Getting Real

Getting Real

Rising real rates eventually sink stocks

I’ve already spilled considerable digital ink in The Free Market Speculator this week, so I’ll keep this column on the short side today.

As many of you are probably aware, the Fed took its long-anticipated “pause” yesterday by keeping its target for the Fed Funds rate unchanged. However, while the headline wasn’t a surprise, and equity markets ended the day slightly higher, the central bank still managed to shock markets:

Source: Bloomberg

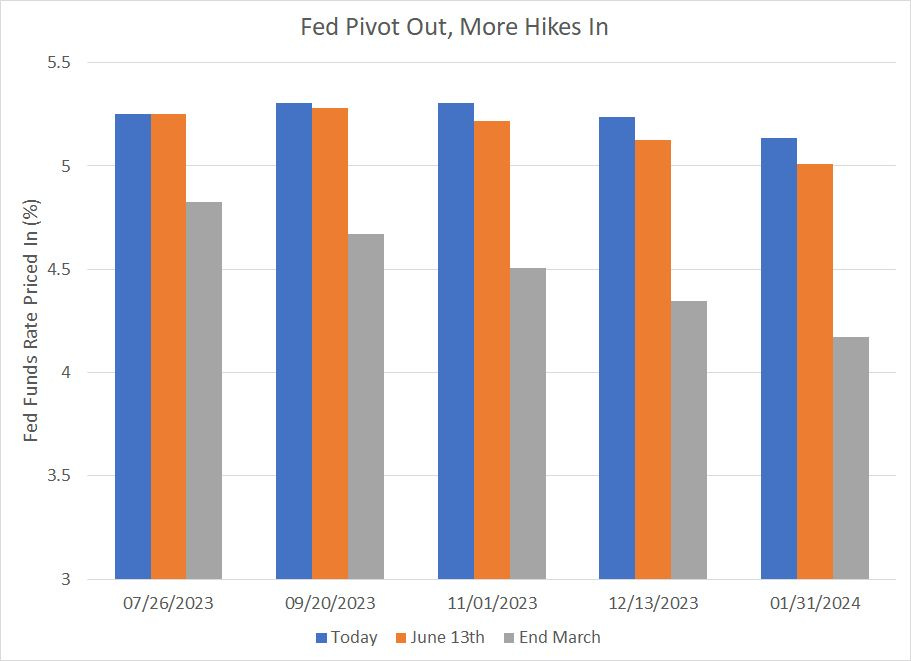

This chart examines expected Fed policy following its next 5 meetings through to January 2024.

This morning futures are pricing in 70% probability the Fed hiked by 25 basis points at its next scheduled meeting on July 26th and 90% probability of a hike by the time of its September 20th meeting.

Just as important, futures have all but priced out any cuts in rates over this time period – there’s a 42.6% probability the Fed cuts 25 basis points from that peak rate by next January, but rates are expected to end January 2024 above 5%.

That’s slightly more hawkish than where this market closed Tuesday; however, the biggest change comes in comparison to expectations at the end of March when futures were looking for the Fed to slash interest rates in the second half of this year, reaching a level of just 4.17% by January 31st.

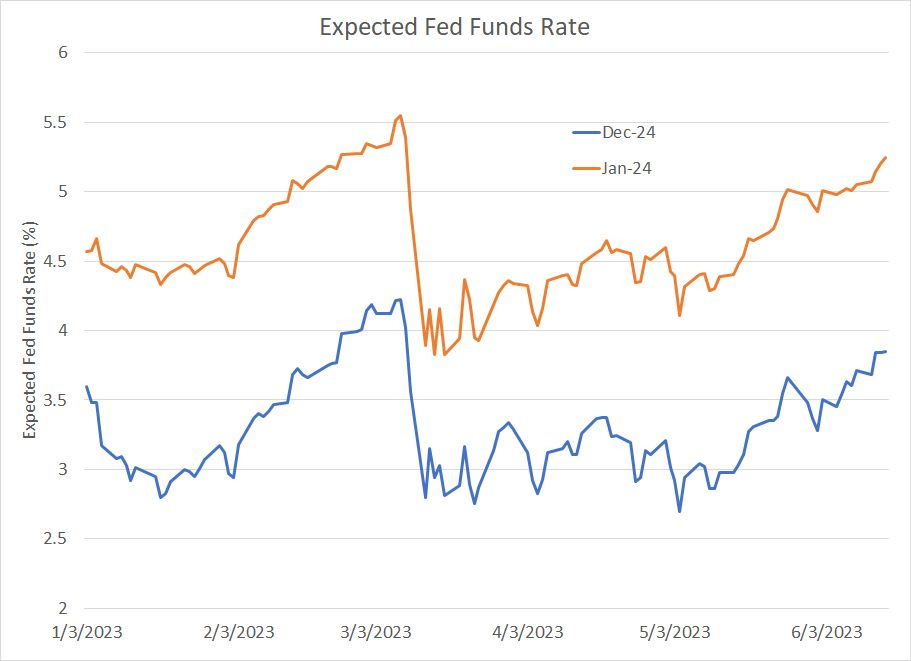

Source: Bloomberg

This chart shows the evolution of rate expectations since the beginning of the year for January 2024 and December 2024 (end of next year). As you can see, market expectations for Fed policy rates slumped in early March as the regional banking mini-crisis and the collapse of SVB Financial sparked concerns of an imminent tightening in credit and recession.

