this time period.

In 2012, US passive equity mutual funds and ETFs held total assets under management (AUM) of about $1.82 trillion, accounting for less than one-third of total equity AUM. Last year, total assets in passive equity funds jumped to $8.56 trillion, an increase of more than $6.7 trillion since 2012 alone.

Passive/index funds and ETFs now account for more than 55.4% of all assets under management in US equity funds.

In short, passive strategies now dominate the investment landscape.

A Moving Target

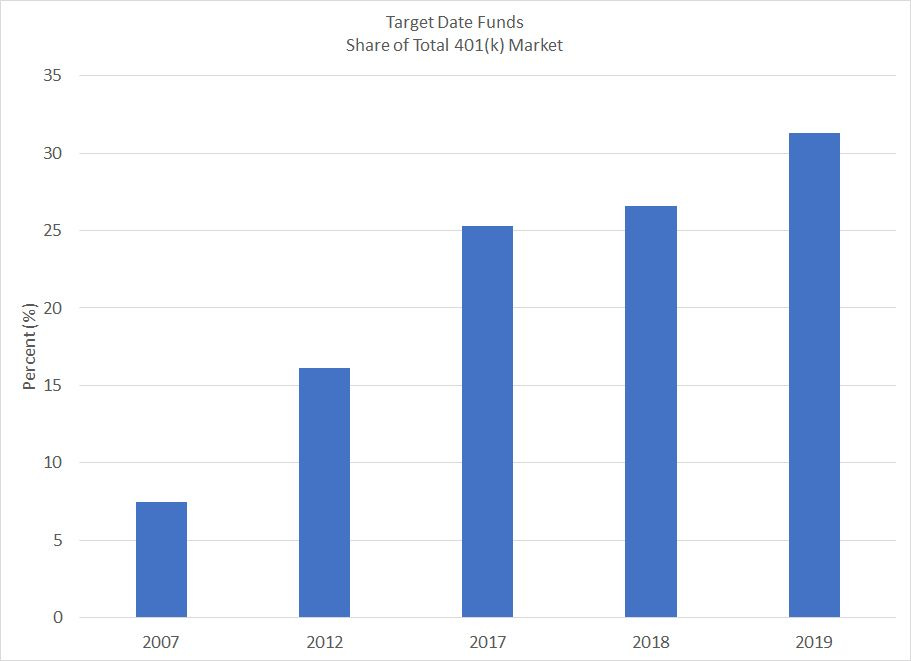

And that brings me to so-called target date retirement funds:

Source: Investment Company Institute

Target date funds attempt to offer portfolio diversification and gradual rebalancing over time.

The idea is that younger investors, still decades from retirement, can afford to place a larger share of their assets in the stock market, where long-term returns are higher at the cost of greater volatility and risk. If the stock market tumbles 30% in a bear market, it’s hardly a disaster for a 25-year-old with 40 working years before retirement; given time, stocks usually bounce back.

Thus, younger investors in target date retirement funds have most of their assets in the stock market, benchmarked to an index like the S&P 500. Over time, as the investor ages, the target fund gradually reduces exposure to stocks and boosts exposure to fixed income (bonds).

Fixed income portfolios generally offer lower return potential; however, safety and stability of principal are of paramount importance for investors approaching retirement.

Sounds logical, right?

Apparently it does to many investors: Back in 2007 only 7.5% of all assets invested in US 401(k) retirement plans was allocated to target date funds; by the end of 2019, at allocation had soared to almost one-third of total AUM.

Why Does Diversification Work?

However, let’s step back for a moment and consider why diversification works.

It’s not about the total number of stocks you own.

For example, if you buy 20 different US bank stocks you’re not really diversified because all of your holdings are in the same industry group. So, in a year like 2008, the entire financial industry got clobbered amid a global credit crisis and there were few hiding places from the carnage.

In 2008 financial stocks were highly correlated, moving in the same direction (down) at the same time.

Diversification only “works” if different stocks and industry groups are driven by different fundamentals, moving in different directions at different speeds. Diversification works when stocks in various industry groups, bonds, commodities and other asset classes are less correlated.

