Bitcoin is Not Digital Gold

Bitcoin is Not Digital Gold

Why bitcoin could drop to $3,150 by yearend

In response to my June 13th article in Free Market Speculator, The Long and Short of Gold, I’ve received e-mails from readers asking if bitcoin is a viable alternative to the yellow metal.

That question isn’t a surprise: Some proponents of the cryptocurrency call it “digital gold,” implying that it fills a role equivalent to bullion or ETFs like the SPDR Gold Shares (NYSE: GLD).

So, let’s take a closer look. In The Long and Short of Gold, I outlined a model that attempts to explain 5-week changes in gold prices using contemporaneous moves in real interest rates (the yield on 5-year TIPS) and the US dollar (using the US dollar Index). While far from perfect, the model offers useful insight into what drives gold over the short-to-intermediate term.

If Bitcoin is “digital gold” then it’s logical to hypothesize a similar relationship exists between real interest rates, the US dollar and bitcoin.

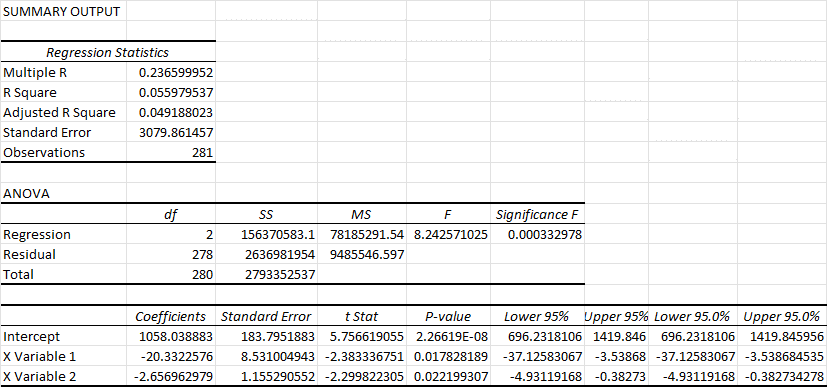

So, I performed the same regression and obtained these results:

Source: Bloomberg

First, gold has been around for thousands of years and has a long history of use as “money.”

Bitcoin is a recent invention. We have data on bitcoin trading back to 2010, but there wasn’t much volume in the cryptocurrencies prior to 2016 or so, so I used data on real interest rates, bitcoin and the US Dollar Index since December 30, 2016. This time series is almost 20 years shorter than what I used to create my gold model.

And, since cryptocurrencies trade over the weekend, I’m actually using the Bloomberg Galaxy Bitcoin Index to describe performance of bitcoin. This index has a good history of tracking the performance of bitcoin against the US dollar and the weekly closes line up with those of real rates and the US dollar Index.

Bottom line: the R-squared value here is just 5.6% compared to more than 26% for the gold model I showed you in my earlier article. While the coefficients of this regression model are statistically significant and show inverse correlation just as for gold, the model is weak.

Simply put, a model with a R-Squared fit of 26%+ is imperfect but useful while trying to use a model with a 5.6% R-squared is an exercise in futility.

So, what is correlated to bitcoin?

I tried several regressions in an effort to answer that question and came up with largely unsatisfactory results. For example, a simple regression of bitcoin against changes in the price of gold over the same time period yields a model with an R-squared of less than 0.5%, suggesting no relationship.

However, one of the more interesting models I tried was to regress the 5-week change in bitcoin against the 5-week change in the value of the Nasdaq 100 (NDX) Index. Interestingly, the Nasdaq and bitcoin are positively correlated, meaning that they tend to move in the same direction over time. The R-squared isn’t great, but at around 10.5%, it’s far higher than the correlations with gold, real rates or the US dollar.

