No Good News and No Bad News

No Good News and No Bad News

Earnings season is now underway

On Friday morning JP Morgan Chase (NYSE: JPM) released its quarterly earnings report, marking the (unofficial) start of Q2 2023 earnings season.

The report was strong across-the-board with the financial giant beating earnings per share estimates, beating revenue estimates and guiding net interest income (NII) – basically the difference between interest received on loans and paid out to depositors – higher for the rest of 2023.

As always, JPM’s earnings call was worth a listen this quarter as management sounded a more cautious tone than seemed warranted by the headline results. For example, guidance on NII was probably the single largest positive surprise in results. And here, both CFO Jeremy Barnum and CEO Jamie Dimon indicated the ongoing surge in NII was unsustainable longer term.

As I said, NII is really a combination of two pieces – the interest rate charged on loans and the interest paid out to customers to attract deposits. When the Federal Reserve boosts interest rates, that’s going to tend to increase rates banks can charge on their loans, so it’s a significant and ongoing tailwind for NIIs at most banks.

Commercial and Industrial (C&I) loans – loans to businesses – typically carry floating rates and are indexed to various benchmarks, resetting higher automatically as rates rise. Credit cards also tend to carry floating rates benchmarked to indices like the Prime Rate, so JPM will tend to see rising interest income from these loans as well when rates rise.

Of course, deposit rates also have some sensitivity to interest rate benchmarks – when the Fed hikes, banks are likely to increase the rates paid on deposits to attract customers. After all, if you can earn extra yield by putting your money in Treasury Bills or a money market account, there’s temptation to withdraw cash from your bank and log in to your Treasury Direct account.

Historically, the rate at which banks hike interest paid on deposits is slower than the rate at which loans reprice, so rising rates will tend to boost NII and bank profits on balance. However, there’s usually a tipping point each cycle where the deposit market grows more competitive, forcing banks to hike rates paid on products like CDs more aggressively, cutting net interest margins.

This year, however, JPM has benefited from rising rates, but hasn’t yet had to compete with other financial institutions to attract deposits, at least not to the same degree as in prior cycles.

One reason: When SVB Financial collapsed in March, there was fear uninsured depositors – those with over $250,000 on deposit at the bank—would lose their uninsured deposit balances or, at a minimum, lose access to their funds for a prolonged period.

In the end, FDIC stepped in and guaranteed all SVB deposits to quell these fears and, presumably, prevent an Old School “run” on regional banks where depositors withdrew their funds en masse.

The Fed followed up with a new lending facility, the Bank Term Funding Program (BTFP), which allows regional banks to borrow against their portfolios of Treasury securities to help ease liquidity constraints caused by deposit flight. But the uncertainty still did prompt many depositors to question the safety of their funds.

As a result, some moved deposits from smaller banks to the systemically important financial institutions (SIFI) like JPM, which are subject to extra regulatory burdens and capital requirements. Banking regulations put in place since the 2007-09 crisis years have created a (bizarre) two-tier banking system in the US comprised of the SIFIs and everyone else. The SIFs are considered “too big to fail” and, by extension, a port in the storm when the system is perceived to be under stress.

Thus, JPM hasn’t had a need to compete to attract deposits to the same degree as in prior cycles.

However, consider this exchange between an analyst and CEO Jamie Dimon during the Q&A portion of the call:

Question: Good morning. So, I mean, in your camp that eventually consumers will want more deposit rate sensitivity here, but I guess what would make you change your rates meaningfully? So the top two banks have about 50% consumer market share, loan-to-deposit ratios are low, your outlook for loan growth, and I think others, it's fairly sluggish, at least outside of card. So I get that it's common sense and that's what we've seen historically, but there really is this kind of big divergence among big banks and everybody else where the big banks just don't need to pay that much for deposits for a slew of reasons. So what would make you change that?

Answer Jamie Dimon: I think every bank is in a different position about what they need. And so, you have a whole range of outcomes. But remember, we do this also by city. So you have different competition in Arizona and Phoenix than you have in Chicago, Illinois. And we do have high interest rate products. So it's a combination of all those things. I wouldn't call it a big bank or a small bank. And you're going to see whenever we report who kind of paid up a little bit more for things and who didn't and things like that.

So, look, guys, I would take it as a given. I think it's a mistake. There is very little pricing power in most of our business and banks are going to go up. Take it as a given. There is no circumstance that we've ever seen in the history of banking where rates didn't get to a certain point that you had to have competing products. And rates go from migration or direct rates or movement to CDs or money market funds. And we're going to have to compete for that. You already see it in parts of our business and not in other parts.

Source: Bloomberg; JPM Q2 2023 Earnings Conference Call

Simply put, Dimon says, as clearly as possible, that even JPM, widely considered among the safest and best-managed banks in the US, will eventually have to raise rates to attract deposits and that’s likely to cut their net interest income (NII).

