Why Oil "Supercycles" End

Why Oil "Supercycles" End

PLUS: why the current rally will be be larger and more durable than most imagine.

Brent oil prices surged 18% from a late September low to last week’s highs near $98/bbl, a move that’s helped power a 13.9% rally in the S&P 500 Energy Index over the past week alone.

Oil’s moves this year have attracted plenty of attention from investors — after all, Energy is the only sector in the S&P 500 that’s up this year and it’s returned a whopping 53.1% year-to-date, outperforming the broader market by 75.8 percentage points.

And oil’s recent rise has also, predictably, attracted a ton of attention from the Biden administration and other politicians concerned about the impact of rising gasoline prices on their poll numbers with mid-term elections now less than a month away.

Most pundits will flag this week’s oil production cut from OPEC as the main reason for oil’s most recent surge; the cartel has been a convenient scapegoat for rising energy prices since the early 1970s.

However, the truth is the big rally in oil this year has been brewing for at least 8 years and has little or nothing to do with OPEC’s recent production cut or the Russia-Ukraine conflict.

Indeed, contrary to popular belief last week’s Saudi-led decision to cut production probably wasn’t a “snub” aimed at Biden or the US — the Kingdom is cutting production not because it wants to but because it must.

(That’s a big topic — I’ll have to leave a more detailed explanation for a future Substack).

The current “supercycle” in oil and other commodities wasn’t catalyzed by any single event and there’s no easy "fix” for what’s likely to be a multi-year cycle for commodities.

Oil prices cycles are all driven by supply and demand; however, here’s what’s crucial to remember:

True oil price supercycles – multi-year rallies in energy commodity prices -- are driven mainly by supply NOT demand.

That’s because energy and oil are the lifeblood of the global economy – if the global economy is growing, so too will demand for energy. Thus, while recessions – basically cyclical downturns in economic growth – can drive a temporary retreat in oil demand and prices, consumption and prices will rebound quickly as soon as the economy recovers.

Some might tell you that’s changing because the advent of electric vehicles spell a break in oil’s dominance as a transportation fuel. However, that’s largely hope and rhetoric over reality.

Just consider: According to the Energy Information Administration (EIA) the US consumed 94.4 quadrillion British Thermal Units (BTUs) of energy (known as “quads” for short) in 2012 in all forms including oil, natural gas, nuclear, coal and renewables. Of that total, oil accounted for 37.25% of energy demand, natural gas for 27.7% and coal for 18.4%. Thus, these three fossil fuels made up 83.35% of total energy demand a decade ago.

Fast forward 10 years to 2022 and EIA projects total US energy consumption of 98.82 quads of which oil, natural gas and coal account for 37.7%, 32% and 10.6% respectively. So, these three fossil fuels still account for 80.3% of total energy consumption and oil and gas are actually more important this year than they were a decade ago.

(For the record, non-hydroelectric renewables like solar and wind now account for just under 5.6% of US energy consumption up from just over 2% a decade ago, a modest rise despite a decade of rapid growth and significant government subsidies.)

The idea there will be an imminent, rapid transition away from oil, natgas and coal in the next few years rendering the global oil production industry “obsolete” represents a dangerous myth. Ironically, that myth, alongside government and investor response to it over the past few years, is what’s likely to prolong the current energy supercycle.

Take a look:

Source: BP Statistical Review or World Energy 2022

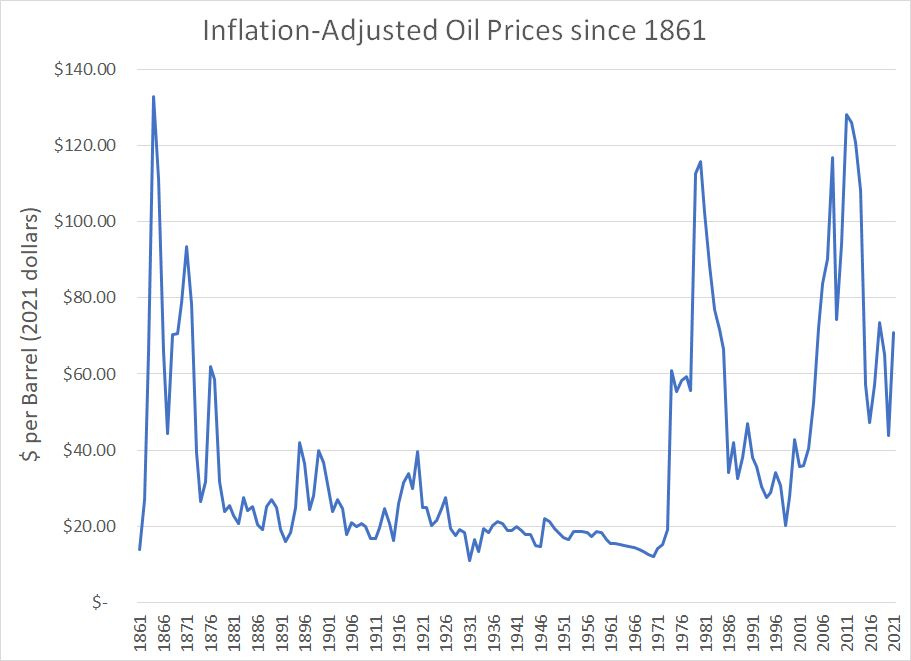

Here’s a chart of inflation-adjusted oil prices from 1861 through 2021. As you can see, from the dawn of the modern oil age in the mid-19th century, there have been several supercycles in prices of various magnitudes.

There have been two major supercycles for energy prices since the 1970s. The first sent oil from a price of $11.99 in 1970 (2021 dollars) to a peak of $115.68 in 1980. The second supercycle started in the late 1990s with oil bottoming at $20.19/bbl (2021 dollars) in 1998 and rallying to peak to make several peaks near $120/bbl between 2008 and 2014.

What ended these two price spikes?

It wasn’t a recession, Fed policy or a drop in demand for oil – global oil demand jumped from 45.4 million bbl/day in 1970 to 61.4 million bbl/day in 1980 and 66.251 million bbl/day in 1990 – oil rose from 1970 to the early 1980s and then fell significantly by 1990.

Same after 2014. As oil prices plummeted from late 2014 through 2021, global oil demand soared from 90.6 million bbl/day to 94.1 million bb/day.

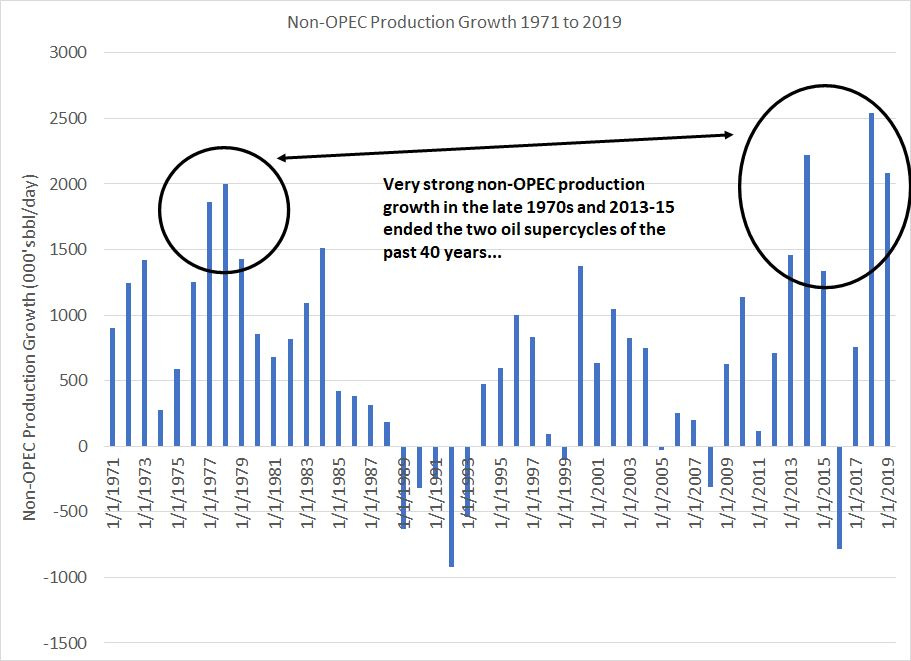

Instead, supercycles in oil come to an end for one reason and one reason ONLY: A surge in capital spending from oil producers that generates significant growth in global oil supply.

Take a look:

Source: Bloomberg, BP Statistical Review of World Energy

In the late 1970s and early 1980s major new production from Mexico, Alaska and the North Sea helped bring down oil prices and break OPEC’s dominance of global supply and prices.