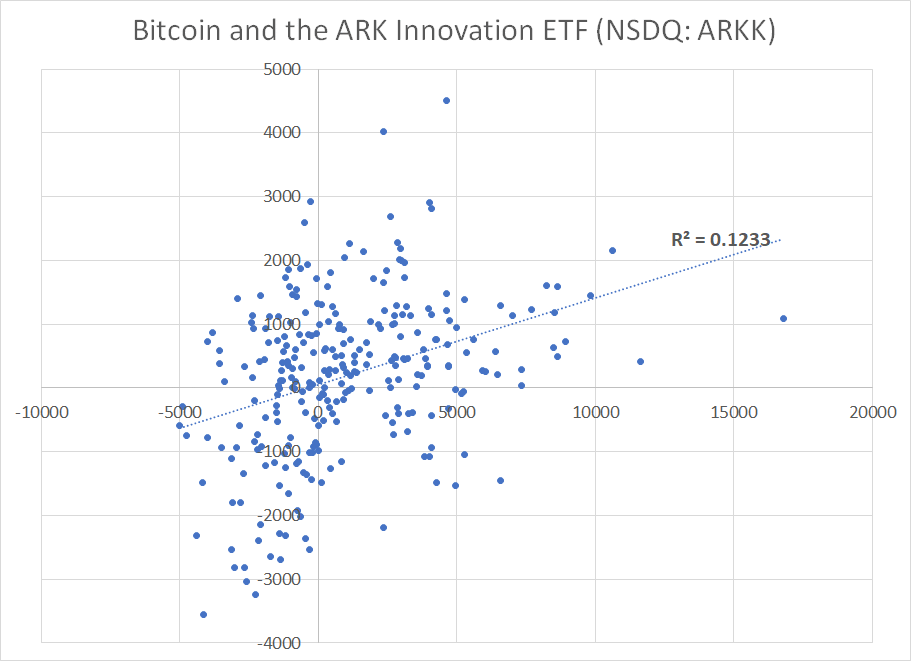

There was one more regression, however, that produced an even higher R-squared value:

Source: Bloomberg

This chart regresses 5-week changes in bitcoin against 5-week changes in the value of ARK Innovation ETF (NSDQ: ARKK). There’s a positive correlation here with an R-squared value of about 12.3%.

Of course, none of this is conclusive. However, I’d posit that bitcoin is NOT “digital gold,” but is far more likely simply a highly speculative pseudo-asset that flourished in recent years primarily due to extreme monetary and fiscal accommodation.

My Targets for Bitcoin

The recent pivot by the Federal Reserve, and the generational rotation away from more speculative and expensive growth stocks in is now crushing bitcoin and other cryptocurrencies alongside the Nasdaq and ARKK.

ARKK recently fell back to a closing low of $36.58, not far above its 2020 closing low of $34.69 and in-line with where it was trading and the end of 2019 before COVID-era stimulus inflated an ARKK bubble.