So, let’s start with the most common form of portfolio diversification — owning some mix of equities (stocks) and fixed income (bonds):

Source: Bloomberg

To create this chart I looked at weekly changes in the yield of the US 10-Year Treasury Bond and percentage changes in the S&P 500 since the mid-1960s. The chart depicts the 104-week (2-year) rolling correlation of bonds and stocks over this time frame.

(When the price of a bond rises, the yield falls, so I’ve inverted the scale.)

Simply put, when this correlation falls below zero (rises on my chart) that indicates the price of the 10-year Treasury Bond and the S&P 500 are positively correlated — stocks and government bonds have tended to move in the same direction over a trailing 2-year lookback window.

Look at my chart and you’ll see that stocks and bond prices were negatively correlated back in the mid-to-late 1960’s, positively correlated for much of the period from 1970 to 1997 and then negatively correlated again from the late 90’s up until very recently.

Portfolio diversification using bonds and stocks works best when these two asset classes are negatively correlated and starts to break down when the correlation flips positive.

Simply put, if you own a mix of bonds and stocks and the S&P 500 declines, you want bond prices to RISE to help offset losses in stocks.

The period from September 2007 through the end of February 2009 offers a perfect example — the S&P 500 plummeted about 50% over this period, but the iShares 7-10 Year Treasury (NYSE: IEF) and iShares 20+ Year Treasury (NYSE: TLT) ETFs jumped 18.1% and 21.8% over the same time period, softening the blow.

Traditional investment allocations like 60/40 — 60% of assets in stocks and 40% in bonds — or target date strategies such as I outlined earlier performed far, far better than the S&P 500 through the 2007-09 bear market.

However, if bonds and stocks are positively correlated this diversification benefit erodes because bond prices and stock prices rise — and fall — together.

There’s a concept in behavioral economics called the “recency bias.” This refers to a natural human tendency to place greater weight upon recent events and experience when making investment decisions.

Take a look at my chart of stock and bond correlation and you’ll see recent experience supports a negative correlation between bond and stock prices. Thus, the recency bias helps explain the growing popularity of passive stock and bond hybrid strategies such as target date funds.

However, for much of the time period covered by my chart, including the near 30-years from 1970 to the late 1990s, stocks and bonds have been positively — NOT negatively — correlated.

More specifically, in inflationary periods, bond and stock prices tend to be positively correlated.

That’s because when the inflation outlook is benign, such as its been for most of this century, the Federal Reserve can respond to market and/or economic weakness by cutting interest rates in an effort to stimulate economic activity. In 2008-09, for example, the Fed cut rates to zero and started its first round of quantitative easing to support the economy.

This drove a surge in bond prices (fall in yields) that helped support hybrid stock-bond strategies through he vicious bear market of 2007-09.

In the 1970s, however, the Fed didn’t have that luxury. As I explained in the January 24, 2023 issue of The Free Market Speculator “Yield Curves, Recessions and Bear Markets,” stubbornly elevated inflation forced the Fed to maintain tight policy despite a deepening US recession.

And, in the mid-1970s, when the Fed finally pivoted — easing policy to support growth — inflation flared anew, reaching fresh peaks in the early 1980s. The 70’s was a terrible decade for both bonds and stocks — the stock market fell about 1.5% annualized when adjusted for inflation while a diversified portfolio of bonds lost roughly 1.2% annualized from 1970-79. Stock and bond market investors didn’t even break even in real terms through the entire period from the late 1960s to the early 1980s.

The problem is the current market and economic environment looks a lot more like the 1970s than the 2000-2021 period', and the recent flip to positive stock and bond market correlation suggests markets are beginning to price in a more 70’s like trading environment.

It’s also apparent in the outlook for inflation and rates, as I explained in my February 14th issue Higher for Longer.

And passive equity funds and ETFs may not be as diversified as you might suppose:

It’s All One Trade

When you buy the S&P 500 or an ETF like the SPY are you really diversified?

Yes, you’re buying 500+ stocks across 11 different economic sectors ranging from technology to financials, consumer staples and energy.

However, because of the way the index is weighted by market capitalization, the vast majority of your assets are actually invested in just a handful of large cap stocks — the top 10 alone account for more than one-quarter of the SPY’s weight and 8 of those 10 stocks are technology stocks or names like Tesla (NSDQ: TSLA) and Amazon.com (NSDQ: AMZN)that are tech-enabled.

