What the Saudis Really Want

What the Saudis Really Want

It's Not What Most People Think

President Biden is scheduled to visit Saudi Arabia later this month.

And while the President recently denied he’d ask the Saudis directly to increase oil production, he did say that he felt all the Gulf states should be increasing oil production, not just Saudi.

He’s getting criticized on the right for begging Saudi Arabia for more barrels, while not exactly adopting a friendly (or even, frankly, a coherent) policy toward US domestic oil and gas production.

And the President is getting criticized on the left for agreeing to meet with Saudi Crown Prince Mohammed bin Salman at all.

You see, on the campaign trail, Biden labeled Saudi Arabia a “pariah” over the killing of journalist Jamal Khashoggi. And, in 2021 shortly after taking office, the Biden administration released a 2018 intelligence report indicating that the Crown Prince personally approved the operation to capture or kill Khashoggi.

The not-so-subtle accusation is that Biden is willing to betray Saudi human rights activists because he’s so desperate for the Kingdom’s barrels to bring down oil prices and inflation.

However, these criticisms from both sides of the aisle, the countless articles and editorials published in the mainstream media regarding the trip, even the Biden administration’s own policies seem predicated on one thing:

The simple assumption that the Saudis WANT higher oil prices because higher oil prices means more money in their pockets.

Listen, no one or, at least, no one outside the royal family and a small inner circle of those at the top of Saudi Aramco could tell you exactly what the Saudis want in terms of oil and gas prices. However, I have spent years watching the Kingdom’s policies toward oil and I’m often shocked at how many observers badly misinterpret Saudi energy policy and motivations.

For example, right now, I think the basic assumption the consensus is making is wrong, DEAD wrong — the Saudis do NOT want higher oil prices and, if they could, would probably happily push oil prices down to $80/bbl or so.

Unfortunately, the reality is far more dangerous as I’ll explain in a moment.

You see, the Saudis know that while high oil prices will temporarily boost their revenues, prolonged elevated prices have major, negative side effects.

The first is demand destruction. Sustained sky-high oil prices will tend to incentivize consumers to use less oil and we’re already seeing signs of that here in the United States:

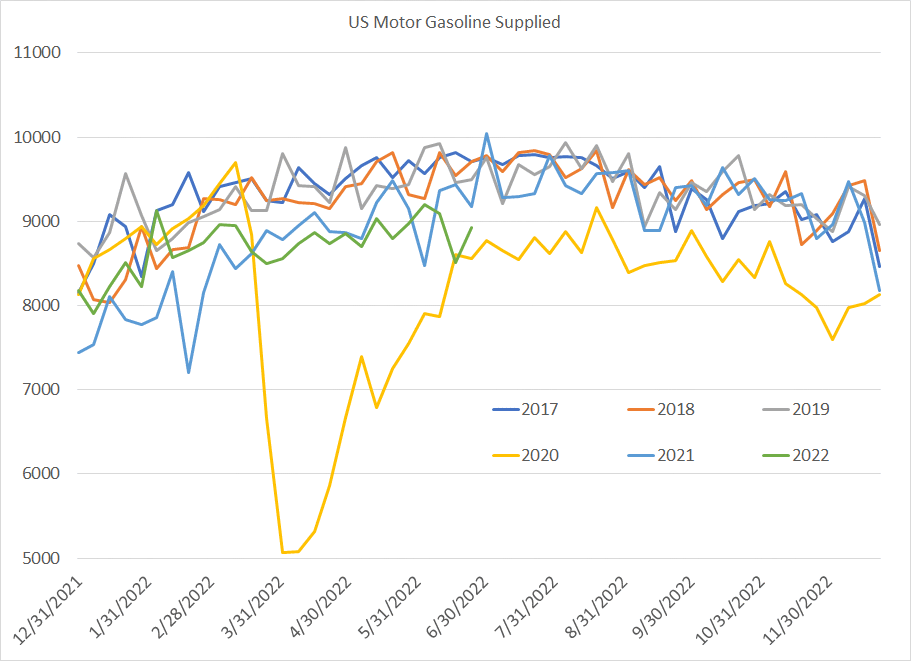

Source: Bloomberg, Energy Information Administration

This chart shows weekly products supplied figures from the US Energy Information Administration, a measure of US demand for gasoline.