Big banks aren’t immune to the tightening of credit conditions and falling deposits across the financial system.

Deposits, QE and QT

Here’s the bigger picture:

Source: Federal Reserve, Bloomberg

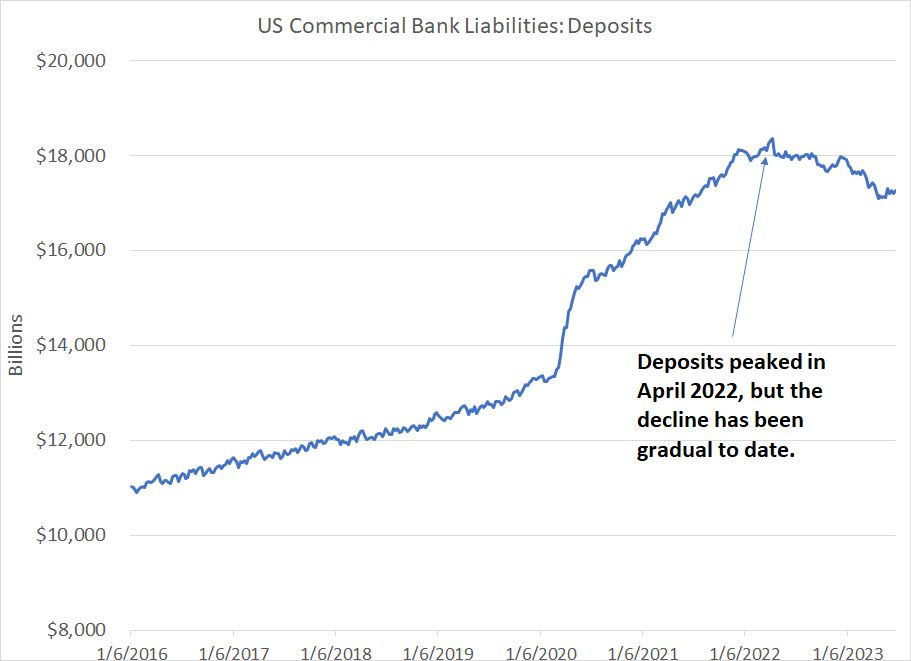

This chart shows total deposits held by all commercial banks in the US, both large institutions like JPM as well as smaller regional and local banks.

Quantitative easing (QE) aims to flood the banking system with deposits to stimulate credit creation and economic activity. On this chart, you can see how quickly deposits rose across the banking system in 2020-21 from around $13.35 trillion in early 2020 to a peak of more than $18.3 trillion in April 2022.

As the Fed hiked rates and started Quantitative Tightening (QT), banking deposits have started to fall, though the pace of decline is far slower than the rise in 2020-21. Thus, the US banking system still has excess deposits and that’s further reduced the need for banks to compete for funds by raising interest rates paid on savings products.

Of course, as I just explained, the picture is different for large banks like JPM as compared to smaller regional banks; the latter did experience more significant deposit flight this spring and some of those deposits found their way to SIFIs like JPM. Dimon’s comments make it clear this tailwind will not persist forever, and banks will start to compete on rates to forestall customers withdrawing deposits to place in higher yielding money market funds, government bonds or CD products.

Rates and Consumers

Dimon and Barnum also had some interesting comments regarding the US consumer during the Q&A session:

Analyst: Good morning. I guess just first question following up on the outlook for the economy, like, we've all been worried about a recession for a year and there's a debate about the lagged effects of the Fed rate hike cycle. When you think about, Jeremy, I think you mentioned your unemployment outlook relatively similar today versus a quarter ago. How worried should we be in terms of the credit cycle 6 to 12 months from now or are you leaning towards concluding that maybe U.S. businesses consumers have absorbed the rate cycle a lot better than we expected a year ago?

Jeremy Barnum: Yes, so I'm sure Jamie has some views here, but in my view, I would just caution against jumping to too many super positive conclusions based on a couple of recent prints. And I think generally, our point is less about trying to predict a particular outcome and more about trying to make sure that we don't get too much euphoria that over-concentrates people on one particular prediction when we know that there's a range of outcomes out there.

So obviously, people are talking a lot about the potential for soft landing right now, no landing, immaculate disinflation, or whatever. And whether our own views on that have changed meaningfully, I don't know. But the broader point is that we continue to be quite focused on Jamie's prior comments that loss rates still have room to normalize even post-pandemic, so we're probably over-earning on credit a little bit.

Obviously, we've talked about the expectation that the NII is going to come down quite a bit. So even forgetting about whether you get some surprisingly negative outcomes on the economy from what we've done today, even in the central case, you just need to recognize that there should be some significant normalization.