And, increasingly, movements in various sectors of the stock market are correlated:

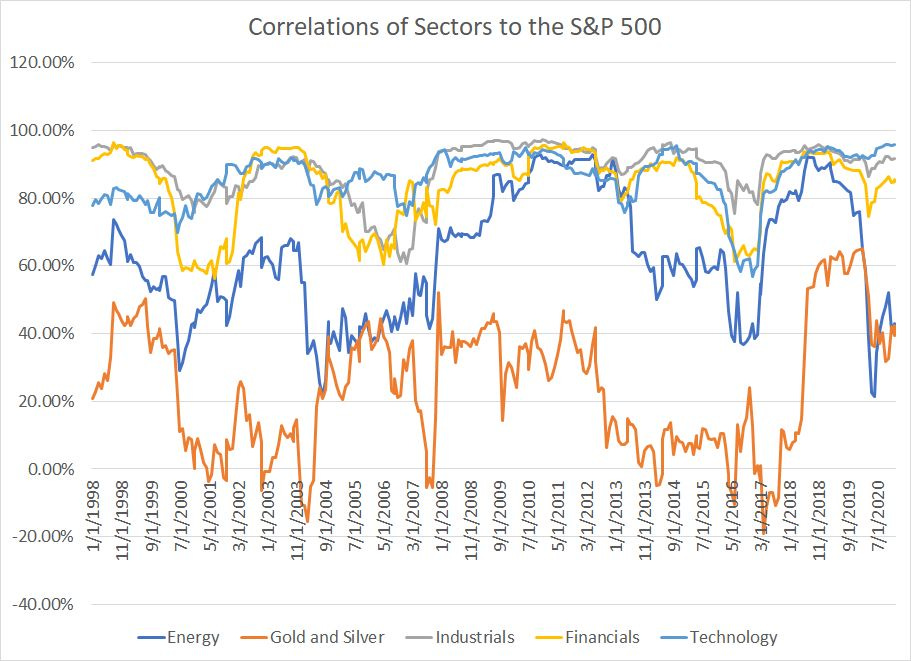

Source: Bloomberg

This chart shows rolling 24-month correlations between 5 equity market indices and the S&P 500 since 1998.

Of course, most stocks are positively correlated to the broader market to some extent; however, the lower the correlation, the more of a diversification benefit you get from holding stocks in that group.

As you can see, since 2016 or so the S&P 500 Financials , Technology and Industrials indices have generally been around 90% correlated to the S&P 500 — these stocks more or less have moved in lockstep with the broader market.

Even precious metals stocks in the Philadelphia Gold & Silver Index (XAU) are about 40% correlated to the S&P 500 over the past 24 months, near the high end of their historic range. On my chart only the S&P 500 Energy sector is showing a market correlation that’s below its long-term average.

However, just remember, energy and precious metals stocks combined account for just over 5% of the S&P 500 while the combined weight of the other 3 indices on my chart is 47.1% , almost 10 times.

Bottom line, let me leave you with 3 points:

Stock-bond hybrid strategies like 60/40 and target date retirement funds likely will not offer the same level of protection and safety as they have for much of the past 25 years, because stock and bond prices tend to be positively correlated during inflationary market environments.

When you buy the S&P 500 or an ETF like SPY, you’re mainly investing in a handful of large-cap stocks from industry groups that are highly correlated to the broader stock market. Increasingly the fate of these large stocks is driven by inflows of passive investment dollars and macroeconomic catalysts such as loose monetary policy rather than company-specific fundamentals. While that’s great when the rising tide of liquidity lifts all boats, it suggests most stocks will also fall as a group, providing little diversification benefit.

Much like the 1970’s consistently generating positive returns from stock and bond markets in coming years will likely rely on a combination of some timing of the cycles in the stock and bond markets coupled with buying specific groups, stocks and ETFs that have below-average correlation to the S&P and can provide a real diversification benefit. You’ll need to look harder to find places to hide from the market’s storms.

I feel as though there will not be a place to hide this time, maybe if you own physical silver or gold and have the ability to short. If you can trade in commodities you may also do well after the initial price drop.