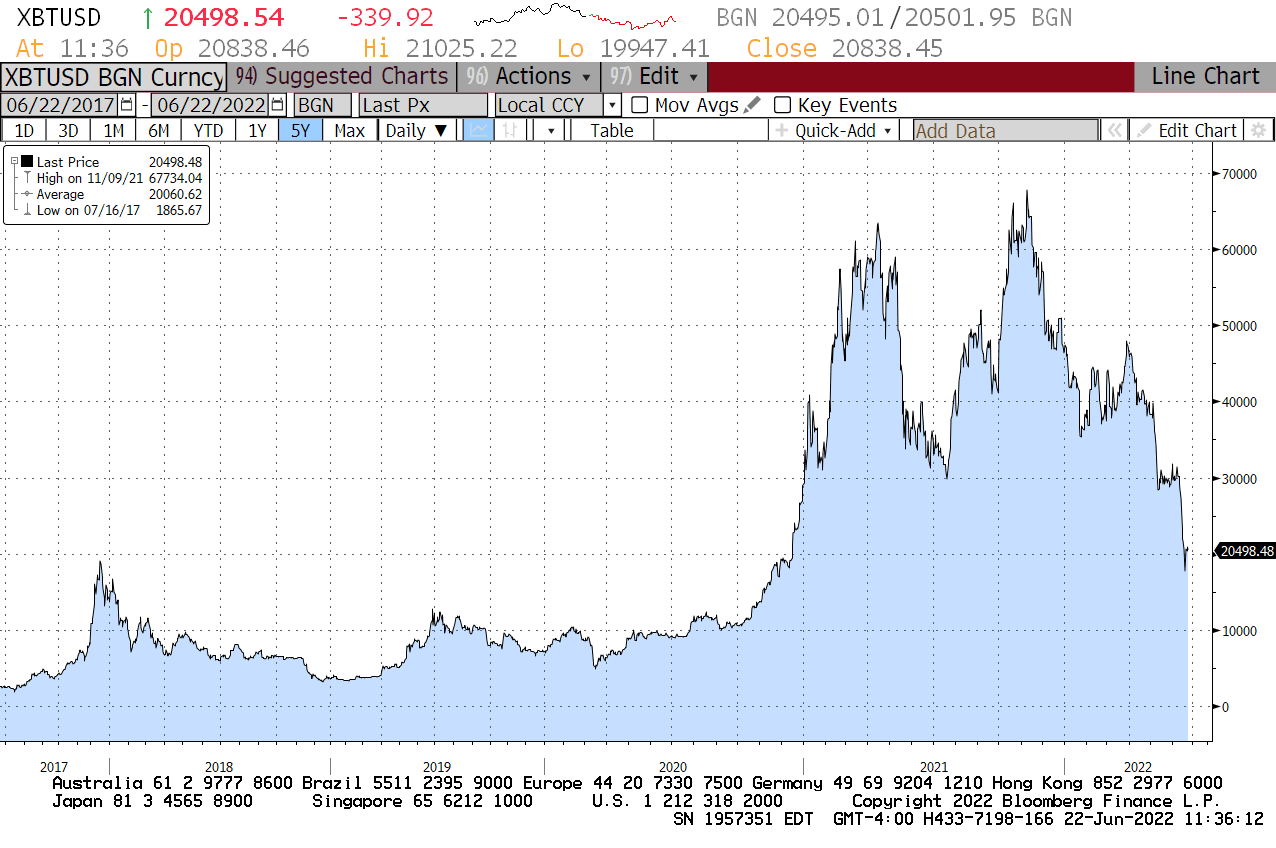

However, Bitcoin continues to hover around $20,000, which is well above where it was trading in 2018-2019:

Source: Bloomberg

I’d posit that bitcoin could easily fall back to $10,000 – half the current quote – which would represent a retest of the top of its late 2019/early 2020 trading range. In other words, bitcoin is likely to follow ARKK’s path in retracing all its coronavirus-era gains, it’s just taking the cryptocurrency a bit longer to get there.

There’s a second target worth keeping in mind: The late 2018 lows around $3,150.

Late 2018 is the last time the Fed tried to drain liquidity and tighten policy; back then the Powell Fed did an abrupt about-face as the stock market plummeted, led by more speculative growth names.

This time around, the Fed is once again tightening policy and growth assets are crashing, but the central bank doesn’t have the luxury of changing course to support stocks given the current sky-high rate of inflation.

So, let me ask you: Would it really be a huge surprise if risky “assets” like bitcoin returned to their late 2018 trading level?

I think that’s likely.

More broadly, there’s an old anecdote, told to me at a conference in San Francisco some 20+ years ago by a mining executive. The gist is this: More than 2,000 years ago during the time of the Roman republic, a Roman Senator could purchase a toga (the formal clothing of that time) appropriate for the floor of the Senate for a cost of approximately 1 ounce of gold. We know this because the Romans kept copious accounts of the cost of various items and their currency, the denarius, was backed by precious metals (gold and silver).

Today, some 2000+ years later, the Roman denarius has no value except perhaps as part of a coin collection. The Romans began debasing their currency – literally reducing the actual content of gold and silver in coins over time – long ago, almost immediately after the currency was introduced in the third century BC. And, of course, the Roman state, which theoretically backed the value of their currency, fell long ago and was a declining military power for a century or two prior to actual collapse.

However, I can still take an ounce of gold (worth around $1,800 right now) and buy a high-quality modern suit with it.

In other words, gold is money and has retained its purchasing power since Roman times, remaining a viable store of value for millennia, through a variety of different empires, currency hegemonies, economic environments and through both war and peacetime. Indeed, gold was money long before Rome existed as there are records from the Mesopotamian civilization of the 7th millennium BC showing the use of coins, bars and ingots as a medium of exchange.

Simply put, based on around 9,000 years of history, gold is money. And based on about 12 years of history, bitcoin is a highly speculative pseudo “asset” with little or no enduring value.

Enjoyed this article? Please consider hitting the heart-shaped “like” button below or sharing the post with friends on social media.

DISCLAIMER: This article is not investment advice and represents the opinions of its author, Elliott Gue. The Free Market Speculator is NOT a securities broker/dealer or an investment advisor. You are responsible for your own investment decisions. All information contained in our newsletters and posts should be independently verified with the companies mentioned, and readers should always conduct their own research and due diligence and consider obtaining professional advice before making any investment decision.