I’ve included the year-to-date figures for 2022 as the green line; for the years 2017 to 2021 inclusive, the chart shows US gasoline demand on the equivalent week of the year.

Two points to note.

First, at the beginning of this year weekly gasoline demand was near (or at) a multi-year seasonal high, meaning gasoline demand was stronger-than-usual for that time of year.

Second, in the most recent week, gasoline demand is lower on a seasonal basis than any other year on my chart except 2020 when government-imposed coronavirus lockdowns pole-axed travel demand (and the economy as a whole for that matter). The key turning point was March — that’s roughly when weekly products supplied data for gasoline began to lag behind the other years on my chart.

Of course, there are a few obvious reasons for that. One is that prices, which had been rising sharply for more than a year leading up to Q1 2022, spiked well over $100/bbl in March. That’s how the market “communicates” — higher prices are the market’s way of forcing consumers to use less of something and for producers to supply more.

And, the demand side of the price signal is working as you can see in the chart I just showed you.

The other, related point is that the US economy showed clear signs of weakness starting early in 2022 and, as I’ve written before in The Free Market Speculator, the probability the country slips into recession by late this year or early next year is high and rising.

Some might say that Fed rate hikes can’t influence oil prices, but that’s silly — historically, when the US economy slips into recession, growth in demand for energy at least slows. In some cases, like the second half of 2008, gasoline demand falls outright.

In effect, engineering a recession isn’t an unwanted side effect of a Fed plan to lower inflation, it is THE plan.

But, from the Saudi’s perspective, sky-high oil prices are actually bad news as they will reduce demand for oil and risk pushing the US and global economies onto recession. Global recessions, in turn, historically cause oil prices to fall, sometimes precipitously.

Think about it: If you were the Saudi government, would you want to take an economic wrecking ball to your main customers so that they’re unwilling and/or unable to buy from you?

Very high oil prices also have negative implications for the Saudis from the supply side. For example a prolonged period of stable oil prices around $100/bbl leading up to the 2014 peak, encouraged more supply. High prices literally financed the shale boom while encouraging OPEC members to “cheat,” producing more than their quotas to generate higher revenues.

As far back as 2013, the Saudis began to bristle over absorbing a chronic oversupply of shale and OPEC barrels by cutting their own production to support prices. Finally, they opened the taps in late 2014 to force down prices, and suffered through six long, painful years of low and volatile prices trying to correct the glut.

Do you really think they’d want to encourage all that competition yet again and repeat that vicious oil bear market by keeping prices too high for too long?

I seriously doubt it.

If you’re interested in understanding exactly how the Saudis saw the oil market back in 2014, I’d encourage you to read Out of the Desert: My Journey from Nomadic Bedouin to the Heart of Global Oil by long-time Saudi Oil Minister Ali al-Naimi. It’s a fascinating read.

As I said, however, the reality is more dangerous:

The Saudis don’t WANT higher oil prices, they’re simply powerless to stop oil prices from rising.

Look, I’ve been saying that OPEC’s spare capacity to produce oil is much smaller than their official numbers suggest for some time, including in my January 19th piece in The Free Market Speculator $110 Crude Oil and Spare Capacity.

I was somewhat amused to read the recent headlines regarding a conversation French President Emmanuel Macron had with US President Joe Biden at the start of a G-7 meeting.

According to a recent, widely cited Bloomberg report, Macron relayed to Biden that MBZ – meaning Sheikh Mohammed bin Zayed of the UAE – told him two things.

First that the UAE is already “at maximum” output and, second, that the Saudis can only increase output a little bit, maybe 150,000 barrels a day or “a little more.”