Since that time, however, expectations for rates at the end of next January have trended higher and we’re now approaching those early March highs.

It also seems the higher-for-longer interest rate narrative is gaining traction as expectations for year-end 2024 rates have creeped back to 3.85% from a nadir of under 2.7% in early May.

What’s even more incredible about all this is that markets still aren’t even pricing in the Fed’s own expectations for interest rates this year and next.

According to the Summary of Economic Projections released yesterday, the median expectation of Federal Reserve Board members is for the Fed Funds rate to end this year at 5.6% and to end 2024 at 4.6%. That’s a full 50 basis points higher from their projections released back in March for December 2023 and 0.3% higher for December of 2024.

That implies about 2 more 25 basis point hikes for 2023 – only 1 is priced into the futures right now – and about 100 basis points of cuts through 2024 compared to market expectations for around 140 basis points of cuts next year.

The Nasdaq Isn’t Getting Real

And let’s not forget that what matters most to markets isn’t the nominal level of interest rates but the real interest rate – the level of interest rates adjusted for inflation:

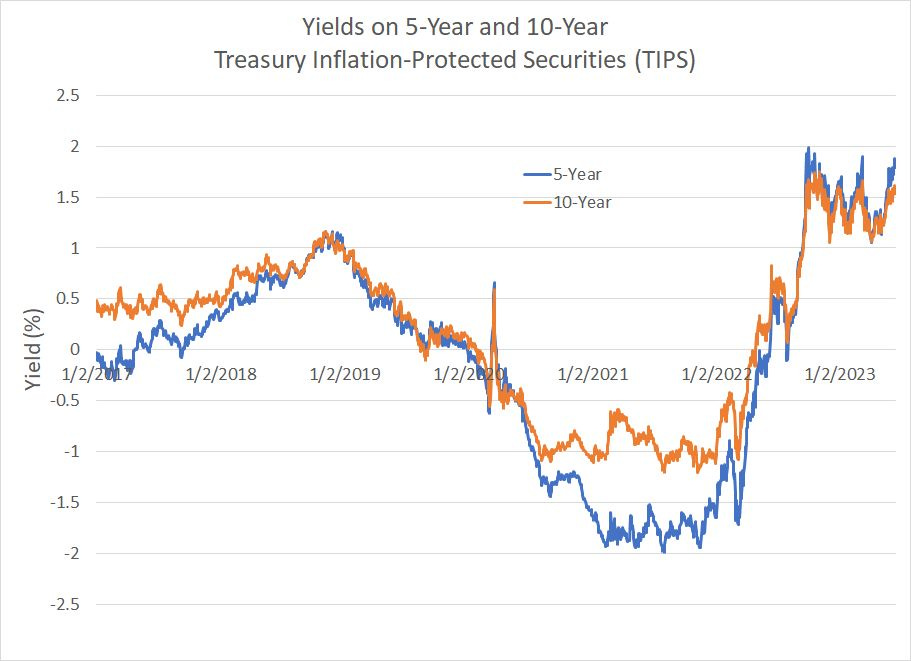

Source: Bloomberg

This chart shows the yield on 5-Year and 10-Year Treasury Inflation-Protected Securities (TIPs) since early 2017.

As you can see, real interest rates are close to their highs set late last year and have surged in recent weeks from 1.06% in early April to almost 1.9% for the 5-Year as of the most recent quote.

I’ve only pictured the data here since 2017, but the last time US 5-year real interest rates were sustainably above 2% was 2006-07. And, as many of you will undoubtedly recall, that episode didn’t end well.

The reason is that the Fed continues to hike rates even though the even as markets remain confident that inflation is no longer a problem as I explained in “Inflation Complacent.”

What’s particularly interesting is that the Nasdaq 100 has historically been particularly sensitive to real interest rates because the index depends on distant future cash flows to support current valuations. Rising real rates drive up the rate at which future cash flows are discounted, depressing valuations.

Yet, despite all that, the Nasdaq 100 has outperformed the S&P 500 by 8.2% since April 6, 2023 even as the 5-year real yield has jumped 78 basis points.

The most likely explanation for that in my view is investors’ current enthusiasm for artificial intelligence (AI), which is powering a handful of the largest names in the Nasdaq. Indeed, the outperformance of the Nasdaq 100 Equal Weight to the S&P 500 is just 0.81% over the same period.

Investors Getting Bullish

Meanwhile, the latest data from the American Association of Individual Investors (AAII) survey is now out:

Source: Bloomberg

As you can see, individual investors bullish on the stock market now outnumber the bears by 22.5%, the largest such gap since late 2021, when the Nasdaq peaked for the current cycle.

None of this means the market will peak soon or that the Nasdaq will stop outperforming the S&P 500. As I noted in the June 5th FMS “Bubbles: Timing is the Trouble,” it’s far easier to identify a bubble in markets than it is to time a top.

However, something (still) must give.

The experience of late 1999-00 shows that bubbles can carry on longer than most expect; however, ultimately the Nasdaq isn’t immune to building risks of a US recession, rising real interest rates and tightening US credit conditions.

DISCLAIMER: This article is not investment advice and represents the opinions of its author, Elliott Gue. The Free Market Speculator is NOT a securities broker/dealer or an investment advisor. You are responsible for your own investment decisions. All information contained in our newsletters and posts should be independently verified with the companies mentioned, and readers should always conduct their own research and due diligence and consider obtaining professional advice before making any investment decision.