Jamie Dimon: Yeah, and I would just add that the 5.8% is not our prediction. That is the average of the unemployment under multiple scenarios that we have to use, which are hypothetical to see some. If you have those predictions, it could all come with something different. And we don't know the outcome. We're trying to be really clear here. The consumer's in good shape. They're spending down their excess cash. That's all tailwinds.

Even if we go into a recession, they're going in with rather good conditions, low borrowings and good house price value still. But the headwinds are substantial and somewhat unprecedented. This war in Ukraine, oil and gas, quantitative tightening, unprecedented fiscal needs of governments, QT, which we've never experienced before. I just think people should take a deep breath in that. And we don't know what those things are going to put us in a soft landing, a mild recession, or a hard recession. And obviously, we should all hope for the best.

Source: Bloomberg, JP Morgan Q2 2023 Earnings Conference Call

In particular, it struck me as notable Barnum mentioned the “no landing” and “immaculate disinflation” scenarios. The former is the view the US economy won’t slow appreciably despite the Fed’s recent spate of hikes, and the latter is the view (dream) that inflation can glide back down to target without a meaningful slowdown in US economic growth and consumer spending.

Both Dimon and Barnum seemed to pour a big bucket of cold water on that view saying that even in a soft-landing scenario there’s significant room for credit trends to normalize, meaning non-performing loans and charge-offs would rise. Further, embracing the most sanguine outcomes ignores multiple key risks still facing the US economy and consumers.

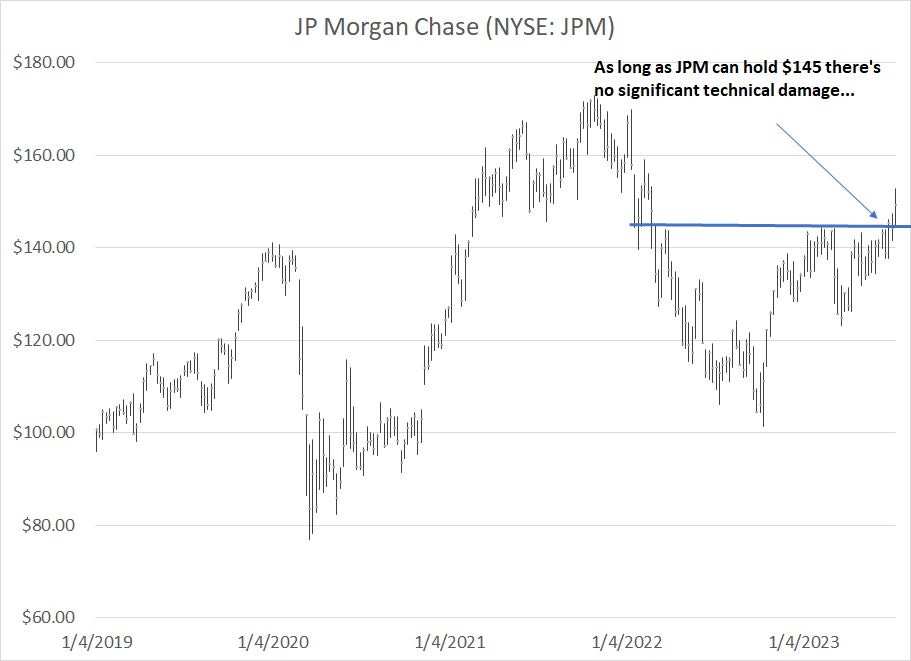

From a technical perspective, JPM stock sits at a crucial juncture:

Source: Bloomberg

The $145 level has served as resistance on multiple occasions since March 2022 and the stock finally popped above that resistance level this month, reaching a peak of $152.89 immediately after the opening bell today.

As always, a stock’s reaction to good earnings news is more important than the news itself. And, as it stands right now, JPM shares lost most of their opening gap higher on Friday following their earnings release; however, the stock did manage a rally yesterday and remains above that critical $145 support.

Perhaps investors will ultimately dismiss management’s cautious comments as an effort to under promise or lower the bar of expectations, putting the company in a good position to beat expectations going forward. And, unless the stock breaks down below $145 over the next week or so, there’s little long-term implication.

However, for three quarters straight now, JPM has generally rallied on the day after reporting earnings including a sizable 7.6% pop on April 14th after the bank’s Q1 2023 results, so I do think a more muted reaction this quarter is a potential red flag.

More broadly, the market’s attention is likely to shift away from economic news for the next few weeks to earnings news, particularly results from most of the tech heavyweights between late-July and early August.

One major problem is investor expectations are looking inflated as we head into earnings season, a point I covered at some length in last Thursday’s issue “The Great Rotation.”

DISCLAIMER: This article is not investment advice and represents the opinions of its author, Elliott Gue. The Free Market Speculator is NOT a securities broker/dealer or an investment advisor. You are responsible for your own investment decisions. All information contained in our newsletters and posts should be independently verified with the companies mentioned, and readers should always conduct their own research and due diligence and consider obtaining professional advice before making any investment decision.