In the three years from the end of 1976 to 1979, non-OPEC countries boosted production by around 5.3 million bbl/day, a volume that accounted for 8.2% of global daily oil demand in 1979.

In the 2014 to 2021 period it was shale – according to BP’s Statistical Review of World Energy US oil production surged from 6.78 million bbl/day in 2008 to more than 17.1 million bbl/day in 2019.

Further shale production growth in 2018 and 2019 despite lower oil prices helped keep prices low for much of the period from late 2014 to late 2020, keeping OPEC focused on defending market share.

The problem is that supply is sticky – it takes years of significant new investment in oil and gas projects before there’s a sizable and durable “payoff” in the form of rising energy production.

Unfortunately, government efforts to address rising gasoline prices -- ranging from efforts to cap prices, impose windfall taxes on producers or subsidize prices for consumers -- will tend to have the opposite effect. Simply put, by delaying the global investment and capital spending needed to incent a durable rise in global supply, these policies delay the very supply adjustment that can actually bring about an end to the supercycle.

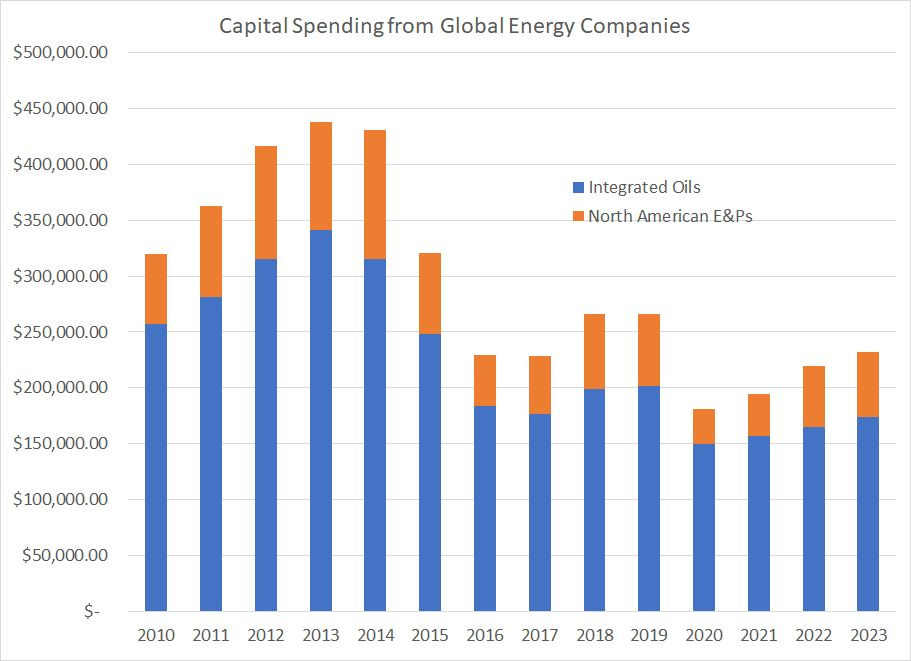

Investment has been lackluster for years:

Source: Bloomberg

This chart shows capital spending (CAPEX) from more than 40 energy producers — both large integrated names like Exxon Mobil (XOM) as well as smaller independent shale producers in North America — since 2010 with consensus estimates for full year 2022 and 2023 spending.

As you can see, annual CAPEX plummeted by almost 60% from the 2013 peak to the 2020 nadir and has only recovered slightly since that time. Indeed, current Wall Street projections show aggregate 2023 spending still down almost 50% from peak levels in 2013/14.

I’d argue this sets up a growing probability the coming supercycle in energy could be even bigger than 1998-2008 or, perhaps on some measures, the 1970s.

Unfortunately, rhetoric from western politicians, continues to all but guarantee that oil and gas producers will be reluctant to finance the massive wave of investment that’s desperately needed to end the current energy price supercycle and provide relief to consumers and inflation.

DISCLAIMER: This article is not investment advice and represents the opinions of its author, Elliott Gue. The Free Market Speculator is NOT a securities broker/dealer or an investment advisor. You are responsible for your own investment decisions. All information contained in our newsletters and posts should be independently verified with the companies mentioned, and readers should always conduct their own research and due diligence and consider obtaining professional advice before making any investment decision.