OPEC is running out of spare capacity and the Saudis, already producing well more than 10 million barrels per day for several months now, are producing at a higher-than-comfortable level. These facts should be abundantly obvious to anyone with even a cursory knowledge of global energy markets and, quite frankly, it’s a bit worrying if this were really news to either President Macron or President Biden.

So, what do the Saudis really want?

The obvious answer would be a Goldilocks level of oil prices — not too high to drive the world into recession and force them to eventually admit they don’t have the capacity to produce much more crude. After all, it’s their spare capacity to produce oil that gives Saudi so much power and influence within OPEC and globally.

At the same time, obviously the Saudis would probably prefer oil prices at levels that allow them to sustain their revenues and keep their own population content through social spending.

This point is probably more controversial, but I suspect the Saudis are also pretty happy about one very valuable gift Europe and the US are handing them right now. You see, as I said earlier, oil like all commodities is driven by three related forces — supply, demand and price.

Price is the language and the balancing factor. Rising prices tend to reduce demand and increase supply while falling prices have the opposite effect. Oil price trends — either higher or lower — are the result of the fact that it takes time for supply and demand to adjust to higher prices. That’s particularly true of the supply side, since it generally takes years for conventional oil projects to move from the discovery phase to first commercial oil production.

The stickier supply and demand, the more time required for the market to balance and the more extreme the resulting moves in prices must be.

And here’s what’s even more important to remember:

Pain is always the direct and inevitable result of efforts to “control” the market or interrupt price signals.

Governments can and do control markets for a time; however, the market eventually will win out.

I’ve already given you one example: The Saudi efforts to maintain steady high oil prices from 2010 to 2014 were successful for years, but ultimately required a painful six-year rebalancing that hurt both Saudi revenues and the US shale industry. A classic circular firing squad.

Today, high oil prices, high natural gas prices (particularly in Europe) and clear signs that OPEC is running out of spare capacity should be a powerful signal to market participants to consume less and produce more. Unfortunately that signal is being blocked, at least in part.

The European Union (EU) has taken some pragmatic steps to offset the loss of Russian gas supply, including allowing more coal-fired power. However, the Continent continues to cling to naïve targets for carbon emissions reductions and expanding alternative energy technologies.

That’s the same intermittent wind and solar technologies that left Europe so hopelessly reliant on Russian gas imports. The same “green” policies that all but guarantee Germany and other EU countries must go begging to Moscow or risk economic devastation next winter.

Boris Johnson’s Conservative government in the UK implemented a windfall profits tax on oil producers, hardly a great way to encourage investment in new supply including billions of needed investment to develop planned projects within the North Sea region.

(Even better, the UK plans to deploy some of its ill-gotten tax gains to essentially subsidize energy, neutralizing a portion of the market’s price signal by artificially boosting demand.)

And, here in the US we have the Administration’s stop-go approach to new well permitting, intense activist campaigns against vital new energy infrastructure and a President who threatens to use “all reasonable and appropriate Federal Government tools and emergency authorities to increase refinery capacity and output in the near term.”

The latter threat is almost comical when you consider the US refining industry is already operating at 95 percent of operable capacity, well above average levels for this time of year and close to record highs. (At least it would be comical if it weren’t so sad).

As my colleague Roger Conrad points out in his recent Substack Piece, Politics is Sabotaging US Energy Policy, the left/right debate on US energy policy is making energy BOTH more expensive and less green.

However, this is all actually really great news for the Saudis.

By frustrating (even hobbling) major non-OPEC producers while pursuing unworkable renewable energy transition and climate policies, government is forestalling needed capital spending on new energy projects and increasing reliance on imported fuels. They’re squeezing Saudi Arabia’s main competitors including US shale and the big US and EU supermajors, increasing the value of Saudi reserves, subsidizing Saudi Aramco’s own production capacity expansion plans and lengthening and reinforcing the amplitude of the coming energy supercycle.

At least someone is happy.